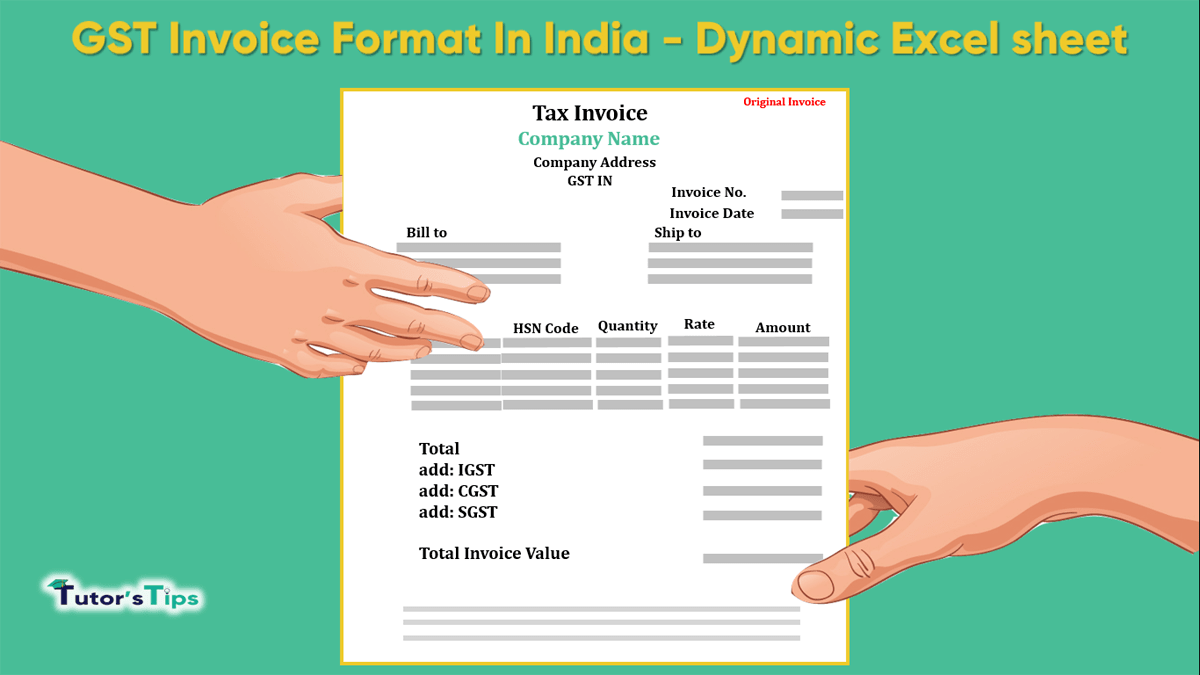

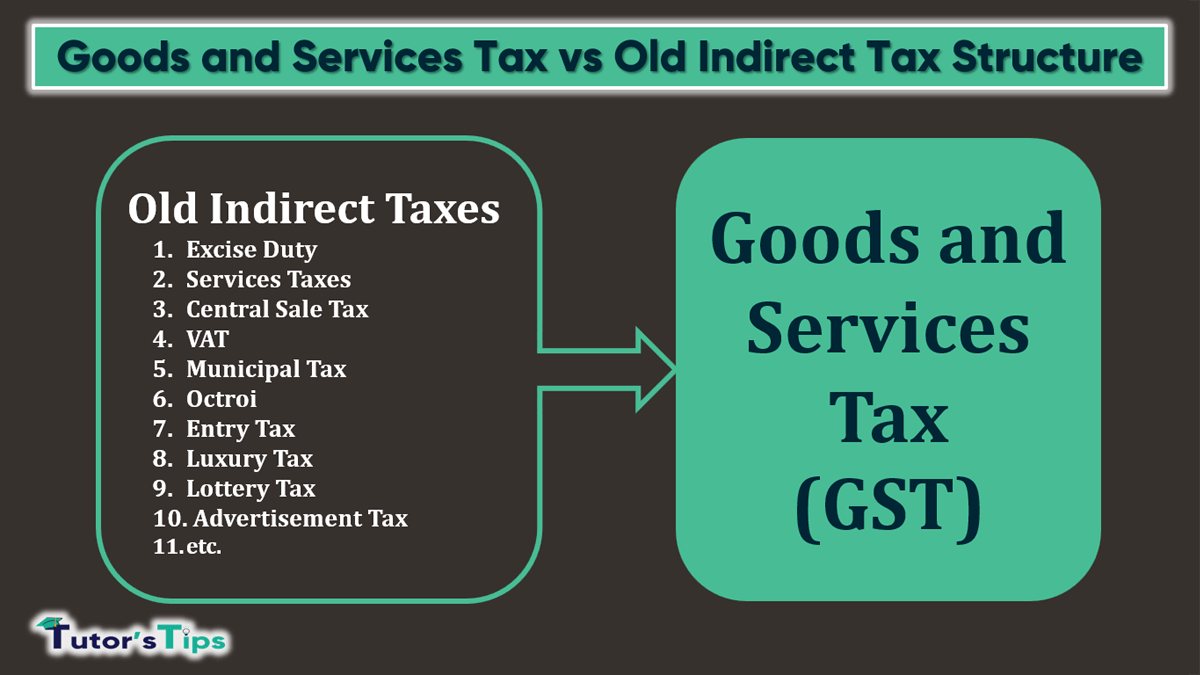

Focus Topic:Goods and Services Tax vs Old Indirect Tax Structure

Estimated Reading Time:4 mins

Comprehensive academic guide covering core concepts of Goods and Services Tax vs Old Indirect Tax Structure.

Syllabus-aligned study material with detailed definitions, formats, and practical examples.

Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

Goods and Services Tax vs Old Indirect Tax Structure: Here is the huge change made by govt. in new Indirect tax (GST) as compare with old Indirect Taxes. In old Indirect Tax, the structure has the major problem of cascading effects (It means the tax on tax).

The Cascading effects by old indirect taxes:

We will explain cascading effects by old indirect taxes by the following stage:

Stage 1-:

On the First stage, a manufacturer of Shoes will purchase raw material from anyone for Rs. 1,000 he has to pay 10% tax on it the total lending cost of raw material will be Rs. 1,100(cost=1,000 + tax=100).

Stage 2-:

On the second stage, a manufacturer sold their final product to wholesaler @ Rs 1,500/- (Cost to manufacturer = 1100 + manufacturing cost & profit= 400), Now Manufacturer has to pay tax @ 10% on the price of the product it means the total lending cost of the product is Rs. 1,650/- (Total price of product 1,500 + Taxes 150).

Stage 3-:

On the third stage, a wholesaler sold this product to trader @ Rs 2,000/- (Cost to wholesaler = 1650 + wholesaling cost & profit= 350), Now Wholesaler has to pay tax @ 10% on the price of the product it means the total lending cost of the product is Rs. 2,200/- (Total price of product 2,000 + Taxes 200).

Stage 4-:

On the Fourth stage, a Trader sold this product to Consumer @ Rs 2,500/- (Cost to trader = 2200 + Trader cost & profit= 300), Now Trader has to pay tax @ 10% on the price of the product it means the total lending cost of the product to Consumer is Rs. 2,750/- (Total price of product 2,500 + Taxes 250).

GST aims to solve this problem by introducing a seam-less Input Tax Credit (ITC).

Today, the tax that you pay on material purchases cannot be claimed from output tax. This is set to change with ITC.

The revival of Cascading effects by GST:

We will explain the revival of Cascading effect GST effects by following stages-:

Stage 1-:

On the First stage, a manufacturer of Shoes will purchase raw material from anyone for Rs. 1,000 he has to pay 10% tax on it the total lending cost of raw material will be Rs. 1,100(cost=1,000 + tax=100).

Stage 2-:

On the second stage, a manufacturer sold their final product to wholesaler @ Rs 1,500/- (Cost to manufacturer = 1100 + manufacturing cost & profit= 400), Now Manufacture has to pay tax @ 10% on only addition made in the product by him it means he has to pay 10% on Rs 400/- only (Tax = Rs 40/- only).

Stage 3-:

On the third stage, a wholesaler sold this product to trader @ Rs 2,000/- (Cost to wholesaler = 1540 + wholesaling cost & profit= 350), Now Wholesaler has to pay tax @ 10% on only in addition made by his in the price of the product (wholesaling cost & profit) by him it means he has to pay 10% on Rs 350/- only (Tax = Rs 35/- only).

Stage 4-:

On the Fourth stage, a Trader sold this product to Consumer @ Rs 2,500/- (Cost to trader = 2200 + Trader cost & profit= 300), Now Trader has to pay tax @ 10% on only on addition made by him in the price of the product (Trading cost & profit) by him it means he has to pay 10% on Rs 300/- only (Tax = Rs 30/- only).

The explanation of cascading effects with Table: -

We will explain cascading effects with the help of following tables and you can better understand the cascading effects with this:

Cascading Effects - Goods and Services Tax vs Old Indirect Tax Structure

Cascading Effects removed- Goods and Services Tax vs Old Indirect Tax structure in the end, the price of product reduced because of lower tax liability (Removing of cascading effect by GST). The final value of the Shoes also therefore reduced from INR 2750 to INR 2255, thus reducing the tax burden on the final customer.

So here is with the implementation of GST consumer will get the same product at a cheap price because it removing cascading effects on the price of products.

👤

Author & Educator

Sarbjit SinghB.Com and M.Com

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

❓ Frequently Asked Questions

What is the main topic of "Goods and Services Tax vs Old Indirect Tax Structure"?

This guide covers "Goods and Services Tax vs Old Indirect Tax Structure", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Goods and Services Tax (GST).

Who can benefit from this guide on "Goods and Services Tax vs Old Indirect Tax Structure"?

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

Where can I practice questions related to "Goods and Services Tax vs Old Indirect Tax Structure"?

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Goods and Services Tax vs Old Indirect Tax Structure" instantly.

Cascading Effects removed- Goods and Services Tax vs Old Indirect Tax structure in the end, the price of product reduced because of lower tax liability (Removing of cascading effect by GST). The final value of the Shoes also therefore reduced from INR 2750 to INR 2255, thus reducing the tax burden on the final customer.

So here is with the implementation of GST consumer will get the same product at a cheap price because it removing cascading effects on the price of products.

Cascading Effects removed- Goods and Services Tax vs Old Indirect Tax structure in the end, the price of product reduced because of lower tax liability (Removing of cascading effect by GST). The final value of the Shoes also therefore reduced from INR 2750 to INR 2255, thus reducing the tax burden on the final customer.

So here is with the implementation of GST consumer will get the same product at a cheap price because it removing cascading effects on the price of products.