Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

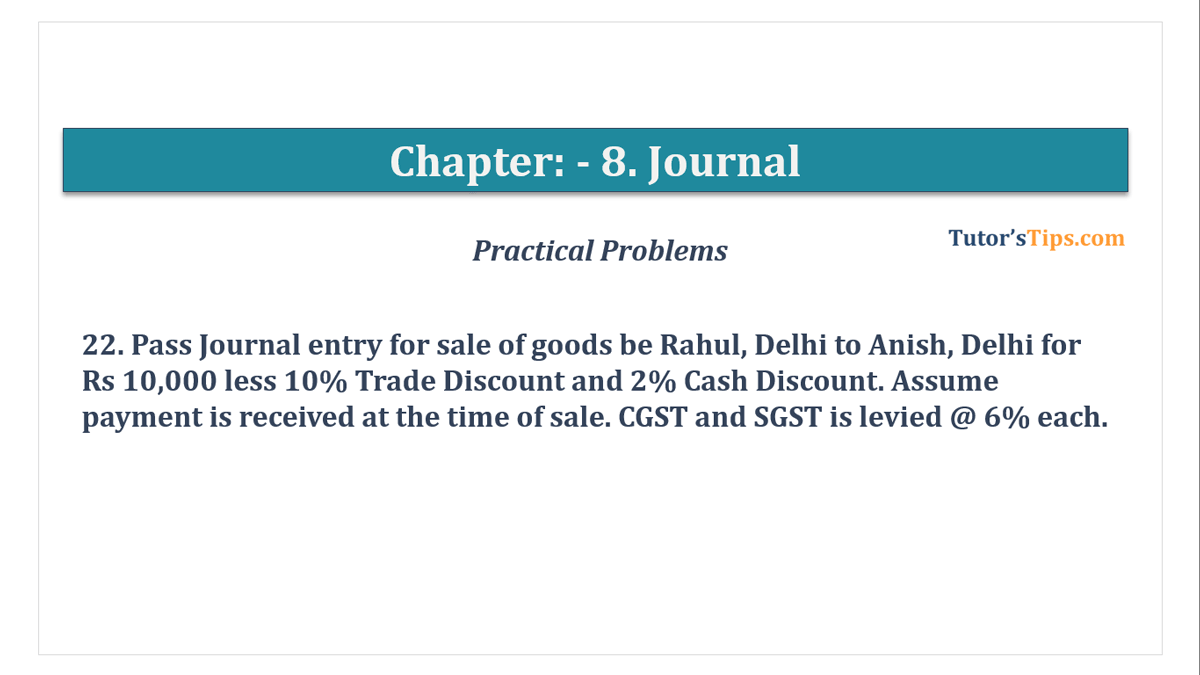

Question No 22 Chapter No 8

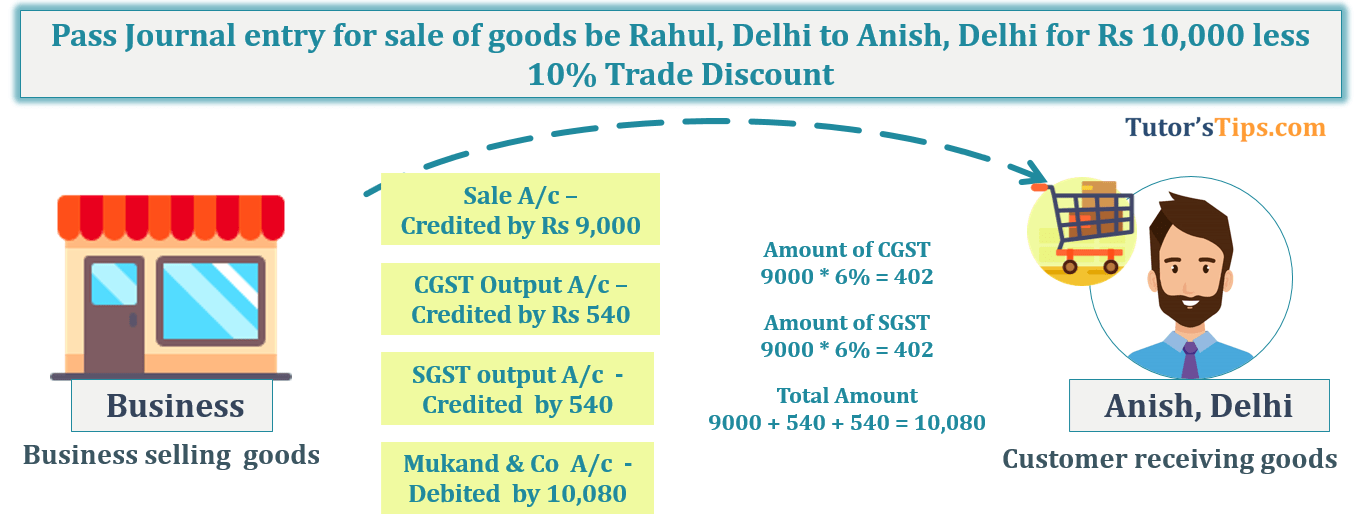

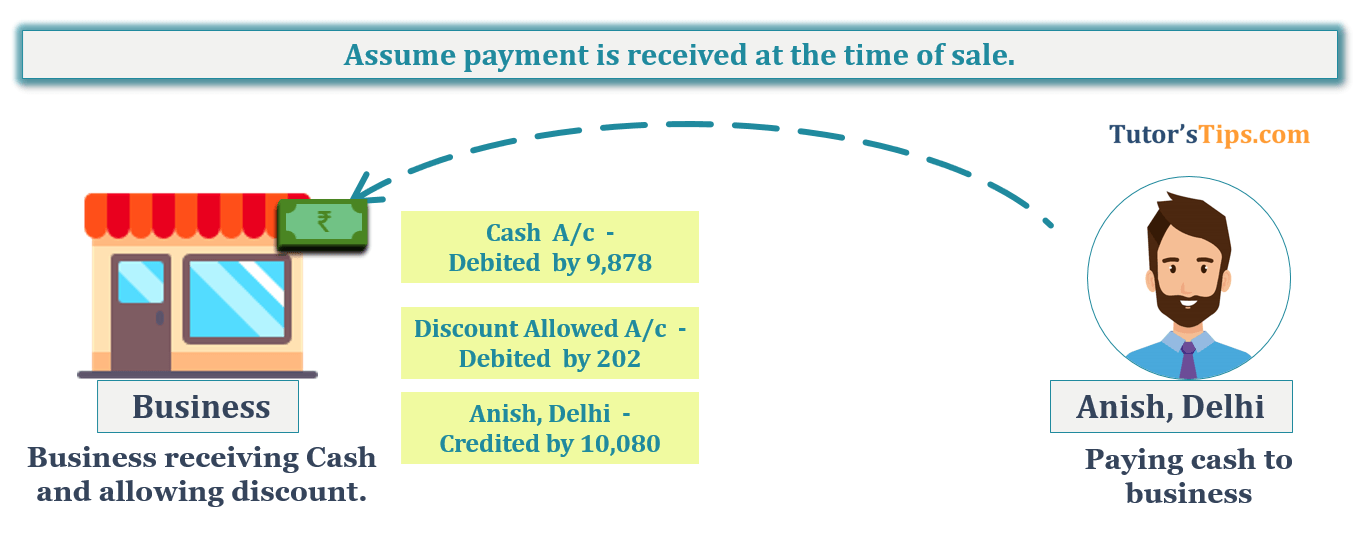

Pass Journal entry for sale of goods be Rahul, Delhi to Anish, Delhi for Rs 10,000 less 10% Trade Discount and 2% Cash Discount. Assume payment is received at the time of sale. CGST and SGST is levied @ 6% each.

Gross Sale Price = 10,000/-

Trade Discount = Sale Price * % of discount

= 10,000 * 10%

= 1,000/-

Net Sale Price = Gross Sale Price - Discount

= 10,000 – 1,000

= 9,000/-

Amount of CGST = Net Sale Price * % of CGST

= 9,000* 6%

= 5,40/-

Amount of SGST = Net Sale Price * % of SGST

= 9,000* 6%

= 5,40/-

Invoice Value = Net Purchase Price + CGST + SGST

= 9,000 + 540 + 540

= 10,080/-

Cash Discount = Invoice Value * % of Discount

= 10,080 * 2%

= 202/-

Cash discount always availed at the time of payment and trade discount is availed at the time of dealing/trading/ Negotiation. So, in this question, we can avail cash discount when payment is made within a specific time limit.

In the Books of M/s Vaish Trader, Delhi

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Anish, Delhi A/c | Dr. | 10,080 | |||

| To Sales A/c | 9,000 | ||||

| To Output CGST A/c | 540 | ||||

| To Output SGST A/c | 540 | ||||

| (Being goods sold to Anish, Delhi ) | |||||

| Cash A/c | Dr. | 9,878 | |||

| Discount Allowed A/c | Dr. | 202 | |||

| To Anish, Delhi A/c | 10080 | ||||

| (Being payment received from Anish, Delhi and allow him discount) | |||||

This is not a part of the solution, So you don't have to write it in the exam. So, why we explained if it is not needed. Because This explanation will help you to understand all transactions with logic and you don't need to remember all the transactions but just understand and remember the logic use behind it.

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|---|---|---|---|---|---|

| Anish, Delhi | Person | Personal Account | Goods received | He is receiver | Debit |

| Sales a/c (Goods) | Assets | Real Account | Goods giving by Business | Goods Goes out | Credit |

| CGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| SGST Output A/c | Income | Nominal Account | Tax collected from buyer | All income and gains | Credit |

| Name of Account | Type of Account | Rule which will Applicable | What happen in the transaction | Rule applied | According to Rule It will be |

|---|---|---|---|---|---|

| Cash | Assets | Real Account | Cash comes in | Comes in | Debit |

| Discount Allowed | Loss | Nominal Account | Loss of the business | All losses & Expenses | Debit |

| Anish, Delhi | Person | Personal Account | Making payment | He is giver | Credit |

Thanks Please share with your friends

Comment if you have any question.

Check out T.S. Grewal +1 Book 2019 @ Amazon.in

T.S. Grewal's Double Entry Book Keeping

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 22 Chapter No 8 - T.S. Grewal 11 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 11 Class Financial Accounting.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 22 Chapter No 8 - T.S. Grewal 11 Class" instantly.