Question 11 Chapter 1 – Unimax

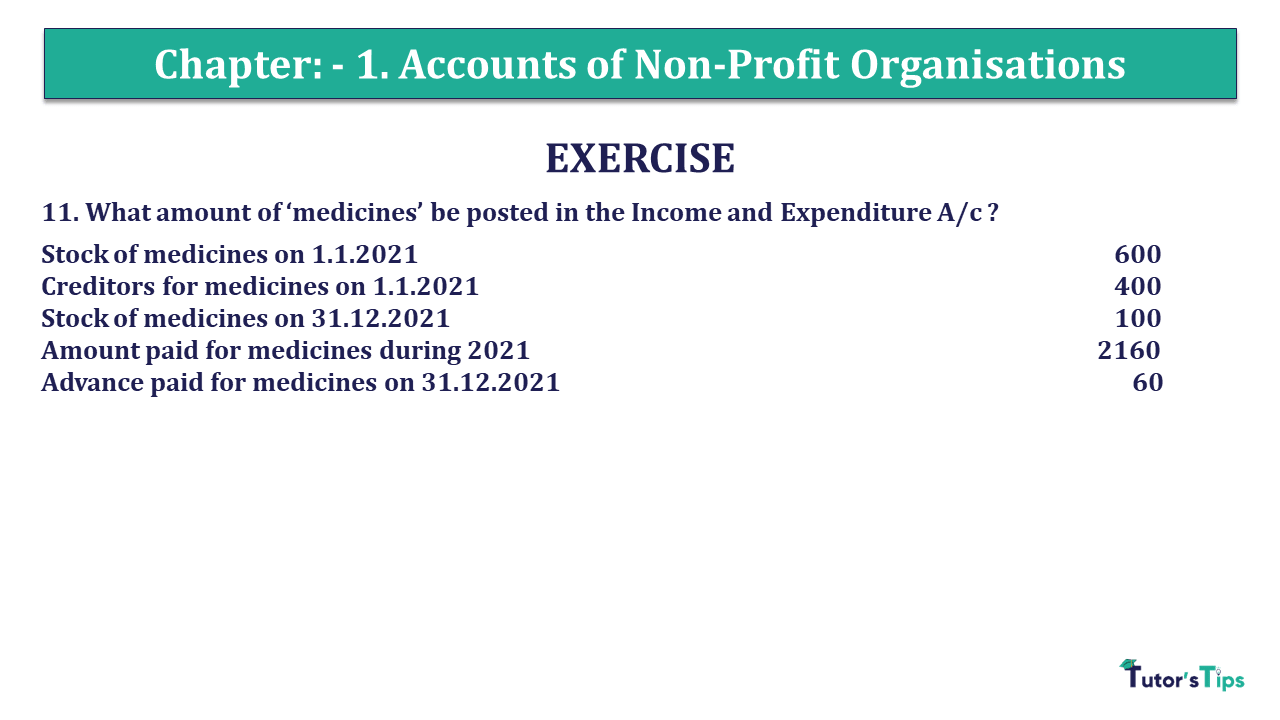

11. What amount of ‘medicines’ be posted in the Income and Expenditure A/c?

| The stock of medicines on 1.1.2021 | 600 |

| Creditors for medicines on 1.1.2021 | 400 |

| The stock of medicines on 31.12.2021 | 100 |

| Amount paid for medicines during 2021 | 2160 |

| Advance paid for medicines on 31.12.2021 | 60 |

The solution to Question 11 Chapter 1 – Unimax Class 12 Part 1:

| Particulars | Amount | |

| The stock of medicine as of 1 Jan. 2012 | 600 | |

| Add: – Amount paid for medicine during the year 2012 | 2160 | |

| Less: – Creditors for medicine as of 1st Jan. 2012 | 400 | |

| Less:-Stock of medicine as of 31st Dec. 2021 | 100 | |

| Less: – Advance paid for medicine as of 31st Dec. 2012 | 60 | 560 |

| Income from subscriptions during the year | 2200 | |

This is all about the Question 11 Chapter 1 – Unimax. You can check out the following article to better understand:

Not-for-Profit Organisations – Meaning and Overview

You Can also read all the above articles in Hindi on our Hindi Website

Not-for-Profit Organisations – Meaning and Overview – In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in Question 11 Chapter 1 – Unimax.

Also, Check out the solved question of all Chapters: –

Accountancy – Unimax Class 12 Part 1 – 2021 – Solution.

Chapter No. 1 – Accounts of Non-Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Basic Concepts)

Chapter No. 3 – Partnership Accounts – II (Goodwill)

Chapter No. 4 – Partnership Accounts – III (Change in Profit Sharing Ratio among Existing Partners)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

Chapter No. 1 – Accounting Not for Profit Organisations

Chapter No. 2 – Partnership Accounts – I (Introduction)

Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

Chapter No. 8 – Company Accounts (Share Capital)

Chapter No. 9 – Company Accounts (Issue of Debentures)

Chapter No. 10 – Company Accounts (Redemption of Debentures)

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures