Question 59 Chapter 8 of +2-A

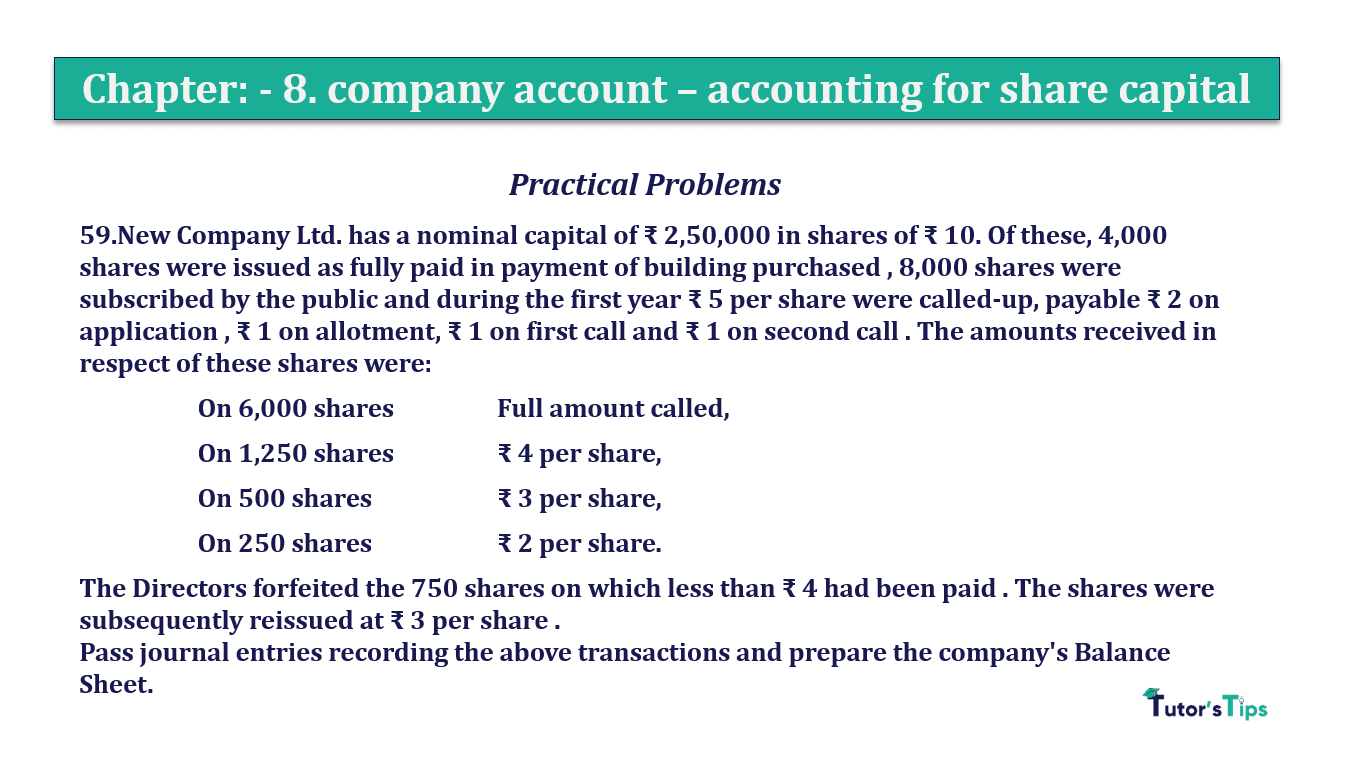

59. New Company Ltd. has a nominal capital of ₹ 2,50,000 in shares of ₹ 10. Of these, 4,000 shares were issued as fully paid in payment of building purchased, 8,000 shares were subscribed by the public and during the first year ₹ 5 per share were called-up, payable ₹ 2 on the application , ₹ 1 on the allotment, ₹ 1 on the first call and ₹ 1 on the second call. The amounts received in respect of these shares were:

| On 6,000 shares | The full amount called, |

| On 1,250 shares | ₹ 4 per share, |

| On 500 shares | ₹ 3 per share, |

| On 250 shares | ₹ 2 per share. |

The Directors forfeited the 750 shares on which less than ₹ 4 had been paid. The shares were subsequently reissued at ₹ 3 per share.

Pass journal entries recording the above transactions and prepare the company’s Balance Sheet.

The solution of Question 59 Chapter 8 of +2-A: –

| Date | Particulars |

L.F. | Debit | Credit | |

| Building A/c | Dr | 40,000 | |||

| To Vendor A/c | 40,000 | ||||

| (Being building purchased ) | |||||

| Vendor A/c | Dr | 40,000 | |||

| To Share capital A/c | 40,000 | ||||

| (Being application money transferred to equity share capital ) | |||||

| Bank A/c | Dr | 16,000 | |||

| To Share application A/c | 16,000 | ||||

| (Being the application money received. ) | |||||

| Share Application A/c | Dr | 16,000 | |||

| To Share Capital A/c | 16,000 | ||||

| (Being application money transferred to equity share capital ) | |||||

| Share allotment A/c | Dr | 8,000 | |||

| To Share capital A/c | 8,000 | ||||

| (Being the first call money due ) | |||||

| Bank A/c | Dr | 7,750 | |||

| Calls in arrear A/c | Dr | 250 | |||

| To Share allotment A/c | 8,000 | ||||

| (Being first call money received ) | |||||

| Share first call A/c | Dr | 8,000 | |||

| To Share capital A/c | 8,000 | ||||

| (Being share forfeited ) | |||||

| Bank A/c | Dr | 7,750 | |||

| Calls in arrear A/c | Dr | 250 | |||

| To Share capital A/c | 8,000 | ||||

| (Being the final call money due ) | |||||

| Bank A/c | Dr | 37,400 | |||

| Calls in arrear A/c | Dr | 600 | |||

| To Share final call A/c | 38,000 | ||||

| (Being first call money received) | |||||

| Share the second call A/c | Dr | 8,000 | |||

| To Share capital A/c | 8,000 | ||||

| (Being the second call money due ) | |||||

| Bank A/c | Dr | 6,000 | |||

| Calls in arrear A/c | Dr | 2,000 | |||

| To capital Reserve A/c | 8,000 | ||||

| (Being second call money received ) | |||||

| Share capital A/c | Dr | 3,750 | |||

| To Share forfeiture A/c | 2,000 | ||||

| To calls in arrear A/c | 1,750 | ||||

| (Being share forfeited ) | |||||

| Bank A/c | Dr | 2,250 | |||

| Forfeited share A/c | Dr | 1,500 | |||

| To Share capital A/c | 3,750 | ||||

| (Being forfeited share reissue ) | |||||

| Share forfeiture A/c | Dr | 500 | |||

| To capital reserve A/c | 500 | ||||

| (Being balance in share forfeiture account transferred to capital Reserve ) | |||||

| Particulars |

Details |

Amount |

| I. Equity and Liabilities | ||

| 1. Shareholders’ Funds | ||

| (a) Share Capital | ||

| (b) Reserves and Surplus | 78,750 | |

| (c) Money Received against Share Warrants | 500 | |

| 2. Share Application Money Pending Allotment | ||

| 3. Non-Current Liabilities | ||

| 4. Current Liabilities | ||

| Total | 79,250 | |

| II. Assets | ||

| 1.Non-Current Assets | ||

| (a) Fixed Assets | ||

| Tangible Assets | 40,000 | |

| 2. Current Assets | ||

| (d) Cash and Cash equivalents | 39,250 | |

| Total | 79,250 |

| Particulars |

Details |

Amount |

| Share capital | ||

| Authorized capital | ||

| 25,000 Equity share of Rs 10each | 2,50,000 | |

| Issued capital | ||

| 12,000 equity shares of Rs 10 each | 1,20,000 | |

| Subscribed capital | ||

| Subscribed and fully paid-up | ||

| 4,000 Equity shares of Rs10 every 8,000 shares of 5 called up- calls in arrear (1,250) | 78,750 | |

| Capital reserve | 500 | |

| Building | 40,000 | |

| Cash at bank | 2,02,000 |

| Calculation of capital reserve | |||

| Particulars |

Details | Amount | |

| Calls-in-Arrears on Allotment (250 shares × Rs.1) | 250 | ||

| Calls-in-Arrears on First Call (750 shares × Rs.1) | 750 | ||

| Calls-in-Arrears on Second Call (2,000 shares × Rs.1) | 2,000 | ||

| Total Calls-in-Arrears Debit | 3,000 | ||

| Less: Calls-in-Arrears Credit (at the time of forfeiture) | (1,750) | ||

| Calls-in-Arrears to be shown in the Balance Sheet | 1250 | ||

| Particulars |

Details | Amount | |

| Share Forfeiture of 250 shares Cr.(on which 2 per share paid) | 500 | ||

| Share Forfeiture of 500 shares Cr. (on which 3 per share) | 1,500 | ||

| Total Share Forfeiture credit Cr.(on 750 shares) | 2,000 | ||

Total Share Forfeiture Cr.(on 750 shares) – Share Forfeiture Dr.(750 shares × Rs.2 per share)

= Rs.2,000 – Rs.1,500 = Rs.500

Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication