⚡

Quick Overview & Key Takeaways

Focus Topic:Question No 38 Chapter No 19 - T.S. Grewal 11 Class

Estimated Reading Time:4 mins

- Comprehensive academic guide covering core concepts of Question No 38 Chapter No 19 - T.S. Grewal 11 Class.

- Syllabus-aligned study material with detailed definitions, formats, and practical examples.

- Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

Question No 38 Chapter No 19

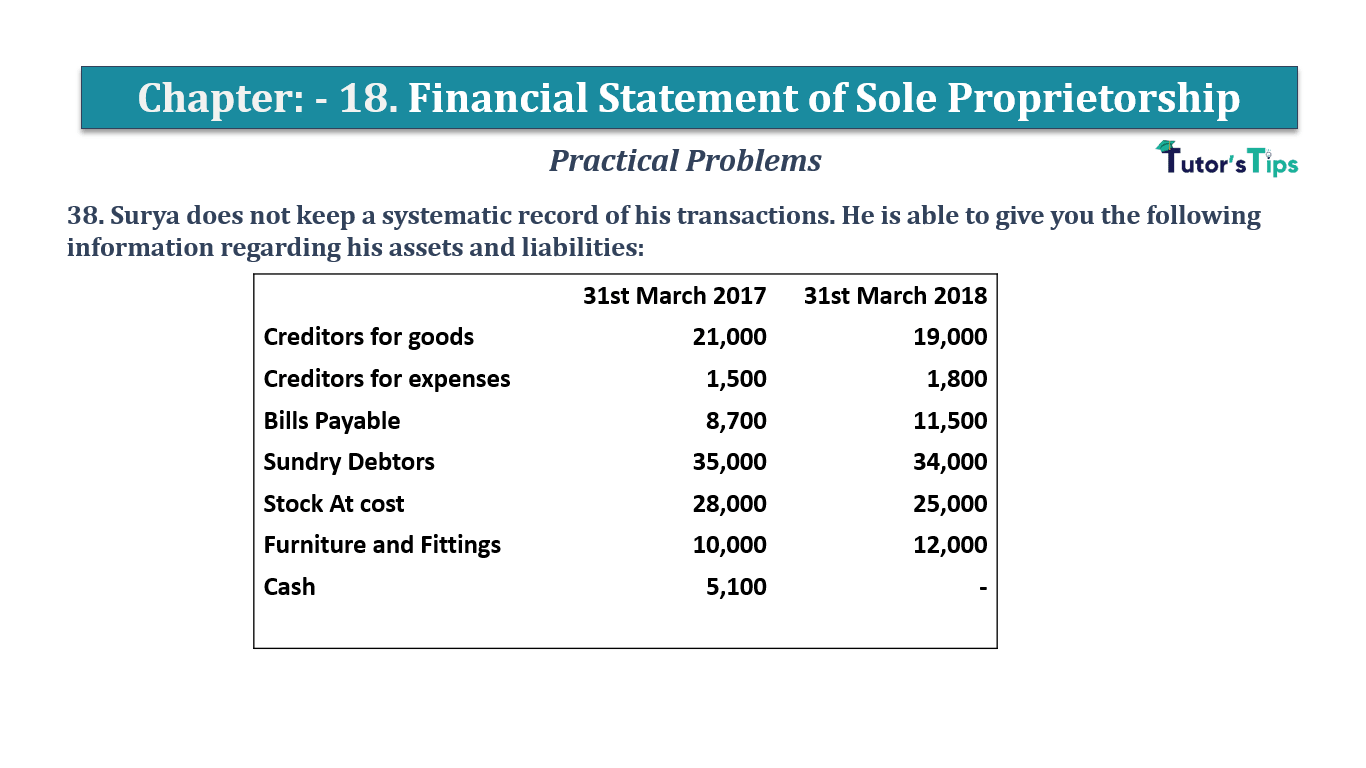

38. Surya does not keep a systematic record of his transactions. He is able to give you the following information regarding his assets and liabilities:

| |

31st March 2017 |

31st March 2018 |

| Creditors for goods |

21,000 |

19,000 |

| Creditors for expenses |

1,500 |

1,800 |

| Bills Payable |

8,700 |

11,500 |

| Sundry Debtors |

35,000 |

34,000 |

| Stock At cost |

28,000 |

25,000 |

| Furniture and Fittings |

10,000 |

12,000 |

| Cash |

5,100 |

- |

Following additional information is also available for the year ended 31st March, 2018:

| |

|

| Bills Payable Issued |

20,800 |

| Cash Sales |

15,000 |

| Payment to Sundry Creditors |

31,000 |

| Expenses paid |

6,600 |

| Drawings |

8,000 |

Bad Debts during the year were 900. As regards sale, Surya tells you that he always sells goods at Cost plus 25%. Furniture and Fittings are to be depreciated at 10% of the value in the beginning of the year. Prepare Surya's Trading and Profit and Loss Account for the year ended 31st March, 2018 and his Balance Sheet

The solution of Question No 38 Chapter No 19:-

Trading Account

Particular

|

Amount |

Particular

|

Amount |

| To Opening Stock |

|

28,000 |

By Sales |

15,000 + 51,000 |

66,000 |

| To Purchases |

|

49,800 |

By Closing Stock |

|

25,000 |

| To Gross Profit |

|

13,200 |

|

|

|

| |

|

91,000 |

|

|

91,000 |

Profit and Loss Account

Particular

|

Amount |

Particular

|

Amount |

| To Bad Debts |

|

900 |

By Gross Profit |

|

13,200 |

| To Expenses |

6,600 |

|

|

|

|

| Add: Closing Creditors for Expenses |

1,800 |

6,900 |

|

|

|

| To Depreciation on Furniture and Fittings |

|

1,000 |

|

|

|

| To Net Profit |

|

4,400 |

|

|

|

| |

|

13,200 |

|

|

13,200 |

Balance Sheet as on April 01, 2018

Particular

|

Amount |

Particular

|

Amount |

| Creditors for Goods |

|

19,000 |

Cash Balance |

|

4,600 |

| Creditors for Expenses |

|

1,800 |

Stock |

|

25,000 |

| Bills Payable |

|

11,500 |

Debtors |

|

34,000 |

| Capital |

46,900 |

|

Furniture and Fittings |

|

12,000 |

| Less: Drawings |

8,000 |

|

|

|

|

| Add: Net Profit |

4,400 |

43,300 |

|

|

|

| |

|

75,600 |

|

|

75,600 |

Balance Sheet as on April 01, 2017

Particular

|

Amount |

Particular

|

Amount |

| Creditors for Goods |

|

21,000 |

Cash Balance |

|

5,100 |

| Creditors for Expenses |

|

1,500 |

Stock |

|

28,000 |

| Bills Payable |

|

8,700 |

Debtors |

|

35,000 |

| Capital |

|

46,900 |

Furniture and Fittings |

|

10,000 |

| |

|

|

|

|

|

| |

|

78,100 |

|

|

78,100 |

Bank Account

Particular

|

Amount |

Particular

|

Amount |

| Balance b/d |

|

5,100 |

Expenses A/c |

|

6,600 |

| Debtors A/c |

|

51,100 |

Sundry Creditors A/c |

|

31,000 |

| Sales A/c |

|

15,000 |

Furniture and Fittings A/c |

|

3,000 |

| |

|

|

Bills Payable A/c |

|

18,000 |

| |

|

|

Drawings A/c |

|

8,000 |

| |

|

|

Balance c/d |

|

4,600 |

| |

|

71,200 |

|

|

71,200 |

Debtors Account

| Particular |

Amount |

Particular |

Amount |

| Balance b/d |

|

35,000 |

Bad Debts |

|

900 |

| |

|

|

Sales A/c Cash |

|

51,100 |

| Sales Credit A/c |

|

51,000 |

|

|

|

| |

|

|

|

|

|

| |

|

|

Balance c/d |

|

34,000 |

| |

|

3,00,000 |

|

|

3,00,000 |

Creditors Account

| Particular |

Amount |

Particular |

Amount |

| Bills Payable A/c |

|

20,800 |

Balance b/d |

|

21,000 |

| Cash A/c |

|

31,000 |

|

|

|

| |

|

|

|

|

|

| Balance c/d |

|

19,000 |

|

|

|

| |

|

|

Purchases A/c |

|

49,800 |

| |

|

70,800 |

|

|

70,800 |

Bills Payable Account

| Particular |

Amount |

Particular |

Amount |

| Cash |

|

18,000 |

Bad Debts |

|

8,700 |

| |

|

|

|

|

|

| |

|

|

|

|

|

| Balance c/d |

|

11,500 |

Creditors for goods |

|

20,800 |

| |

|

29,500 |

|

|

29,500 |

Furniture and Fittings Account

| Particular |

Amount |

Particular |

Amount |

| Balance b/d |

|

10,000 |

Depreciation |

|

1,000 |

| Cash A/c |

|

31,000 |

|

|

|

| |

|

|

Balance c/d |

|

12,000 |

| Cash-Purchases |

|

3,000 |

|

|

|

| |

|

70,800 |

|

|

70,800 |

Computation of Cost of Goods Sold and Credit Sales

| COGS |

= |

Opening. Stock + Purchases – closing. Stock |

| |

= |

28,000 + 49,800 – 25,000 |

| |

= |

52,800 |

| Gross Profit |

= |

52,800 × 25/100 |

| |

= |

13,200 |

| Total Sales |

= |

COGS + Gross Profit |

| |

= |

52,800 + 13,200 |

| |

= |

66,000 |

| Credit Sales |

= |

Total Sales – Cash Sales |

| |

= |

66,000 – 15,000 |

| |

= |

51,000 |

https://tutorstips.com/final-accounts/

https://tutorstips.com/profit-and-loss-account/

https://tutorstips.com/balance-sheet/

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: -

-

- Chapter No. 1 – Introduction to Accounting

- Chapter No. 2 – Basic Accounting Terms

- Chapter No. 3 – Theory Base of Accounting, Accounting Standards and International Financial Reporting Standards(IFRS)

- Chapter No. 4 – Bases of Accounting

- Chapter No. 5 – Accounting Equation

- Chapter No. 6 – Accounting Procedures – Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 7 – Origin of Transactions – Source Documents and Preparation of Vouchers

- Chapter No. 8 – Journal

- Chapter No. 9 – Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

- Chapter No. 11 – Special Purpose Books II – Other Books

- Chapter No. 12 – Bank Reconciliation Statement

- Chapter No. 13 – Trial Balance

- Chapter No. 14 – Depreciation

- Chapter No. 15 – Provisions and Reserves

- Chapter No. 16 – Accounting for Bills of Exchange

- Chapter No. 17 – Rectification of Errors

- Chapter No. 18 – Financial Statements of Sole Proprietorship

- Chapter No. 19 – Adjustments in preparation of Financial Statements

- Chapter No. 20 – Accounts from incomplete Records – Single Entry System

- Chapter No. 21 – Computers in Accounting

- Chapter No. 22 – Accounting Software – Tally

- Chapter No. 5 - Accounting Equation

- Chapter No. 6 - Accounting Procedures - Rules of Debit and Credit

- Goods and Services Tax(GST)

- Chapter No. 8 - Journal

- Chapter No. 9 - Ledger

- Chapter No. 10 – Special Purpose Books I – Cash Book

Check out T.S. Grewal +1 Book 2019 @ Official Website of Sultan Chand Publication

T.S. Grewal's Double Entry Book Keeping