Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Question No 42 Chapter No 18

Goods withdrawn for business and personal use

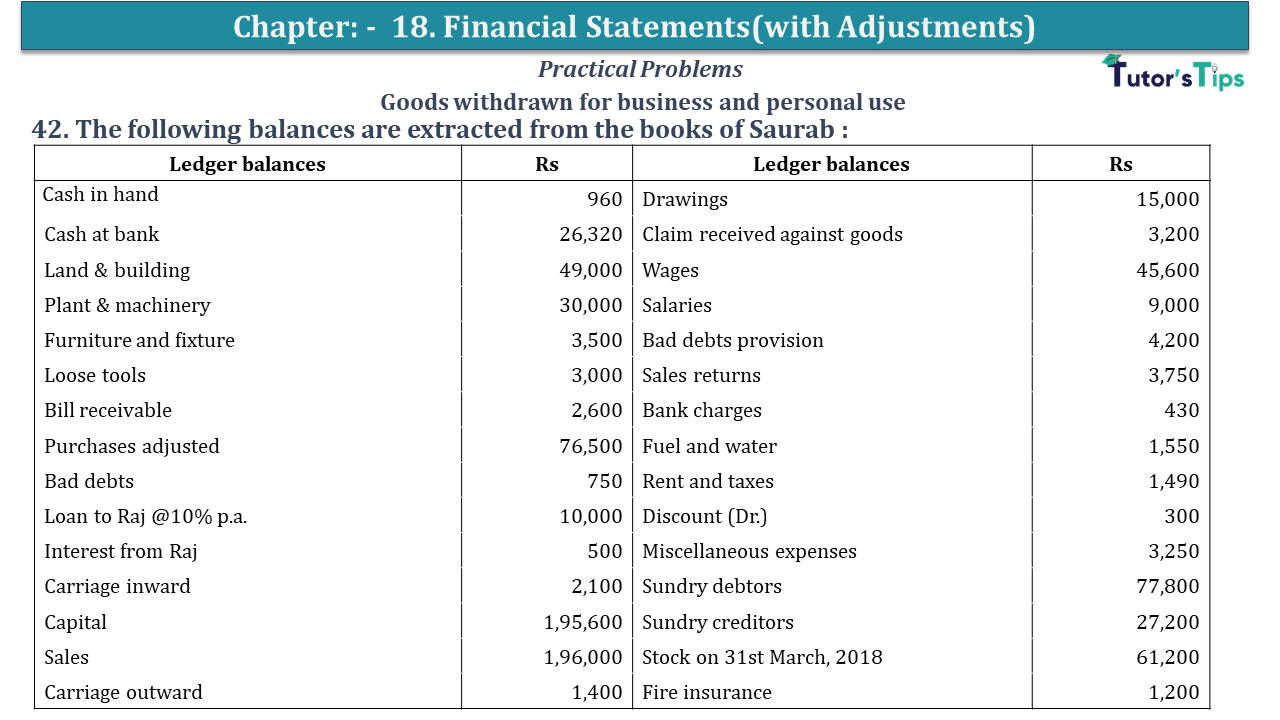

42. The following balances are extracted from the books of Saurab :

| Ledger balances | Rs | Ledger balances | Rs |

| Cash in hand | 960 | Drawings | 15,000 |

| Cash at bank | 26,320 | Claim received against goods | 3,200 |

| Land & building | 49,000 | Wages | 45,600 |

| Plant & machinery | 30,000 | Salaries | 9,000 |

| Furniture and fixture | 3,500 | Bad debts provision | 4,200 |

| Loose tools | 3,000 | Sales returns | 3,750 |

| Bill receivable | 2,600 | Bank charges | 430 |

| Purchases adjusted | 76,500 | Fuel and water | 1,550 |

| Bad debts | 750 | Rent and taxes | 1,490 |

| Loan to Raj @10% p.a. | 10,000 | Discount (Dr.) | 300 |

| Interest from Raj | 500 | Miscellaneous expenses | 3,250 |

| Carriage inward | 2,100 | Sundry debtors | 77,800 |

| Capital | 1,95,600 | Sundry creditors | 27,200 |

| Sales | 1,96,000 | Stock on 31st March, 2018 | 61,200 |

| Carriage outward | 1,400 | Fire insurance | 1,200 |

Adjustments:

Prepare the balance sheet and trading and profit and loss account as on and for the year ended 31st March 2018, after giving effect to the following adjustments

(a) Depreciation to be charged on land and building @ 2.5%, on plant and machinery at 10% and furniture and fixture at 10%.

(b) Provision for doubtful debts to be made at 5% and for a discount at 2%.

(c) The unexpired amounts to be carried forward are fire insurance 200 and rates and taxes 500. (d) Loose tools were valued at 1,200 on 31st March 2018.

(e) Of the sundry debtors 800 are bad and should be written/off.

(f) Trade expenses 300 have not yet been paid and wages include 500 spent on installation of machinery purchased

Trading A/c

| Particular |

Amount | Particular |

Amount | ||

|---|---|---|---|---|---|

| To Purchases A/c | 76,500 | By Sale A/c | 1,96,000 | ||

| To wages A/c | 45,600 | Less: return | 3,750 | 1,92,250 | |

| Less: wages paid for installation | 500 | 45,100 | |||

| To fuel & power A/c | 1,550 | By Closing Stock A/c | 3,200 | ||

| To carriage inwards A/c | 2,100 | ||||

| To Gross Profit A/c | 70,200 | ||||

| 1,95,450 | 1,95,450 | ||||

Profit/Loss A/c

| Particular |

Amount | Particular |

Amount | ||

|---|---|---|---|---|---|

| To Carriage outwards | 1,400 | By Gross Profit A/c | 70,200 | ||

| To fire insurance | 1,200 | By Rent A/c | 500 | ||

| Less: prepaid | 200 | 1,000 | Add: Interest accrued | 500 | 1,000 |

| To Rates & taxes | 1,490 | ||||

| Less: Paid in advice | 500 | 990 | |||

| To provision for doubtful debts | |||||

| Add: bad debts | 750 | ||||

| Add: further bad debts | 800 | ||||

| Add: new provision | 3,850 | ||||

| Less: old provision | 4,200 | 1,200 | |||

| To discount | 300 | ||||

| To provision for discount on debtors | 1,463 | ||||

| To Salaries | 9,000 | ||||

| To bank charges | 430 | ||||

| To miscellaneous Exp. | 3,250 | ||||

| To trade exp. | 300 | ||||

| To Dep. On land & building | 1,225 | ||||

| To Dep. On plant & machinery | 3,050 | ||||

| To Dep. Furniture & fixture | 350 | ||||

| To Dep. Loose tools | 1,800 | ||||

| To Net profit A/c | 45,442 | ||||

| 71,200 | 71,200 | ||||

Balance Sheet

| Labilities |

Amount | Assets |

Amount | ||

|---|---|---|---|---|---|

| Capital A/c | 1,95,600 | Debtors | 77,800 | ||

| Add: Net Profit | 45,442 | Less: bad debts | 800 | ||

| Less: Drawing | 15,000 | 2,26,042 | Less: provision | 3,850 | |

| Creditor | 27,200 | Less: provision for discount | 1,463 | 71,687 | |

| Outstanding trade exp. | 300 | Cash at bank | 960 | ||

| Cash at bank | 26,320 | ||||

| Furniture & fitting | 3,500 | ||||

| Less: depreciation | 350 | 3,150 | |||

| Loose tools | 3,000 | ||||

| Less: depreciation | 1,800 | 1,200 | |||

| Closing Stock | 61,200 | ||||

| Bills receivable | 2,600 | ||||

| Loan to Raj | 10,000 | ||||

| Interest outstanding | 500 | ||||

| Fire insurance prepaid | 200 | ||||

| Rates & taxes prepaid | 500 | ||||

| Plant & machinery | 30,000 | ||||

| Add: wages for installation | 500 | ||||

| Less: depreciation | 3,050 | 27,450 | |||

| Land & building | 49,000 | ||||

| Less: depreciation | 1,225 | 47,775 | |||

| 2,53,542 | 2,53,542 | ||||

https://tutorstips.com/final-accounts/

https://tutorstips.com/profit-and-loss-account/

https://tutorstips.com/balance-sheet/

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Chapter No. 2 - Theory Base of Accounting

Chapter No. 3 - Origin of Transactions

Chapter No. 4 - Vouchers and transactions

Chapter No. 6 - Accounting for Goods and Services Tax(GST)

Chapter No. 9 - Other Subsidiary Books

Chapter No. 10 - Journal Proper

Chapter No. 11 - Trial Balance

Chapter No. 12 - Bank Reconciliation Statement

Chapter No. 14 - Provisions and Reserves

Chapter No. 15 - Bills of Exchange

Chapter No. 16 - Rectification of Errors

Chapter No. 17 - Financial Statements - (Without Adjustments)

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 42 Chapter No 18 - USHA Publication 11 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to USHA Publication +1 Elements of Book-Keeping.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 42 Chapter No 18 - USHA Publication 11 Class" instantly.