Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

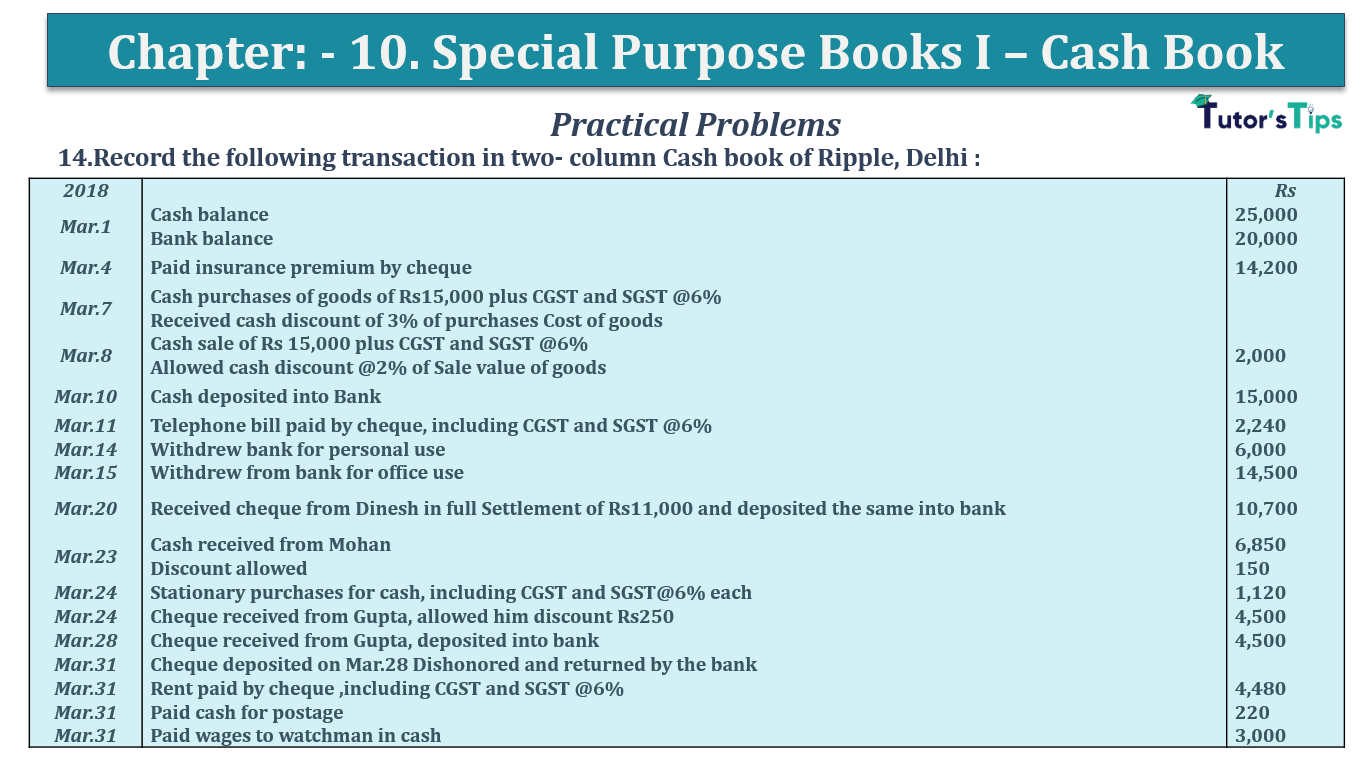

Question No 14 Chapter.

14.Record the following transaction in two-column Cashbook of Ripple, Delhi :

| 2018 | Rs | |

| Mar.1 | Cash balance | 25,000 |

| Bank balance | 20,000 | |

| Mar.4 | Paid insurance premium by cheque | 14,200 |

| Mar.7 | Cash purchases of goods of Rs15,000 plus CGST and SGST @6% | |

| Received cash discount of 3% of purchases Cost of goods | ||

| Mar.8 | Cash sale of Rs 15,000 plus CGST and SGST @6% | 2,000 |

| Allowed cash discount @2% of the Sale Value of goods | ||

| Mar.10 | Cash deposited into Bank | 15,000 |

| Mar.11 | Telephone bill paid by cheque, including CGST and SGST @6% | 2,240 |

| Mar.14 | Withdrew bank for personal use | 6,000 |

| Mar.15 | Withdrew from a bank for office use | 14,500 |

| Mar.20 | Received cheque from Dinesh in full Settlement of Rs11,000 and deposited the same into a bank | 10,700 |

| Mar.23 | Cash received from Mohan | 6,850 |

| Discount allowed | 150 | |

| Mar.24 | Stationary purchases for cash, including CGST and SGST@6% each | 1,120 |

| Mar.24 | Cheque received from Gupta, allowed him to discount Rs250 | 4,500 |

| Mar.28 | Cheque received from Gupta, deposited into bank | 4,500 |

| Mar.31 | Cheque deposited on Mar.28 Dishonored and returned by the bank | |

| Mar.31 | Rent paid by cheque, including CGST and SGST @6% | 4,480 |

| Mar.31 | Paid cash for postage | 220 |

| Mar.31 | Paid wages to the watchman in cash | 3,000 |

In the Books of Ripple, Delhi

| Dr. | Cash Book | Cr. | |||||||

| Date | Particulars |

L.F. | Cash | Bank | Date | Particulars |

L.F. | Cash | Bank |

|---|---|---|---|---|---|---|---|---|---|

| Mar. 2018 | Mar. 2018 | ||||||||

| 1 | To Balance B/d | 25,000 | 20,000 | 4 | By Insurance premium A/c | 14,200 | |||

| 8 | To Sale A/c | 14,664 | 7 | By Purchase A/c | 14,550 | ||||

| 8 | To Output CGST A/c | 900 | 7 | By Input CGST A/c | 900 | ||||

| 8 | To Output SGST A/c | 900 | 7 | By Input SGST A/c | 900 | ||||

| 10 | To Cash A/c | c | 15,000 | 10 | By Bank A/c | 15,000 | |||

| 15 | To Bank A/c | c | 14,500 | 11 | By Telephone bill A/c | 2,000 | |||

| 20 | To Dinesh A/c | 10,700 | 11 | By Input CGST A/c | 120 | ||||

| 23 | To Dinesh A/c | 6,850 | 11 | By Input SGST A/c | 120 | ||||

| 28 | To cheque in hand A/c | 4,500 | 14 | By Drawing A/c | 6,000 | ||||

| 15 | By Cash A/c | 14,500 | |||||||

| 24 | By Stationary A/c | 1,000 | |||||||

| 24 | By Input CGST A/c | 60 | |||||||

| 24 | By Input SGST A/c | 60 | |||||||

| 28 | By Gupta A/c | 4,500 | |||||||

| 31 | By Rent A/c | 4,000 | |||||||

| 31 | By Input CGST A/c | 240 | |||||||

| 31 | By Input SGST A/c | 240 | |||||||

| 31 | By Postage A/c | 220 | |||||||

| 31 | By wages A/c | 3,000 | |||||||

| 31 | By Balance C/d | 28,244 | 4,280 | ||||||

| 67,814 | 50,200 | 67,814 | 50,200 | ||||||

All transactions which are highlighted with (*) are explained as following as follows: -

*Oct. 2 Cash Sale Rs 60,000 plus CGST and SGST @6% each

The calculation of Amount of CGST and SGST @ 6% each

60,0000 * 12% = 7,200/-

*Oct. 9 Sale of goods of 10,000 plus CGST and SGST@6% each

The calculation of Amount of CGST and SGST @ 6% each

10,000 * 6% = 600/- each

*Oct. 18 Ramesh who owed Rs 5,000 became Bankrupt and Paid us 50 paise in a rupee

The calculation of the Amount of Bad Debts

5,000 X .50

2,500/-

*Oct. 27 Sold goods for Rs 11,000 Plus CGST and SGST @6% against Cash

The calculation of Amount of CGST and SGST @ 6% each

11,000 * 6% = 660/- each

*Oct. 28 Received a cheque for goods sold for Rs 9,000 plus CGST and SGST @6% each

The calculation of Amount of CGST and SGST @ 6% each

9,000 * 6% = 540/- each

To understand more about cash book please check out following links: -

https://tutorstips.com/cash-book/

https://tutorstips.com/single-column-cash-book/

https://tutorstips.com/double-column-cash-book/

https://tutorstips.com/triple-column-cash-book/

https://tutorstips.com/petty-cash-book/

Thanks Please share with your friends

Comment if you have any question.

Also, Check out previous Chapters: -

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

T.S. Grewal's Double Entry Book Keeping

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 14 Chapter No 10 - T.S. Grewal 11 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 11 Class Financial Accounting.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 14 Chapter No 10 - T.S. Grewal 11 Class" instantly.