Question 44 Chapter 5 of +2-B

Table of Contents

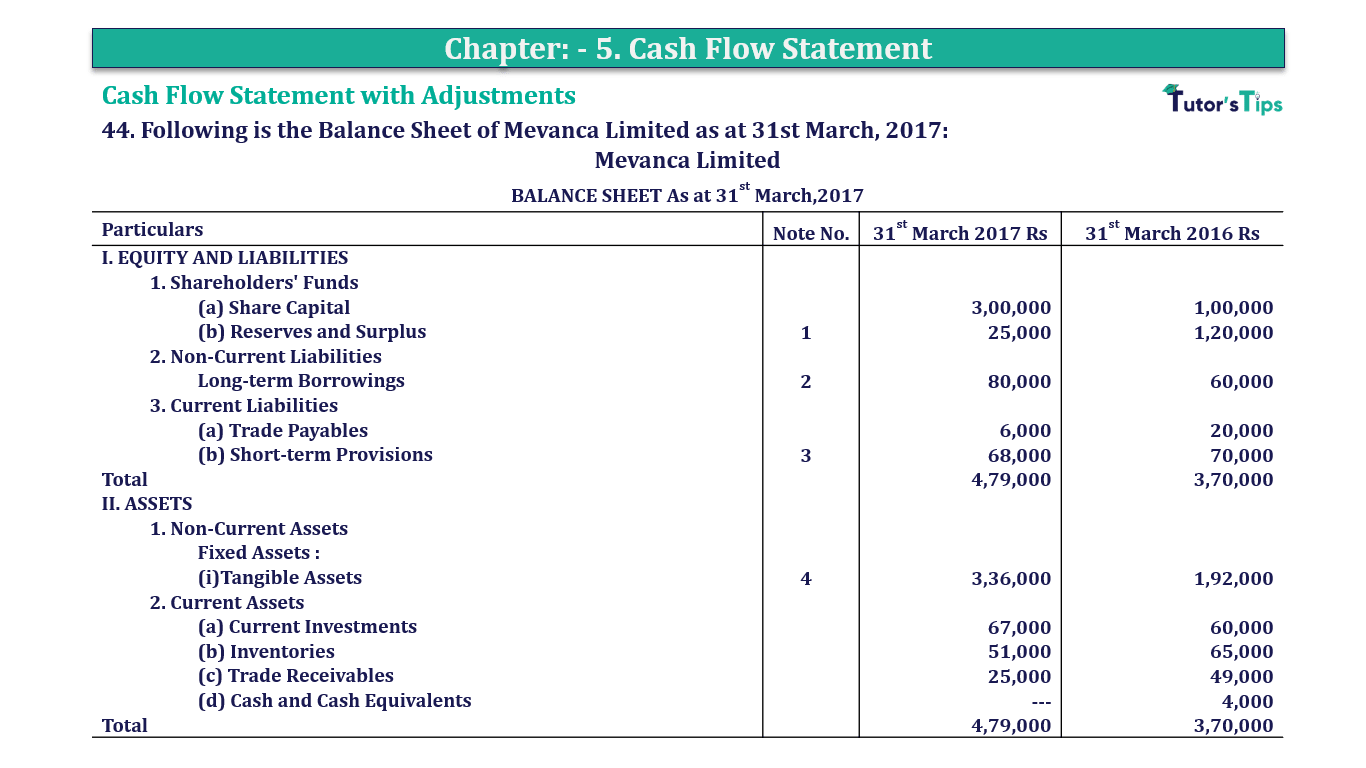

44. Following is the Balance Sheet of Mevanca Limited as at 31st March 2017:

| Mevanca Limited | |||

| BALANCE SHEET As at 31st March 2017 | |||

| Particulars | Note No. | 31st March 2017 Rs |

31st March 2016 Rs |

| I. EQUITY AND LIABILITIES | |||

| 1. Shareholders’ Funds | |||

| (a) Share Capital | 3,00,000 | 1,00,000 | |

| (b) Reserves and Surplus | 1 | 25,000 | 1,20,000 |

| 2. Non-Current Liabilities | |||

| Long-term Borrowings | 2 | 80,000 | 60,000 |

| 3. Current Liabilities | |||

| (a) Trade Payables | 6,000 | 20,000 | |

| (b) Short-term Provisions | 3 | 68,000 | 70,000 |

| Total | 4,79,000 | 3,70,000 | |

| II. ASSETS | |||

| 1. Non-Current Assets | |||

| Fixed Assets : | |||

| (i)Tangible Assets | 4 | 3,36,000 | 1,92,000 |

| 2. Current Assets | |||

| (a) Current Investments | 67,000 | 60,000 | |

| (b) Inventories | 51,000 | 65,000 | |

| (c) Trade Receivables | 25,000 | 49,000 | |

| (d) Cash and Cash Equivalents | — | 4,000 | |

| Total | 4,79,000 | 3,70,000 | |

Notes to Accounts

| Particulars | 31st March, 2017 (Rs) | 31st March 2016 (Rs) |

| 1. Reserves and Surplus | ||

| Surplus, i.e., Balance in Statement of Profit and Loss | 25,000 | 1,20,000 |

| 2. Long-term Borrowings | ||

| 10% Long-term Loan | 80,000 | 60,000 |

| 3. Short-term Provisions | ||

| Provision for Tax | 68,000 | 70,000 |

| 4. Fixed Assets | 3,84,000 | 2,15,000 |

| Machinery | -48,000 | -23,000 |

| Accumulated Depreciation | 3,36,000 | 1,92,000 |

Additional Information:

(i) Additional loan was taken on 1st July, 2016.

(ii) Tax of 53,000 was paid during the year.

Prepare Cash Flow Statement.

The solution of Question 44 Chapter 4 of +2-B: –

Cash Flow Statement for the year ended 31st March,2013 |

||

| Particulars |

Rs |

|

| I. Cash Flow from Financing Activities | ||

| Net Loss as per Statement of Profit and Loss | (95,000) | |

| Add: Provision for Tax | 51,000 | 44,000 |

| Net loss before Tax and Extraordinary Items | (44,000) | |

| Items to be Added: | ||

| Depreciation charged during the year | 25,000 | |

| Interest paid on loan (WN I) | 7,500 | |

| Net Loss before Working Capital Changes | (11,500) | |

| Less: Decrease in Current Liabilities | ||

| Trade Payables | 14,000 | |

| Less: Increase in Current Assets | ||

| Inventories | 7,000 | |

| Add: Decrease in Current Assets | ||

| Trade Receivables | 14,000 | |

| Other Current Assets | 4,000 | (14,500) |

| Net Loss before Tax | (14,500) | |

| Add: Tax paid | 53,000 | |

| Net Cash Flow from Operating Activities | 67,500 | |

| II. Cash Flow from Financing Activities | ||

| Purchase of Machinery (WN II) | 1,69,000 | |

| Net Cash Used in Investing Activities | 1,69,000 | |

| III: Cash Flow from Financing Activities | ||

| Proceeds from Issue of Shares | 2,00,000 | |

| Proceeds from additional loan taken | 20,000 | |

| Less: Interest paid on long-term loan | 7,500 | 2,12,500 |

| Net Cash Flow from Financing Activities | 2,12,500 | |

| IV. Net Decrease in Cash and Cash Equivalents |

(24,000) | |

| Add: Cash and Cash Equivalents in the beginning of the period |

49,000 |

|

| Cash and Cash Equivalents at the end of the period |

25,000 | |

Working Note

| Provision for Tax A/c |

|||

| Particulars |

Rs | Particular | Rs |

| To Cash A/c | 32,000 | By Balance b/d | 70,000 |

| To Balance c/d | 68,000 | By Profit and Loss A/c (Dep. charged during the year) (Bal. Fig.) | 51,000 |

| 1,21,000 | 1,21,000 | ||

Interest on Loan Rs 20,000 Calculated from 1st July, 2016

| Interest on Loan |

= | 10% | ||||

| * Interest on Bank Loan | = | Rs 20,000 | X | 10% | X | 9 |

| 12 | ||||||

| = | Rs 1,500 |

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication