Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

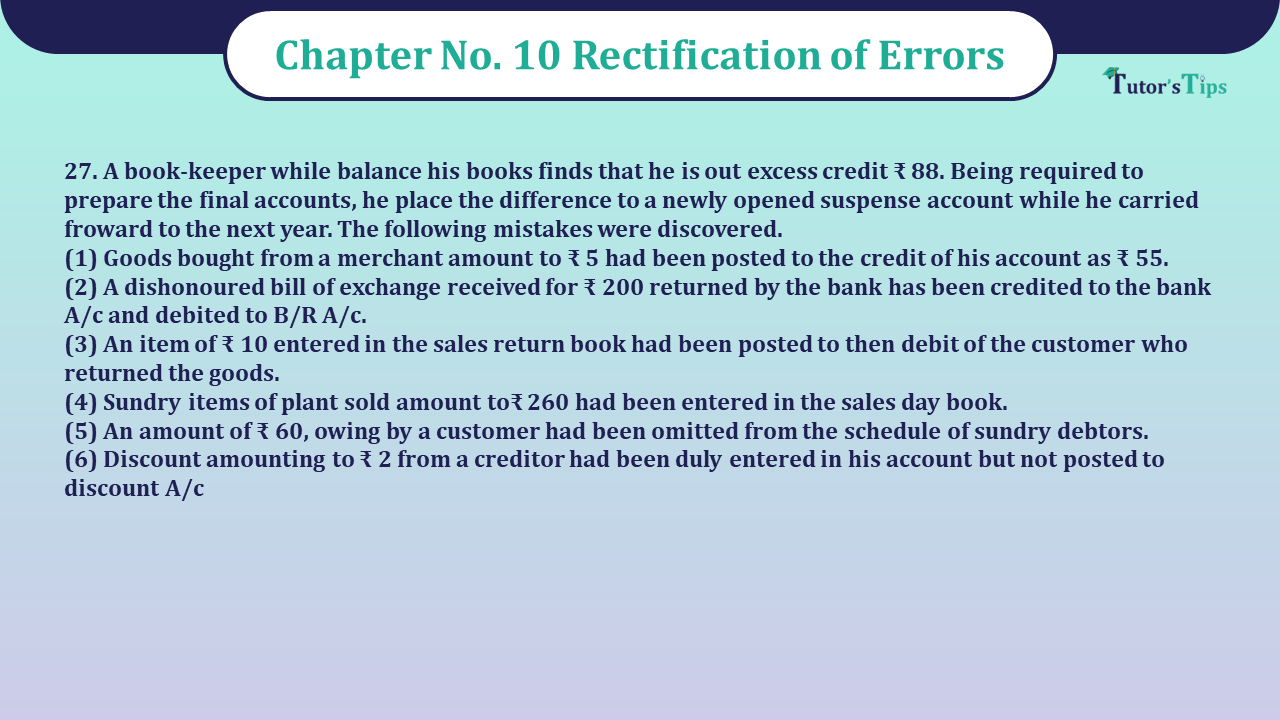

Question No 27 Chapter No 10 - Unimax Class 11

27 A book-keeper while balance his books finds that he is out excess credit ₹ 88. Being required to prepare the final accounts, he place the difference to a newly opened suspense account while he carried froward to the next year. The following mistakes were discovered.

(1) Goods bought from a merchant amount to ₹ 5 had been posted to the credit of his account as ₹ 55.

(2) A dishonoured bill of exchange received for ₹ 200 returned by the bank has been credited to the bank A/c and debited to B/R A/c.

(3) An item of ₹ 10 entered in the sales return book had been posted to then debit of the customer who returned the goods.

(4) Sundry items of plant sold amount to₹ 260 had been entered in the sales day book.

(5) An amount of ₹ 60, owing by a customer had been omitted from the schedule of sundry debtors.

(6) Discount amounting to ₹ 2 from a creditor had been duly entered in his account but not posted to discount A/c

Journal

| Date | Particulars | L.F. | Debit | Credit | ||

|---|---|---|---|---|---|---|

| 1 | Merchant’s A/c | Dr. | 50 | |||

| To Sales A/c | 2,500 | |||||

| (Being goods bought from Merchant of ₹ 05 posted to credit of his a/c as ₹ 55, now rectified) | ||||||

| 2 | Debtors A/c | Dr. | 200 | |||

| To Bills receivable A/c | 200 | |||||

| (Being bill receivable dishonoured & credited to Bank & debit of B/R now rectified) | ||||||

| 3 | Suspense A/c | Dr. | 20 | |||

| To Customer’s A/c | 20 | |||||

| (Being goods returned by customer entered in debit of his a/c, now rectified) | ||||||

| 4 | Sales A/c | Dr. | 260 | |||

| To Plant A/c | 260 | |||||

| (Being plant sold entered in sales book, now rectified) | ||||||

| 5 | Sundry debtors A/c | Dr. | 60 | |||

| To Suspense A/c | 60 | |||||

| (Being customer not entered in sundry debtors, now rectified) | ||||||

| 6 | Suspense A/c | Dr. | 2 | |||

| To discount A/c | 2 | |||||

| (Being discount from a credit entered in his account but not posted to discount a/c, now rectified) | ||||||

| Dr. | Suspense A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| To Balance b/d | 88 | By Machinery A/c | 50 | ||||

| To Customer A/c | 20 | By Sundry debtors A/c | 60 | ||||

| To Discount A/c | 02 | ||||||

| 110 | 110 | ||||||

It is all about Question 27 Chapter 10 of Class 11 unimax, If you have any problem please comment below.

Read out the full article to know the meaning of Rectification of Errors

Error Rectification in accounting – Explanation with examples

Also, Check out the same article in Hindi from the following link

Error Rectification in accounting – Explanation with examples-in Hindi

Also, Check out the solved question of all Chapters: –

Part-I

Students may choose only one part from the Part II and Part III

Part-II

Part-III

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 27 Chapter No 10 - Unimax 11 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax class 11 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 27 Chapter No 10 - Unimax 11 Class" instantly.