Question 23 Chapter 4 of +2-A

Table of Contents

23. A, B and C are partners sharing profits and losses in the ratio of 5 : 3 : 2. Their Balance Sheet as at 31st March, 2019 stood as follows:

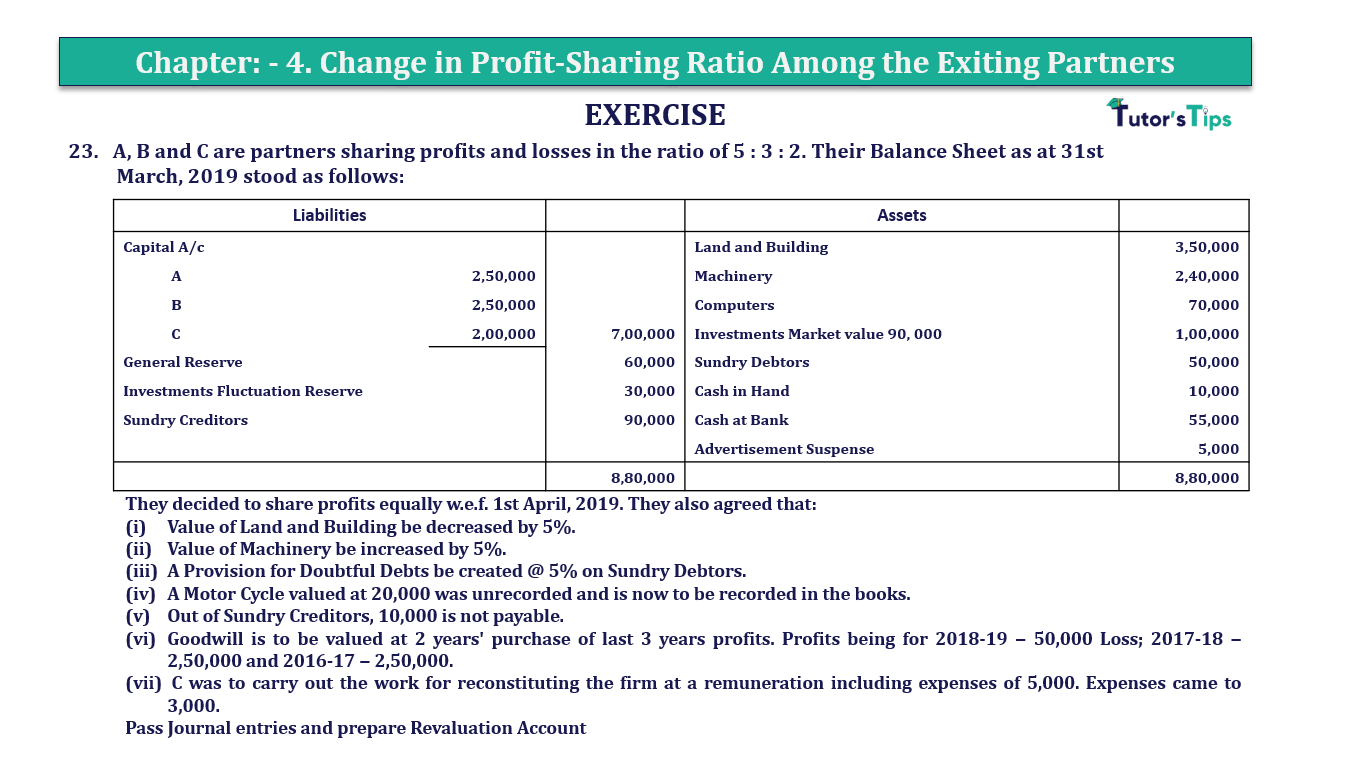

| Liabilities | Assets | |||

| Capital A/c | Land and Building | 3,50,000 | ||

| A | 2,50,000 | Machinery | 2,40,000 | |

| B | 2,50,000 | Computers | 70,000 | |

| C | 2,00,000 | 7,00,000 | Investments Market value 90, 000 | 1,00,000 |

| General Reserve | 60,000 | Sundry Debtors | 50,000 | |

| Investments Fluctuation Reserve | 30,000 | Cash in Hand | 10,000 | |

| Sundry Creditors | 90,000 | Cash at Bank | 55,000 | |

| Advertisement Suspense | 5,000 | |||

| 8,80,000 | 8,80,000 |

They decided to share profits equally w.e.f. 1st April, 2019. They also agreed that:

- Value of Land and Building be decreased by 5%.

- Value of Machinery be increased by 5%.

- A Provision for Doubtful Debts be created @ 5% on Sundry Debtors.

- A Motor Cycle valued at 20,000 was unrecorded and is now to be recorded in the books.

- Out of Sundry Creditors, 10,000 is not payable.

- Goodwill is to be valued at 2 years’ purchase of last 3 years profits. Profits being for 2018-19 − 50,000 Loss; 2017-18 − 2,50,000 and 2016-17 − 2,50,000.

- C was to carry out the work for reconstituting the firm at a remuneration including expenses of 5,000. Expenses came to 3,000.

Pass Journal entries and prepare Revaluation Account

The solution of Question 23 Chapter 4 of +2-A

| In the Books of _______________ | |||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2019 | |||||

| April 1 | General Reserve A/c*1 | Dr | 60,000 | ||

| To A’s Capital A/c | 30,000 | ||||

| To B’s Capital A/c | 18,000 | ||||

| To C’s Capital A/c | 12,000 | ||||

| (Being General Reserve Distributed among partners) | |||||

| A’s Capital A/c | Dr | 2,500 | |||

| B’s Capital A/c | Dr | 1,500 | |||

| C’s Capital A/c | Dr | 1,000 | |||

| To Advertisement Suspense A/c*2 | 5,000 | ||||

| (Being Advertisement Suspense adjusted) | |||||

| Investment Fluctuation Reserve A/c*3 | Dr | 30,000 | |||

| To Investment A/c | 10,000 | ||||

| To A’s Capital A/c | 10,000 | ||||

| To B’s Capital A/c | 6,000 | ||||

| To C’s Capital A/c | 4,000 | ||||

| (Being Investment Fluctuation Reserve is Distributed among partners and adjusted) | |||||

| Revaluation A/c | Dr | 25,000 | |||

| To Land & Building A/c | 17,500 | ||||

| To Provision for Doubtful Debts A/c | 2,500 | ||||

| To Bank A/c | 5,000 | ||||

| (Being Increase in the value of the assets and decrease in the values of liabilities are transferred to revaluation a/c) | |||||

| Machinery A/c | Dr | 12,000 | |||

| Motor Cycle A/c | Dr | 20,000 | |||

| Creditors A/c | Dr | 10,000 | |||

| To Revaluation A/c | 42,000 | ||||

| (Being Increase in the value of the assets and decrease in the values of liabilities are transferred to revaluation a/c) | |||||

| Revaluation A/c*4 | Dr | 17,000 | |||

| To A’s Capital A/c | 8,500 | ||||

| To B’s Capital A/c | 5,100 | ||||

| To C’s Capital A/c | 3,400 | ||||

| (Being Profit on revaluation of assets and liabilities are Distributed among partners) | |||||

| B’s Capital A/c | Dr | 10,000 | |||

| C’s Capital A/c | Dr | 40,000 | |||

| To A’s Capital A/c*5 | 50,000 | ||||

| (Being goodwill account adjusted) | |||||

Working Note :

WN *1 Calculation of Adjustment of General Reserve: –

| Amount to be Credited to A’s Capital | = | 60,000 | X | 5 |

| 10 | ||||

| = | 30,000 |

| Amount to be Credited to B’s Capital | = | 60,000 | X | 3 |

| 10 | ||||

| = | 18,000 |

| Amount to be Credited to C’s Capital | = | 60,000 | X | 2 |

| 10 | ||||

| = | 12,000 |

WN *2 Calculation of Adjustment of Advertisement Suspense: –

| Amount to be Debited to A’s Capital | = | 5,000 | X | 5 |

| 10 | ||||

| = | 2,500 |

| Amount to be Debited to B’s Capital | = | 5,000 | X | 3 |

| 10 | ||||

| = | 1,500 |

| Amount to be Debited to C’s Capital | = | 5,000 | X | 2 |

| 10 | ||||

| = | 1,000 |

WN *3 Calculation of Adjustment of General Reserve: –

| Distributable Amount of I.F.R. | = | Total I.F.R. Balance – (Difference between Market value and Cost) |

| = | 30,000 – (90,000 – 80,000) | |

| Distributable Amount of I.F.R. | = | 20,000 |

| Amount to be Debited to A’s Capital | = | 20,000 | X | 5 |

| 10 | ||||

| = | 10,000 |

| Amount to be Debited to B’s Capital | = | 20,000 | X | 3 |

| 10 | ||||

| = | 6,000 |

| Amount to be Debited to C’s Capital | = | 20,000 | X | 2 |

| 10 | ||||

| = | 4,000 |

WN *4 Calculation of Adjustment of Revaluation Profit: –

| Amount to be Debited to A’s Capital | = | 17,000 | X | 5 |

| 10 | ||||

| = | 8,500 |

| Amount to be Debited to B’s Capital | = | 17,000 | X | 3 |

| 10 | ||||

| = | 5,100 |

| Amount to be Debited to C’s Capital | = | 17,000 | X | 2 |

| 10 | ||||

| = | 3,400 |

| Old Ratio of X, & Y | = | 5 : 3 : 2 |

| New Ratio of X, & Y | = | 1 : 1 : 1 |

Calculate the Sacrificing or Gaining Ratio of Partners

Sacrificing or Gaining Ratio = Old Ratio – New Ratio

| A’s Share Sacrificing/Gaining | = | 5 | – | 1 |

| 10 | 3 |

| = | 15- 10 | |

| 30 |

| = | 5 | (Sacrificing) |

|

| 30 |

| B’s Share Sacrificing/Gaining | = | 3 | – | 1 |

| 10 | 3 |

| = | 9- 10 | |

| 30 |

| = | – 1 | Gain |

|

| 30 |

| C’s Share Sacrificing/Gaining | = | 2 | – | 1 |

| 10 | 3 |

| = | 6- 10 | |

| 30 |

| = | – 4 | Gain |

|

| 30 |

WN *5 Adjustment of Goodwill : –

| Goodwill | = | Average Profit X No. of years’ Purchase |

| = | 1,50,000 X 2 | |

| Goodwill | = | 3,00,000 |

| Amount to be Credited to A’s Capital | = | 3,00,000 | X | 5 |

| 30 | ||||

| = | 50,000 |

| Amount to be Debited to B’s Capital | = | 3,00,000 | X | 1 |

| 30 | ||||

| = | 10,000 |

| Amount to be Debited to C’s Capital | = | 3,00,000 | X | 4 |

| 30 | ||||

| = | 40,000 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication