Question 29 Chapter 5 of +2-B

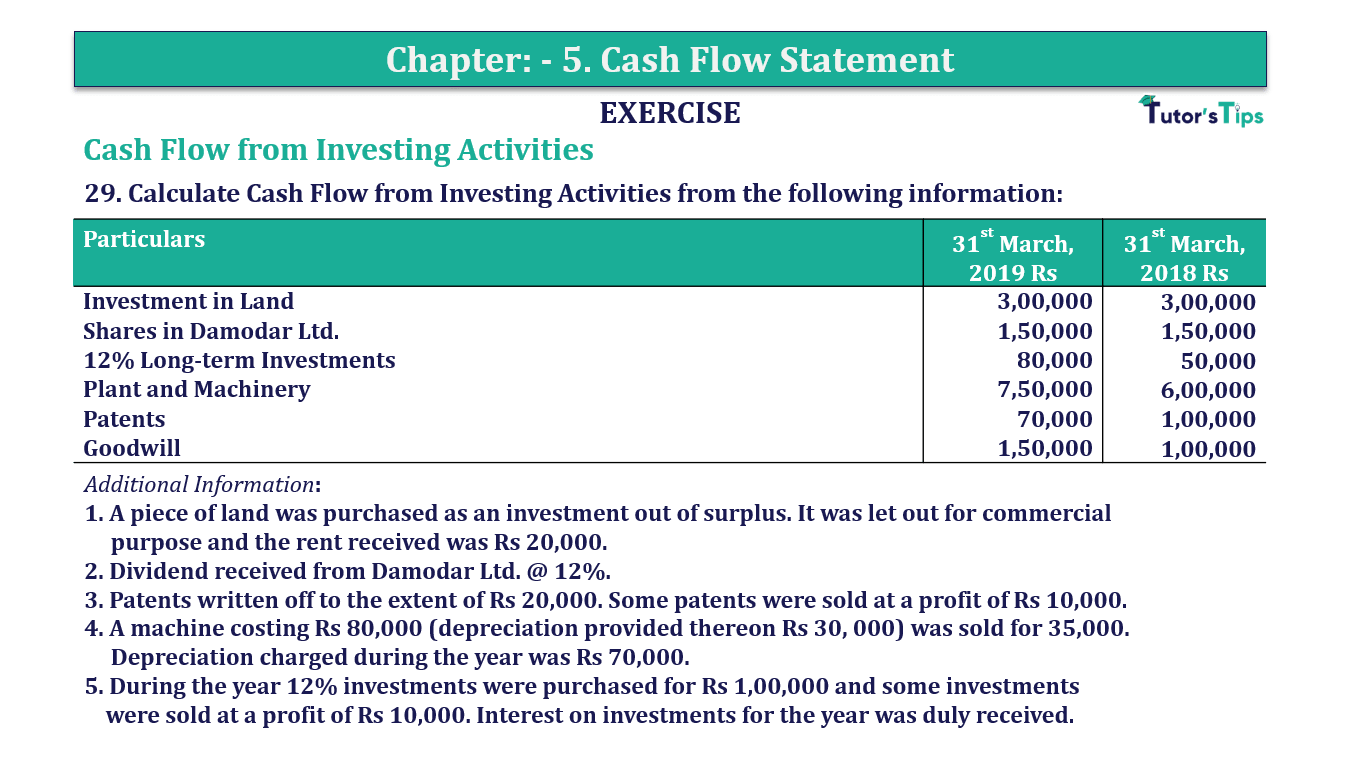

29. Calculate Cash Flow from Investing Activities from the following information:

| Particulars | 31st March, | 31st March, |

| 2019 Rs | 2018 Rs | |

| Investment in Land | 3,00,000 | 3,00,000 |

| Shares in Damodar Ltd. | 1,50,000 | 1,50,000 |

| 12% Long-term Investments | 80,000 | 50,000 |

| Plant and Machinery | 7,50,000 | 6,00,000 |

| Patents | 70,000 | 1,00,000 |

| Goodwill | 1,50,000 | 1,00,000 |

Additional Information:

1. A piece of land was purchased as an investment out of surplus. It was let out for commercial

purpose and the rent received was Rs 20,000.

2. Dividend received from Damodar Ltd. @ 12%.

3. Patents written off to the extent of Rs 20,000. Some patents were sold at a profit of Rs 10,000.

4. A machine costing Rs 80,000 (depreciation provided thereon Rs 30, 000) was sold for 35,000.

Depreciation charged during the year was Rs 70,000.

5. During the year 12% investments were purchased for Rs 1,00,000 and some investments

were sold at a profit of Rs 10,000. Interest on investments for the year was duly received.

The solution of Question 29 Chapter 4 of +2-B: –

Cash Flow From for the year ended 31st March, 2019 |

||

| Particulars |

Rs |

|

| I. Cash Flow from Investing Activities | ||

| Rent Received | 20,000 | |

| Dividend Received | 18,000 | |

| Sale of Plant and Machinery (WN 1) | 35,000 | |

| Sale of Investment (WN 2) | 80,000 | |

| Interest on Investments* | 6,000 | |

| Sale of Patents (WN 3) | 20,000 | |

| Less: Purchase of Plant and Machinery | 2,70,000 | |

| Less: Purchase of Investment | 1,00,000 | |

| Less: Purchase of Goodwill | 50,000 | 2,41,000 |

| Net Cash Used in Investing Activities | 2,41,000 | |

*Interest on Investment:-

| Interest on Investment | = | 12% |

| = | Rs 2,00,000 X 12% | |

| = | Rs 6,000 |

| Plant and Machinery Account |

|||

| Particulars |

Rs | Particular | Rs |

| To Balance b/d | 6,00,000 | By Depreciation A/c | 70,000 |

| To Bank A/c (Purchase) (Bal. Fig.) | 2,70,000 | By Bank A/c (Sale) | 35,000 |

| By Loss on Sale (Profit and Loss A/c) | 15,000 | ||

| By Balance c/d | 7,50,000 | ||

| 8,70,000 | 8,70,000 | ||

| Investments Account |

|||

| Particulars |

Rs | Particular | Rs |

| To Balance b/d | 50,000 | By Bank A/c (Sale) | 80,000 |

| To Bank A/c (Purchase) (Bal. Fig.) | 1,00,000 | By Balance c/d | 80,000 |

| To Profit on sale (Profit and Loss A/c) | 10,000 | ||

| 1,60,000 | 1,60,000 | ||

| Investments Account |

|||

| Particulars |

Rs | Particular | Rs |

| To Balance b/d | 1,00,000 | By Profit & loss A/c (Written-off) | 20,000 |

| To Profit on sale (Profit and Loss A/c) | 10,000 | By Bank A/c (Sale) (Bal. fig.) | 20,000 |

| By Balance c/d | 70,000 | ||

| 1,10,000 | 1,10,000 | ||

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: –

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication