Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

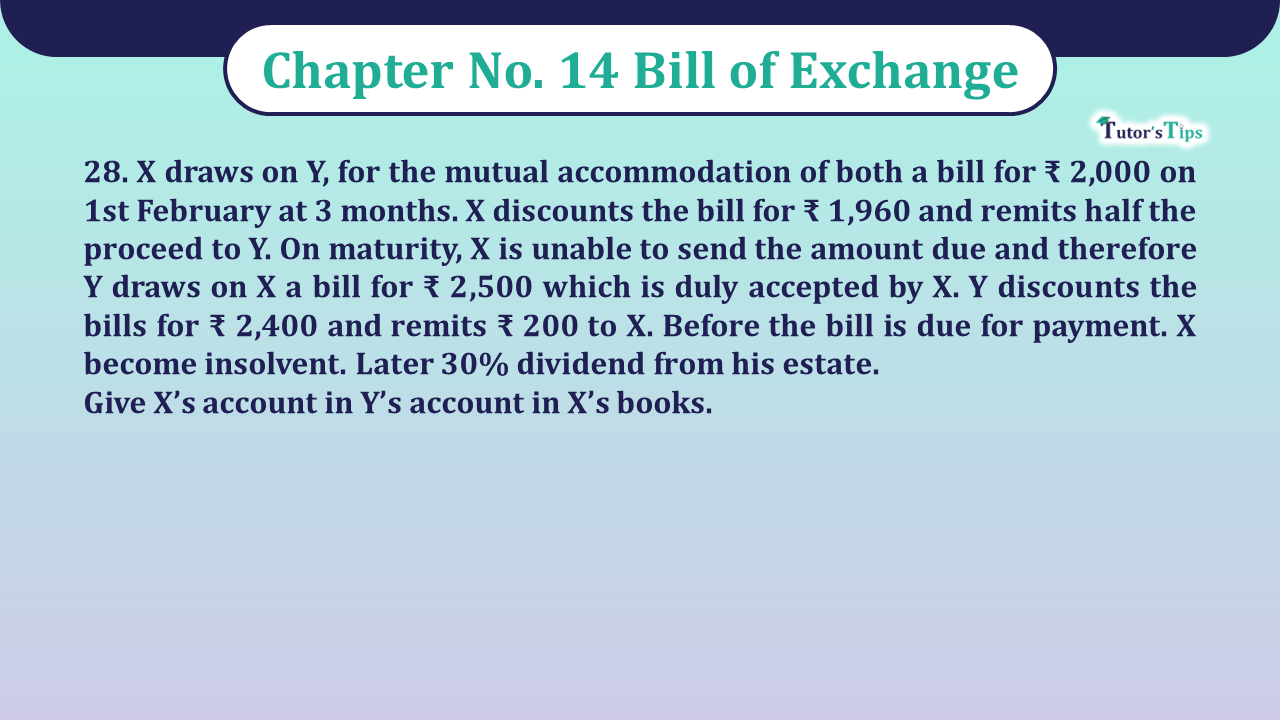

28. X draws on Y, for the mutual accommodation of both a bill for ₹ 2,000 on 1st February at 3 months. X discounts the bill for ₹ 1,960 and remits half the proceed to Y. On maturity, X is unable to send the amount due and therefore Y draws on X a bill for ₹ 2,500 which is duly accepted by X. Y discounts the bills for ₹ 2,400 and remits ₹ 200 to X. Before the bill is due for payment. X become insolvent. Later 30% dividend from his estate.

Give X’s account in Y’s account in X’s books.

Journal for Mr. ‘X’ (Drawer)

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Feb. 1 | Bill receivable A/c | Dr. | 2,000 | ||

| To Y’s A/c | 2,000 | ||||

| (Being acceptance of bill received from Y for mutual accommodation) | |||||

| Feb. 1 | Bank A/c | Dr. | 1,960 | ||

| Discount A/c | Dr. | 40 | |||

| To Bills receivable A/c | 2,000 | ||||

| (Being bill discounted with bank) | |||||

| Feb.1 | Y’s A/c | Dr. | 1,000 | ||

| To Cash A/c | 980 | ||||

| To Discount A/c | 20 | ||||

| (Being half the amount remitted) | |||||

| May 4 | Y’s A/c | Dr. | 2,500 | ||

| To Bills payable A/c | 2,500 | ||||

| (Being acceptance of bill given to Y) | |||||

| May 4 | Cash A/c | Dr. | 200 | ||

| Discount A/c | Dr. | 50 | |||

| To Y’s A/c | 250 | ||||

| (Being cash received from Y and discount allowed) | |||||

| Due date | Bill payable A/c | Dr. | 2,500 | ||

| To Y’s A/c | 2,500 | ||||

| (Being insolvent & bill not met) | |||||

| Before Due date | Y’s A/c (1,000+250) | Dr. | 1,250 | ||

| To cash A/c | 375 | ||||

| To Deficiency A/c | 875 | ||||

| (Being insolvent & only 30% paid to Y) | |||||

| Dr. | Y's A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Feb. 1 | To cash A/c | 980 | Feb. 1 | By Bill receivable A/c | 2,000 | ||

| Feb. 1 | To Discount A/c | 20 | Mar. 4 | By Discount A/c | 50 | ||

| May 4 | To Bill payable A/c | 2,500 | May 4 | By Cash A/c | 200 | ||

| To Cash A/c | 375 | By Bill Payable A/c | 2,500 | ||||

| To Deficiency A/c | 875 | ||||||

| 4,750 | 4,750 | ||||||

Journal for Mr. ‘Y’ (Drawee)

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Feb. 1 | X’s A/c | Dr. | 2,000 | ||

| To Bill payable A/c | 2,000 | ||||

| (Being acceptance of bill given to X for 3 months) | |||||

| Feb. 1 | Cash A/c | Dr. | 980 | ||

| Discount A/c | Dr. | 20 | |||

| To X’s A/c | 1,000 | ||||

| (Being half the amount of bill received from X) | |||||

| May 4 | Bills payable A/c | Dr. | 2,000 | ||

| To Cash A/c | 2,000 | ||||

| (Being bill met on due date) | |||||

| May 4 | Bills receivable A/c | Dr. | 2,500 | ||

| To X’s A/c | 2,500 | ||||

| (Being acceptance of bill received from X) | |||||

| May 4 | Bank A/c | Dr. | 2,400 | ||

| Discount A/c | Dr. | 100 | |||

| To Bills receivable A/c | 2,500 | ||||

| (Being bill discounted with bank) | |||||

| May 4 | X’s A/c | Dr. | 250 | ||

| To Cash A/c | 200 | ||||

| To Discount A/c | 50 | ||||

| (Being cash paid to X) | |||||

| Before Due date | X’s A/c | Dr. | 2,500 | ||

| To Bank A/c | 250 | ||||

| (Being bill not met on due date by X) | |||||

| Before Due date | Cash A/c | Dr. | 375 | ||

| Bad debts A/c | Dr. | 875 | |||

| To X’s (1,000+250) A/c | 1,250 | ||||

| (Being ‘X’ become insolvent and only 30% amount received from him) | |||||

| Dr. | X's A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Feb. 1 | To Bills payable A/c | 2,000 | Feb. 1 | By Bill receivable A/c | 23,000 | ||

| Mar. 4 | To Discount A/c | 50 | Feb. 1 | By Bill receivable A/c | 23,485 | ||

| May 4 | To cash A/c | 200 | Mar. 4 | By Cash A/c | 10,000 | ||

| To Bank A/c | 2,500 | By Bill receivable A/c | 13,985 | ||||

| 4,750 | 4,750 | ||||||

Working Note:

(i) As soon as one party become insolvent after making dishonoured entry it should be found as to how much amount is due by ‘X’ to ‘Y’ for which we should prepare X’s account in Y’s books and Y’s A/c in X’s book. Both will show the same amount with different balance (Dr. or Cr.)

(ii) Discounting charges of second bill have been apportioned in the ratio in which X & Y shared the proceeds of second bill i.e. 1:1 shown as follows:

Total proceeds received of second bill

Amount paid on behalf of partners for 1st bill

| X | Y | |

| 1,000 | 1,000 | |

| Balance (₹ 2,400-2,000) 400, distributed as | 200 | 200 |

| 1,200 | 1,200 | |

| Ratio which proceeds of second bill shared 1:1 | ||

| Discounting charges of second bill to be shared | 50 | 50 |

Read out the full article to know the meaning of Cash Book

Bill of exchange (BOE): Meaning and Examples

Also, Check out the same article in Hindi from the following link

Bill of exchange (BOE): Meaning and Examples

Also, Check out the solved question of all Chapters: –

Part-I

Students may choose only one part from the Part II and Part III

Part-II

Part-III

Check out T.S. Grewal +1 Book 2019 @ Oficial Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 28 Chapter No 14 – Class 11 Unimax", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax class 11 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 28 Chapter No 14 – Class 11 Unimax" instantly.