Question 93 Chapter 8 of +2-A

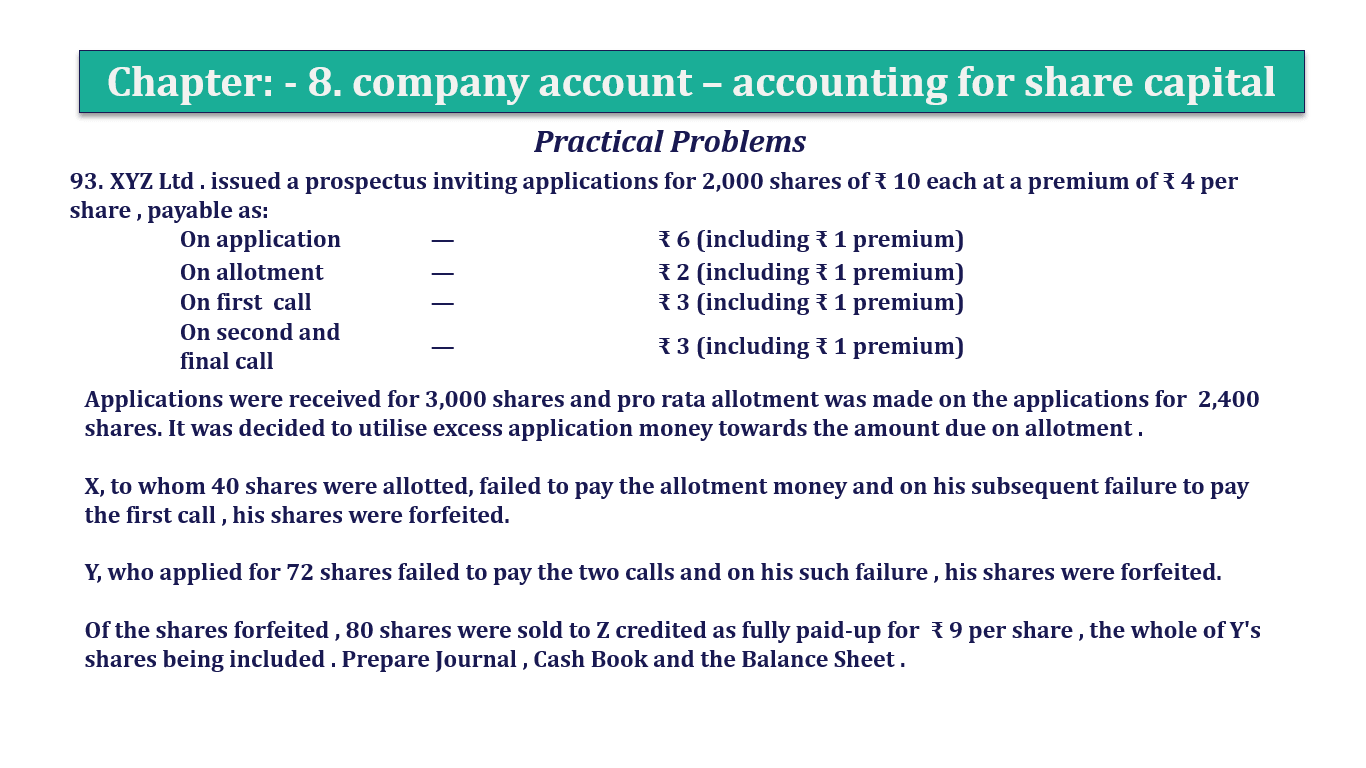

93. XYZ Ltd. issued a prospectus inviting applications for 2,000 shares of ₹ 10 each at a premium of ₹ 4 per share, payable as:

Applications were received for 2,40,000 shares and allotment was made as:

| On application | — | ₹ 6 (including ₹ 1 premium) |

| On allotment | — | ₹ 2 (including ₹ 1 premium) |

| On the first call | — | ₹ 3 (including ₹ 1 premium) |

| On the second and final call | — | ₹ 3 (including ₹ 1 premium) |

Applications were received for 3,000 shares and pro rata allotment was made on the applications for 2,400 shares. It was decided to utilise excess application money towards the amount due on allotment.

X, to whom 40 shares were allotted, failed to pay the allotment money and on his subsequent failure to pay the first call, his shares were forfeited.

Y, who applied for 72 shares failed to pay the two calls and on his such failure, his shares were forfeited. Of the shares forfeited, 80 shares were sold to Z credited as fully paid-up for ₹ 9 per share, the whole of Y’s shares being included. Prepare Journal, Cash Book and the Balance Sheet.

The solution of Question 93 Chapter 8 of +2-A: –

| Date | Particulars |

L.F. | Debit | Credit | |

| Share application A/c | Dr | 14,400 | |||

| To Share capital A/c | 10,000 | ||||

| To Securities premium A/c | 2,000 | ||||

| To share allotment A/c | 2,400 | ||||

| (Being application money transferred to equity share capital ) | |||||

| Share allotment A/c | Dr | 4,000 | |||

| To Share capital A/c | 2,000 | ||||

| To Securities premium A/c | 2,000 | ||||

| (Being the allotment money due ) | |||||

| (Being share forfeited ) | |||||

| Share first call A/c | Dr | 6,000 | |||

| To Share capital A/c | 4,000 | ||||

| To Securities premium A/c | 2,000 | ||||

| (Being the first call money due ) | |||||

| Share capital A/c | Dr | 320 | |||

| Securities premium A/c | Dr | 72 | |||

| To share forfeiture A/c | 240 | ||||

| To share allotment A/c | 32 | ||||

| To share first call A/c | 120 | ||||

| (Being share forfeited ) | |||||

| Share final call A/c | Dr | 5,880 | |||

| To Share capital A/c | 3,920 | ||||

| To Securities premium A/c | 1,960 | ||||

| (Being the allotment money due ) | |||||

| Share capital A/c | Dr | 600 | |||

| Securities premium A/c | Dr | 120 | |||

| To share forfeiture A/c | 360 | ||||

| To share final call A/c | 360 | ||||

| (Being share forfeited ) | |||||

| Share final call A/c | Dr | 1,98,100 | |||

| To Share capital A/c | 1,98,100 | ||||

| (Being the final call money due ) | |||||

| Share Forfeiture A/c | Dr | 720 | |||

| Share Forfeiture A/c | Dr | 80 | |||

| To share capital A/c | 800 | ||||

| (Being forfeited share reissue ) | |||||

| Share forfeiture A/c | Dr | 400 | |||

| To capital Reserve A/c | 400 | ||||

| (Being the gain on reissue transferred to capital reserve ) | |||||

| Particulars |

Details |

Amount |

| I. Equity and Liabilities | ||

| 1. Shareholders’ Funds | ||

| (a) Share Capital | ||

| (b) Reserves and Surplus | 19,920 | |

| (c) Money Received against Share Warrants | 8,168 | |

| 2. Share Application Money Pending Allotment | ||

| 3. Non-Current Liabilities | ||

| 4. Current Liabilities | ||

| Total | 28,088 | |

| II. Assets | ||

| 1.Non-Current Assets | ||

| (a) Fixed Assets | ||

| Tangible Assets | ||

| 2. Current Assets | ||

| (d) Cash and Cash equivalents | 28,088 | |

| Total | 28,088 |

| Particulars |

Details |

Amount |

| Share capital | ||

| Authorized capital | ||

| 25,000 Equity share of Rs 10each | – | |

| Issued capital | ||

| 2,000 equity shares of Rs 10 each | 20,000 | |

| Subscribed capital | ||

| Subscribed and fully paid-up | ||

| 1,980 Equity shares of Rs10 each + share forefeitur (120 ) | 19,920 | |

| Capital reserve | 400 | |

| Building | 7,768 | |

| Cash at bank | 28,088 |

Working notes –

| No of share allotted | = | 2,400 | * 40 | = | 48shares |

| 2,000 |

| Amount | |

| Money received on application(48 shares * Rs 6) | 288 |

| Less: Application money transferred to share capital (40 * Rs 5) | (200) |

| Excess received on the application | 88 |

| Amount | |

| Amount due on allotment | 3,600 |

| Less: Excess money on application | (1500) |

| Calls in arrears on the allotment | 2,100 |

| Amount | |

| Money due an allotment (2,00,000 *Rs 5 ) | 4,000 |

| Less: excess money on application | (2,400) |

| Less: calls in arrear on X share + calls in arrear on Y share | (1632) |

| Money received on Allotment | 1,568 |

| No of share allotted | = | 2,000 | * 72 | = | 60 shares |

| 2,400 |

| Capital reserve | Amount |

| Money due on the first call (2,000 * Rs 3) | 6,000 |

| Less: calls in arrear for Ramesh (40 *Rs 3) | (120) |

| Less: calls in arrear on Rajesh (60* Rs 3) | (180) |

| Money received on the first call | 5,700 |

| Share final call | Amount |

| Money due on first call | 5,880 |

| Less : calls in arrear on Rajesh | (180) |

| Money received on Final call | 5,700 |

capital reserve on X share & Y share

| Capital reserve | Amount |

| Share forfeiture Cr. | 120 |

| Less: share forfeiture Dr. | (20) |

| Capital reserve of 1,000 shares (X share) | 100 |

| Capital reserve | Amount |

| Share forfeiture Cr. | 360 |

| Less: share forfeiture Dr. | (60) |

| Capital reserve of share ( Y share ) | 300 |

Total Capital Reserve on 60 shares = Re-issued shares of X + Re-issued shares of Y= 100 + 300 = Rs.100

Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

T

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication