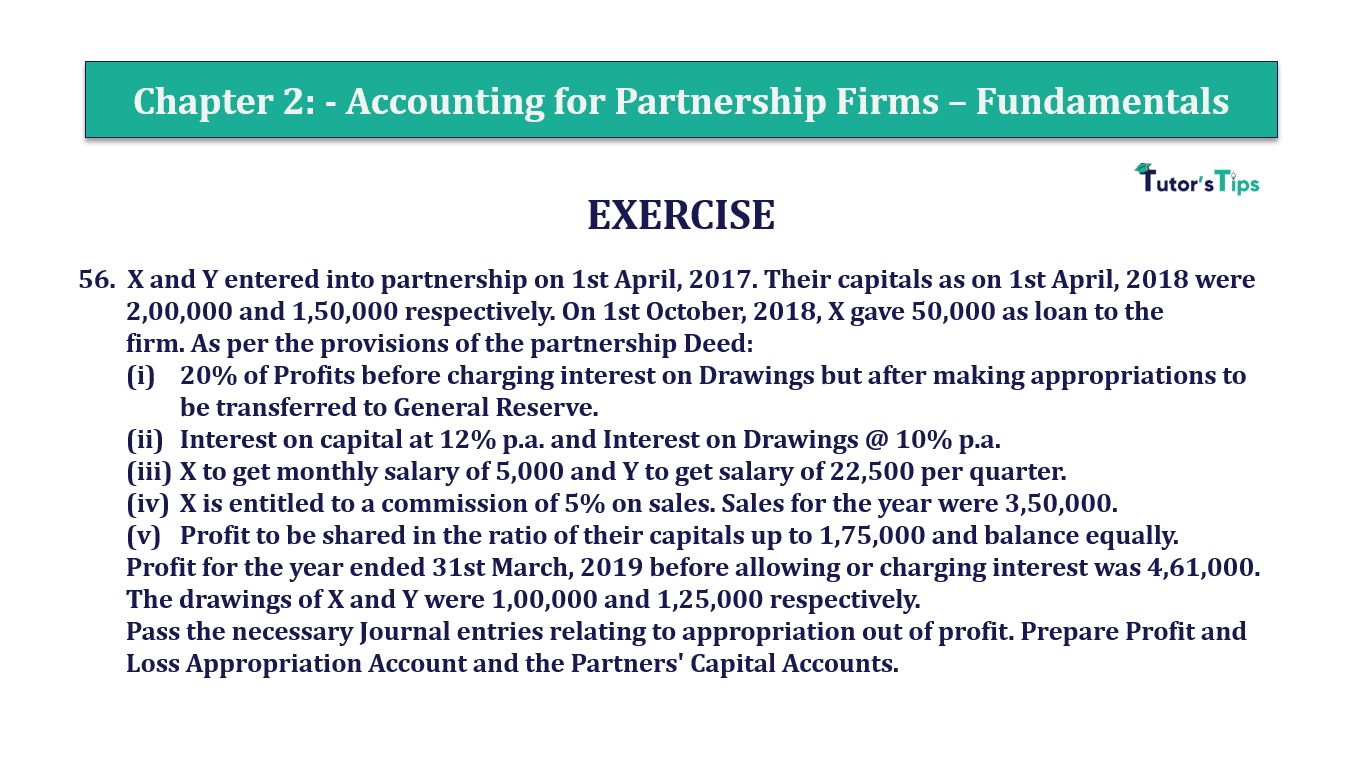

Question 56 Chapter 2 of +2-A

56. X and Y entered into a partnership on 1st April 2017. Their capitals as on 1st April, 2018 were 2,00,000 and 1,50,000 respectively. On 1st October 2018, X gave 50,000 as a loan to the firm. As per the provisions of the partnership deed:

- 20% of Profits before charging interest on Drawings but after making appropriations to be transferred to General Reserve.

- Interest on capital at 12% p.a. and Interest on Drawings @ 10% p.a.

X to get a monthly salary of 5,000 and Y to get the salary of 22,500 per quarter. - X is entitled to a commission of 5% on sales. Sales for the year were 3,50,000.

- Profit to be shared in the ratio of their capitals up to 1,75,000 and balance equally.

- Profit for the year ended 31st March 2019 before allowing or charging interest was 4,61,000. The drawings of X and Y were 1,00,000 and 1,25,000 respectively.

The solution of Question 56 Chapter 2 of +2-A:

| Profit and Loss Appropriation Account for the year ended 31st March 2019 |

||||||

| Expenditure |

Amount | Income |

Amount | |||

| To Interest on Capital A/c *1 | By Profit and Loss A/c | 4,59,500 | ||||

| X’s Capital A/c | 24,000 | |||||

| Y’s Capital A/c | 18,000 | 42,000 | ||||

| To Commission to Y A/c *2 | 17,500 | |||||

| To X’s Salary A/ c (5,000 ×12) | 60,000 | |||||

| To Y’s Salary A/c (5,000 ×12) | 90,000 | |||||

| To Reserve A/c *3 | 50,000 | |||||

| To Profit Transferred to *4 | ||||||

| X’s Current A/c | 1,18,125 | |||||

| Y’s Current A/c | 93,125 | 2,11,250 | ||||

| 4,59,500 | 4,59,500 | |||||

| Partners’ Capital Accounts for the year ended 31st March 2019 |

|||||

| Particulars | X | Y |

Particulars |

X | Y |

| To Drawings A/c | 1,00,000 | 1,25,000 | By Balance B/d | 2,00,000 | 1,50,000 |

| To Interest on Drawings A/c | 5,000 | 6,250 | By Interest on Capital A/c *1 | 24,000 | 18,000 |

| By Salaries A/c | 60,000 | 90,000 | |||

| By Commission A/c *2 | 17,500 | – | |||

| By P&L Appropriation A/c*4 | 1,18,125 | 93,125 | |||

| To Balance c/d | 3,14,625 |

2,19,875 |

|||

| 4,19,625 |

3,51,125 |

4,19,625 |

3,51,125 |

||

Working Note: –

*1 Calculation of Interest on X’s, Y’s, & Cherry’s Capital

Interest on Capital = Opening Capital X Rate of Interest

| Interest on X’s Capital | = | 2,00,000 | X | 5 |

| 100 |

Interest on X’s Capital = 24,000/-

| Interest on Y’s Capital | = | 1,50,000 | X | 5 |

| 100 |

Interest on Y’s Capital = 18,000/-

*2 Calculation of Commission to X

| Commission to X | = | 5% on Sales |

| Sales | = | 3,50,000 |

| Commission to X | = | Sales | X | Rate |

| 100 |

| Commission to X | = | 3,50,000 | X | 5 |

| 100 |

Commission to X = 17,500/-

*3 Calculation of Amount to be transferred to Reserve

| Amount for Reserve | = | 10% of Divisible Profit |

| Divisible Profit | = | Profit – Interest on Capital – Partners’ Commission – Partners’ Salary |

| = | 4,59,500 − 42,000 −17,500 − 60,000 − 90,000= Rs = 2,50,000 |

| Amount of Reserve | = | 2,50,000 | X | 20 |

| 100 |

Amount of Reserve = 50,000/-

*4 Calculation of Interest on X’s, Y’s, & Cherry’s Drawing

Interest on Drawing = Total Drawing X Rate of Interest X Period

| Interest on X’s Drawing | = | 1,00,000 | X | 10 | X | 6 |

| 100 | 12 |

Interest on X’s Drawing = 5,000/-

| Interest on Y’s Drawing | = | 1,25,000 | X | 10 | X | 6 |

| 100 | 12 |

Interest on Y’s Drawing = 6,250/-

*5: -Calculation of share of profit of X’s & Y’s

Net Profit after interest & Salary = 2,11,250

Distribution of first Rs 1,75,000 in the Capital Ratio 2,00,000 : 1,50,000 i.e. 4 : 3

| Profit share of X | = | 1,75,000 X 4/7 |

| Profit share of X | = | 1,00,000/- |

| Profit share of Y | = | 1,75,000 X 3/7 |

| Profit share of Y | = | 75,000/- |

Distribution of remaining profit in the ratio of 1:1

Remaining Profit available for distribution = Rs 2,11,250 − 1,75,000 = Rs 36,250

| Profit share of X | = | 36,250 X 1/2 |

| Profit share of X | = | 18,125/- |

| Profit share of Y | = | 36,250 X 1/2 |

| Profit share of Y | = | 18,125/- |

Total Profit Share of X = 1,00,000 + 18,125 = Rs 1,18,125

Total Profit Share of Y = 75,000 + 18,125 = Rs 93,125

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication