We can divide all the businesses or organisations into two major categories namely, profit(commercial) organisations and not-for-profit organisations. The earning profit is the basic difference between these two categories of business. The primary objective of profit organisations is to do work to earn profit but on the other hand, the primary objective of not-for-profit organisations is to do work for the welfare of society.

Subscribe to our Youtube Channel

Meaning of Not-for-Profit Organisations: –

Not-for-profit organisations are those organisations which did not do their work to earn profit rather than their main objective is to do work to achieve a specific goal for the welfare of society or its members. These are also known as non-profit organisations.

The type of organisation runs its operation mainly on donations, entrance fees, subscription fees or membership fees.

Examples: –

- Charitable Hospital

- Charitable Schools, Colleges or Educational Institutions

- Particulars Club of any Society, Colony or city

- Gurudwaras, Temple, Church and Masjids

Basic Terminology of Not-for-Profit Organizations: –

There are basic terms which you have to know before starting this chapter these are shown as follows: –

- Subscription

- Membership Fees

- Donations

- Government Grants

- Entrance Fees

- Honorarium

- Legacy

- Capital Fund

- Endowment Fund

- Sale of Scrap

- Sale of assets

1. Subscription: –

Subscription in NPO means paying some amount to an organisation by its member on a regular basis. It can be collected by the Organisation on a monthly, quarterly or yearly basis. This is the revenue for the organisation so, it will be credited to the Income and expenditure account.

2. Membership Fees: –

Membership fees mean to pay something to an organisation by its member to join the organisation. This is also the revenue for the organisation so, it will be credited to the Income and expenditure account.

3. Donations: –

Donation means when someone pays some amount to the organisation without any consideration. The main source of revenue for the Not-for-Profit organisation is donations. If a Donation is received for specific work then it will be treated as capital receipt and transferred to fund accounts(Balance Sheet) other than that, it will be treated as our revenue so, it will be credited to the Income and expenditure account.

4. Government Grants: –

Government Grants mean when the government pays some amount to the organisation for specific work or on a recurring basis. If Grants are received for specific work then it will be treated as capital receipts and transferred to fund accounts(Balance Sheet). If received on a recurring basis to run the organisation’s operations then it will be treated as our revenue for the organisation so, it will be credited to the Income and expenditure account.

5. Entrance Fees: –

Entrance fees mean to pay something to an organisation by its member to join the organisation. This is a one-time payment so it will be capitalized. So, it will be treated as capital receipts and transferred to the funds (Balance sheet). If in any business it is a recurring payment then it will be treated as revenue receipts and will be credited in the income and expenditure account. (This will be given in the question.)

6. Honorarium: –

Honorarium means the amount which is paid to non-employees for services received by them. It will be treated as revenue payment so will be debited to the Income and Expenditure account.

7. Legacy: –

Any amount received by the organisation as per the Will of a deceased person is called a Legacy. This item is non-recurring in nature so it will be treated as a capital receipt and recorded on the liabilities side of the Balance sheet.

8. Capital Fund: –

The captial fund is similar to the Capital Account like profit organisations. The excess of assets over liabilities is called a capital fund. This will be recorded on the liabilities side of the Balance sheet.

9. Endowment Fund: –

When any assets are received by the organisation as a gift then on the liabilities side we have created a fund named Endowment Fund to show the restriction.

10. Sale of Scrap:-

The sale of old newspapers, Magazines etc., is treated as revenue items and will be recorded on the credit side of the income and expenditure account.

11. Sale of assets: –

The amount received from the sale of assets is treated as capital receipts so will not be recorded in the Income and expenditure account. But profit or loss incurred will be transferred to the Income and expenditure account.

Financial Statements under Not-for-Profit Organisations: –

In the Not-for-Profit Organisation, we have prepared the following financial statements: –

- Receipts and Payment A/c

- Income and Expenditure A/c

- Balance Sheet

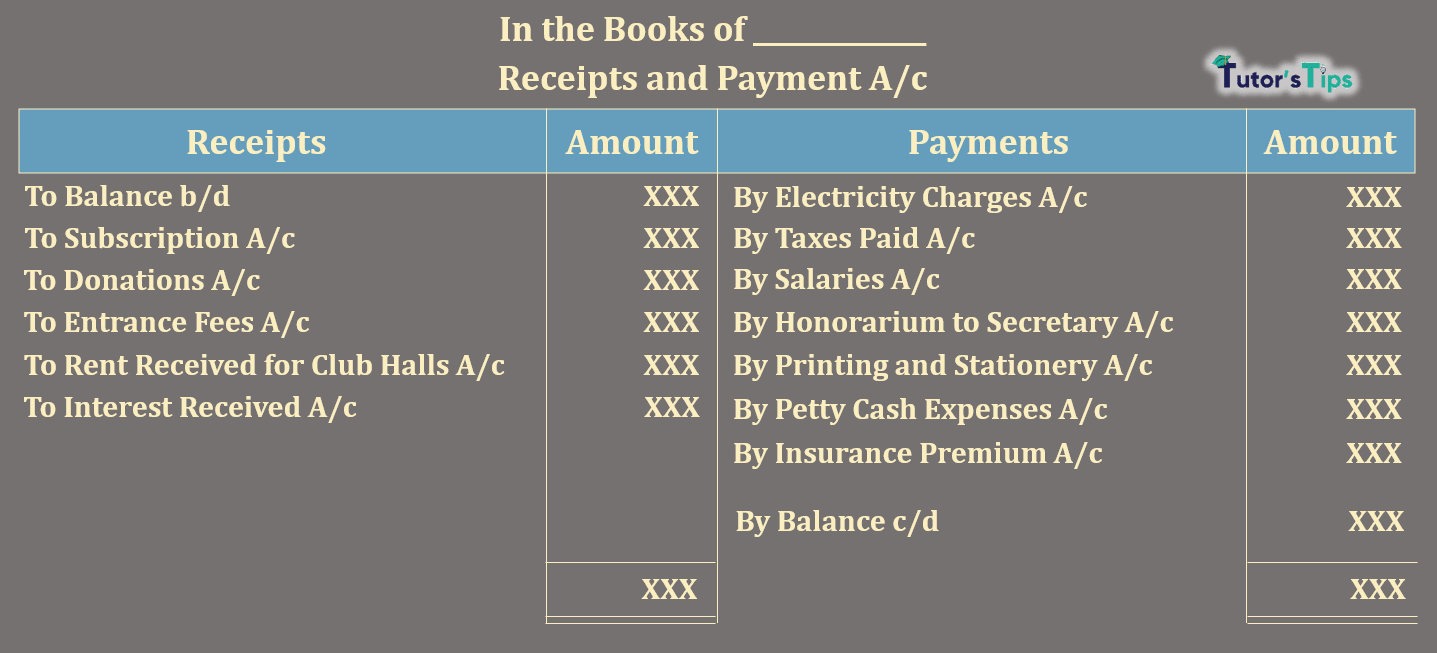

1. Receipts and Payments A/c

The Receipts and Payment account is similar to the cash account prepared in the profit organisations. All the transactions related to the cash receipts and cash payments are recorded in these accounts in Not-for-Profit organisations. The following is the format of the receipt and payment account.

2. Incomes and Expenditures A/c

The Income and Expenditure account is similar to the Trading and Profit/Loss account prepared in the profit organisations. All the transactions of the revenue receipts and payments related to the current year are recorded in these accounts in Not-for-Profit organisations.

The excess over the income from expenditure is known as Surplus instead of Profit and excess over the expenditure from the income is known as a deficit instead of a loss. The following is the format of the Income and Expenditure account.

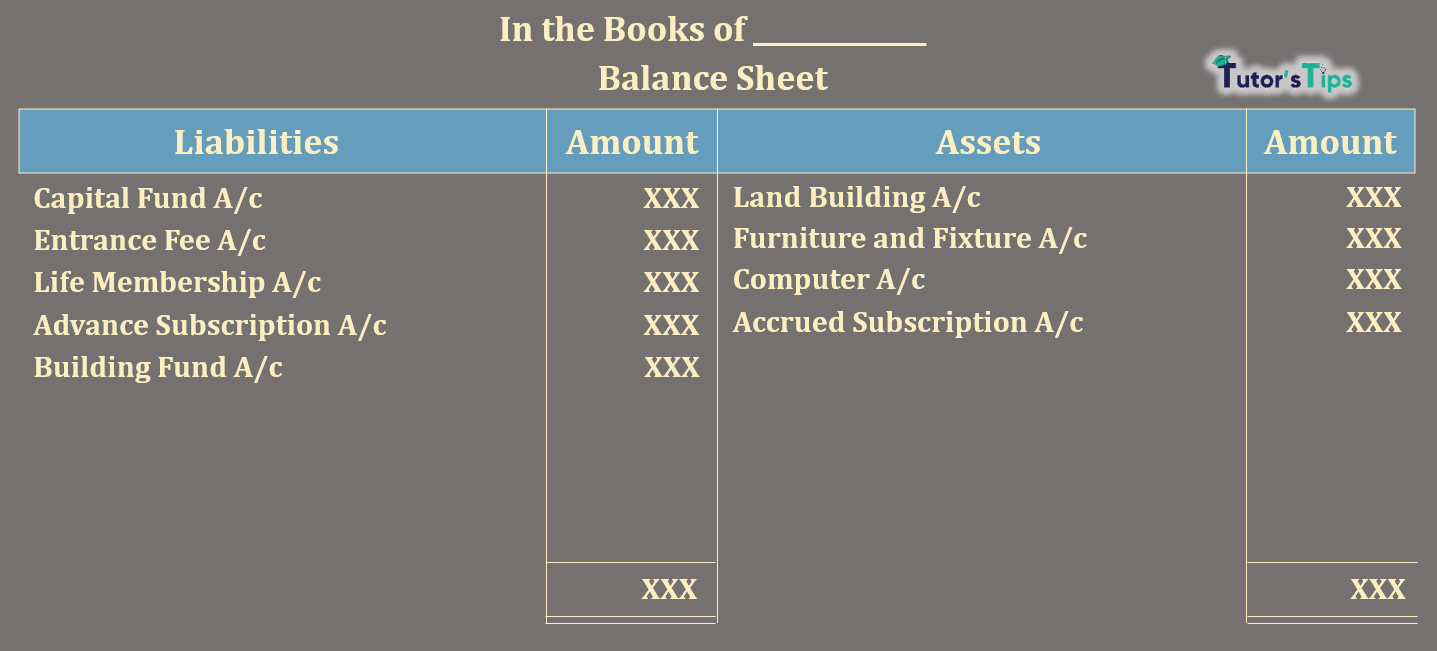

3. Balance Sheet

The balance sheet is similar to the balance sheet prepared in the profit organisations. There is just one difference between the balance sheet of Not-For-Profit organisations and Profit organisations. In Not-For-Profit organisations, there will be a capital Fund rather than a capital account. The following is the format of the Balance Sheet.

Thanks for reading the topic

please comment your feedback in the comment box whatever you want. If you have any questions please ask us by commenting on us

Check out T.S. Grewal’s +2 Book 2020 @ Official Website of Sultan Chand Publication