Question 42 Chapter 2 – Unimax Class 12 Part 1

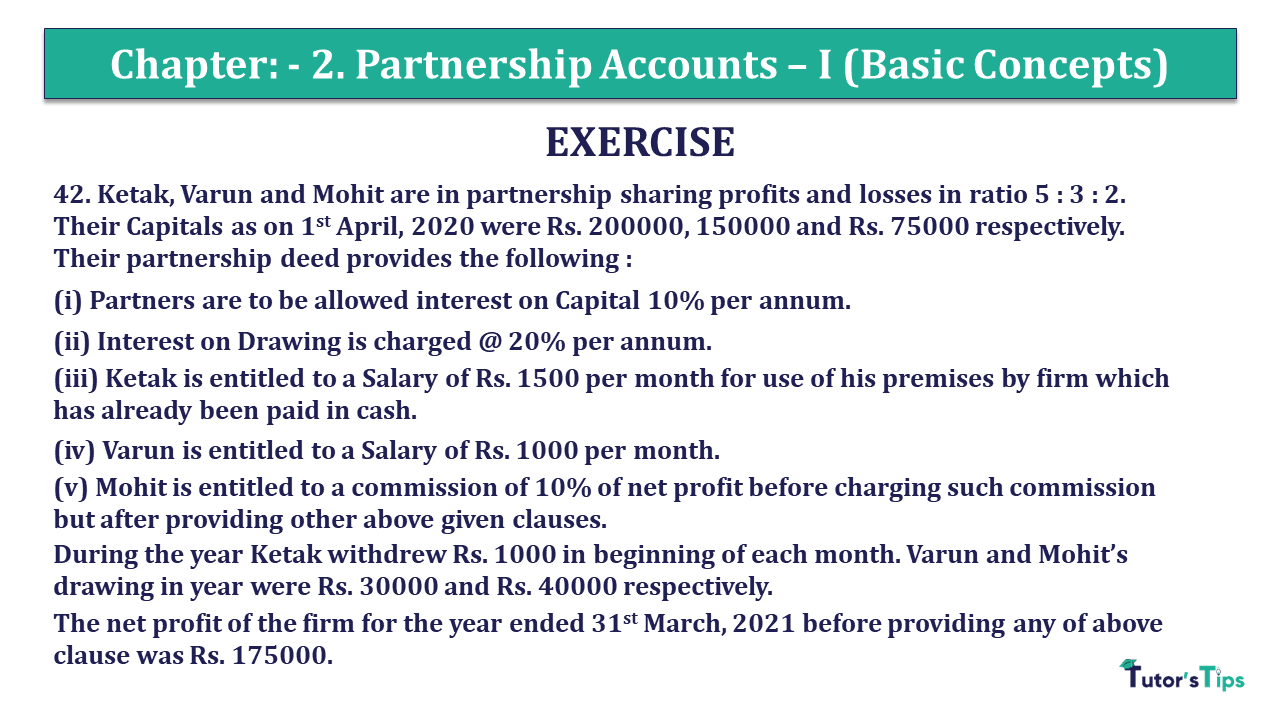

42. Ketak, Varun and Mohit are in partnership sharing profits and losses in ratio 5 : 3 : 2. Their Capitals as on 1st April, 2020 were Rs. 200000, 150000 and Rs. 75000 respectively. Their partnership deed provides the following :

(i) Partners are to be allowed interest on Capital 10% per annum.

(ii) Interest on Drawing is charged @ 20% per annum.

(iii) Ketak is entitled to a Salary of Rs. 1500 per month for use of his premises by firm which has already been paid in cash.

(iv) Varun is entitled to a Salary of Rs. 1000 per month.

(v) Mohit is entitled to a commission of 10% of net profit before charging such commission but after providing other above given clauses.

During the year Ketak withdrew Rs. 1000 in beginning of each month. Varun and Mohit’s drawing in year were Rs. 30000 and Rs. 40000 respectively.

The net profit of the firm for the year ended 31st March, 2021 before providing any of above clause was Rs. 175000.

The solution of Question 42 Chapter 2 – Unimax Class 12 Part 1:

Profit & Loss of Appropriation A/c of firm For the year ended 31st March., 2021

| Particulars | Rs. | Particulars | Rs. | ||

| To Interest on Capital | By Net Profit b/d | 175000 | |||

| – Ketak | 20000 | By Interest on Drawings A/c | |||

| – Varun | 15000 | Ketak | 1300 | ||

| – Mohit | 7500 | 42500 | Varun | 3000 | |

| To Rent (Ketak) (Rs. 1500 x 12) | 18000 | Mohit | 4000 | 8300 | |

| To Salary (Varun) (Rs. 1000 x 12) | 12000 | ||||

| To Commission (Mohit) (110800 x 10/100) | 11080 | ||||

| To Profit transferred | |||||

| Ketak | 49860 | ||||

| Varun | 29916 | ||||

| Mohit | 19944 | 99720 | |||

| 183300 | 183300 |

Partner’s Capital Accounts

| Particulars | Ketak | Varun | Mohit | Particulars | Ketak | Varun | Mohit |

| To Drawings | 12000 | 30000 | 40000 | 200000 | 150000 | 75000 | |

| To Interest on Drawings | 1300 | 3000 | 4000 | By Interest on Capital | 20000 | 15000 | 7500 |

| To Balance c/d | 256560 | 173916 | 69524 | By Salaries A/c | 12000 | ||

| By Commission A/c | 11080 | ||||||

| By Profit & Loss Appropriaton A/c | 49860 | 29916 | 19944 | ||||

| 269860 | 2069150 | 113524 | 269860 | 2069150 | 113524 | ||

| By Balance b/d | 269860 | 2069150 | 113524 |

Working Notes :

(1) Interest on Capitals @ 10% p.a.

Ketak : Rs. 200000 x 10/100 = Rs. 20000

Varun : Rs. 150000 x 10/100 = Rs. 15000

Mohit : Rs. 75000 x 10/100 = Rs. 7500

(2) Interest on Partner’s Drawings

Ketak : Rs. 12000 x 20/100 x 6.5/12 = Rs. 1300

Varun : Rs. 30000 x 20/100 x 6/12 = Rs. 3000

Mohit : Rs. 40000 x 20/100 x 6/12 = Rs. 4000

https://tutorstips.com/not-for-profit-organisations/

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication