Question 39 Chapter 1 – Unimax Class 12 Part 1

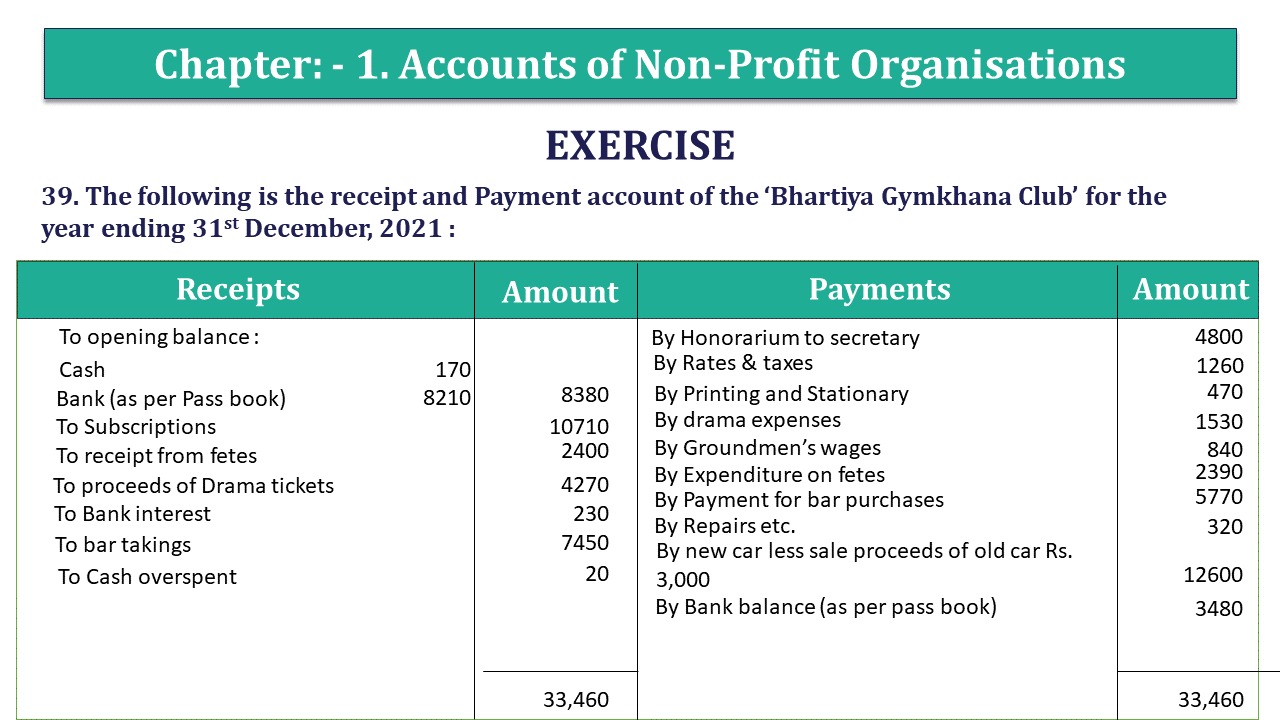

39. The following is the receipt and Payment account of the ‘Bhartiya Gymkhana Club’ for the year ending 31st December, 2021 :

| Receipts | Amount | Payments | Amount | ||

| To opening balance : | By Honorarium to secretary | 4800 | |||

| Cash | 170 | By Rates & taxes | 1260 | ||

| Bank (as per Pass book) | 8210 | 8380 | By Printing and Stationary | 470 | |

| To Subscriptions | 10710 | By drama expenses | 1530 | ||

| To receipt from fetes | 2400 | By Groundmen’s wages | 840 | ||

| To proceeds of Drama tickets | 4270 | By Expenditure on fetes | 2390 | ||

| To Bank interest | 230 | By Payment for bar purchases | 5770 | ||

| To bar takings | 7450 | By Repairs etc. | 320 | ||

| To Cash overspent | 20 | By new car less sale proceeds of old car Rs. 3,000 | 12600 | ||

| By Bank balance (as per pass book) | 3480 | ||||

| 33,460 | 33,460 |

You are given the following additional information :

| Particulars | 31.12.2020 | 31.12.2021 |

| (1) Subscription due | 1200 | 980 |

| (2) Unpresented Cheques being payment of printing | 90 | 30 |

| (3) Club premises at cost | 29000 | – |

| (4) Depreciation on club premises | 18800 | – |

| (5) Car at cost | 12190 | – |

| (6) Depreciation on car | 10290 | – |

| (7) Value of bar stock | 710 | 870 |

| (8) Amount due for bar purchases | 590 | 430 |

(9) Cash overspent represents amount of honorarium to the secretary not drawn due to shortage of funds. But the total salary payable to him for the year was already included in Rs. 4,800.

(10) Depreciation is to be provided @ 5% p.a. on the written down value of club premises and @ 15% p.a. on car for whole of the year.

You are required to adjust bank balance according to cash book and prepare income and expenditure account of the club and balance sheet as on 31st Dec., 2021.

The solution of Question 39 Chapter 1 – Unimax Class 12 Part 1:

Income and Expenditure account of Bhartiya Gymkhana Club

For the year ending 31st Dec, 2012

| Expenditure | Amount | Income | Amount | |

| To Honorarium | 4800 | By Subscription | 10490 | |

| To Rates & Taxes | 1260 | By Receipts from fetes | 2400 | |

| To Printing & Stationery | 410 | By proceeds of drama | 4270 | |

| To Drama Expenses | 1530 | By Bank interest | 230 | |

| To Ground man wages | 840 | By Bar takings | 7450 | |

| To expenses on fates | 2390 | By profit on the sale of old car | 1100 | |

| To Repairs | 320 | |||

| To Bar Expneses (2) | 5450 | |||

| To Depreciation : | ||||

| On club house | 510 | |||

| On Car | 2340 | 2850 | ||

| To surplus (excess of income over expenditure) | 6090 | |||

| 25940 | 25940 |

Balance Sheet of Bhartiya Gymkhana As on 31st Dec, 2012

| Liabilities | Amount | Assets | Amount | ||

| Outstanding Honorarium | 20 | O/s Subscription | 980 | ||

| Outstanding Expenses for Bar purchases | 430 | Bar Stock | 870 | ||

| Capital Fund | 21710 | Car | 13260 | ||

| Add Surplus | 6090 | 27800 | Club House premises | 9690 | |

| Bank | 3480 | ||||

| Less Unpresented cheque for stationery on 31-12-12 | 30 | 3450 | |||

| 28250 | 28250 |

https://tutorstips.com/not-for-profit-organisations/

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication