Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Question No 2 Chapter No 11

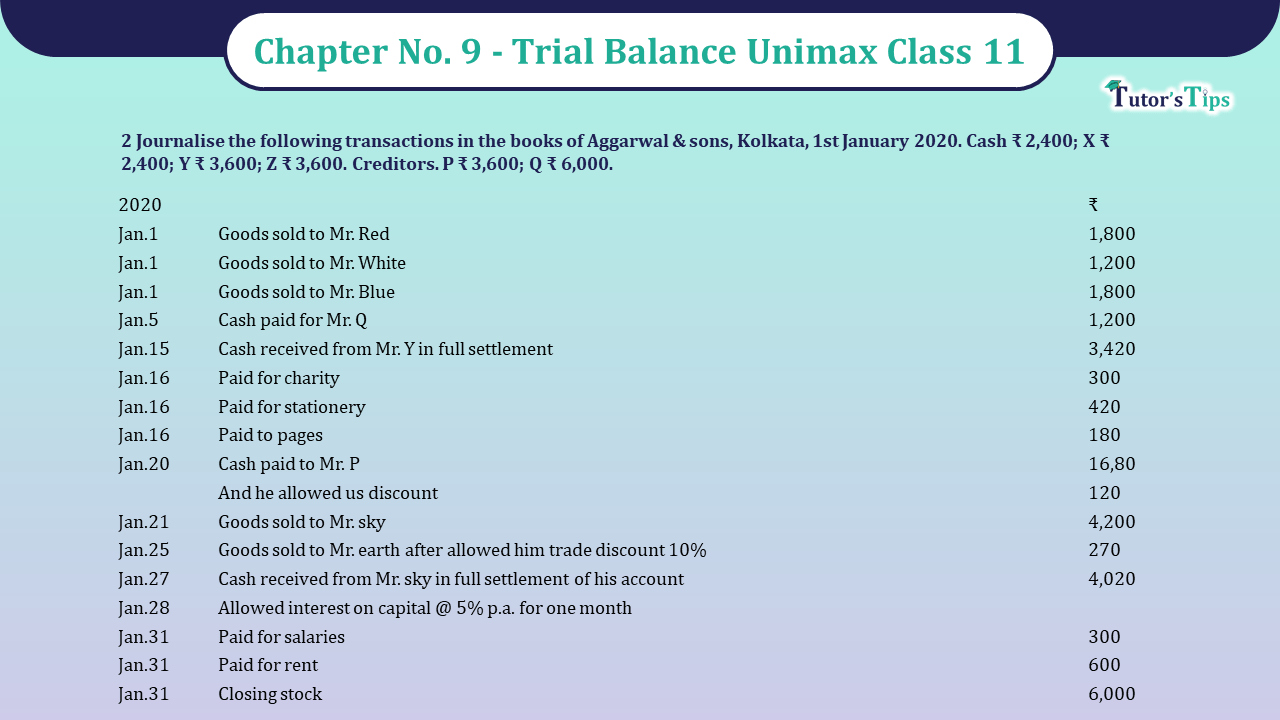

Journalise the following transactions in the books of Aggarwal & sons, Kolkata, 1st January 2020. Cash ₹ 2,400; X ₹ 2,400; Y ₹ 3,600; Z ₹ 3,600. Creditors. P ₹ 3,600; Q ₹ 6,000.

| 2020 | ₹ | |

| Jan.1 | Goods sold to Mr. Red | 1,800 |

| Jan.1 | Goods sold to Mr. White | 1,200 |

| Jan.1 | Goods sold to Mr. Blue | 1,800 |

| Jan.5 | Cash paid for Mr. Q | 1,200 |

| Jan.15 | Cash received from Mr. Y in full settlement | 3,420 |

| Jan.16 | Paid for charity | 300 |

| Jan.16 | Paid for stationery | 420 |

| Jan.16 | Paid to pages | 180 |

| Jan.20 | Cash paid to Mr. P | 16,80 |

| And he allowed us discount | 120 | |

| Jan.21 | Goods sold to Mr. sky | 4,200 |

| Jan.25 | Goods sold to Mr. earth after allowed him trade discount 10% | 270 |

| Jan.27 | Cash received from Mr. sky in full settlement of his account | 4,020 |

| Jan.28 | Allowed interest on capital @ 5% p.a. for one month | |

| Jan.31 | Paid for salaries | 300 |

| Jan.31 | Paid for rent | 600 |

| Jan.31 | Closing stock | 6,000 |

Journal

| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 2020 | |||||

| Jan.1 | Cash A/c | Dr. | 12,000 | ||

| Furniture A/c | Dr. | 2,400 | |||

| W’s A/c | Dr. | 2,400 | |||

| Building A/c | Dr. | 36,000 | |||

| X’s A/c | Dr. | 2,400 | |||

| Y’s A/c | Dr. | 3,600 | |||

| Z’s A/c | Dr. | 3,600 | |||

| To P’s A/c | 3,600 | ||||

| To Q’s A/c | 6,000 | ||||

| To Capital A/c | 52,800 | ||||

| (Being opening entry made) | |||||

| Jan.1 | Mr. Red’s A/c | Dr. | 1,800 | ||

| To Sales A/c | 1,800 | ||||

| (Being goods sold to Mr. Red) | |||||

| Jan.1 | Mr. White’s A/c | Dr. | 1,200 | ||

| To Sales A/c | 1,200 | ||||

| (Being goods sold to Mr. White) | |||||

| Jan.1 | Mr. Blue’s A/c | Dr. | 1,800 | ||

| To Sales A/c | 1,800 | ||||

| (Being goods sold to Mr. Blue) | |||||

| Jan.5 | Mr. Q’s A/c | Dr. | 1,200 | ||

| To Cash A/c | 1,200 | ||||

| (Being cash paid to Mr. Q) | |||||

| Jan.15 | Cash A/c | Dr. | 3,420 | ||

| Discount A/c | Dr. | 180 | |||

| To Mr. T’s A/c | 3,600 | ||||

| (Being cash received from Mr. Y and discount allowed) | |||||

| Jan.16 | Charity A/c | Dr. | 300 | ||

| To Cash A/c | 300 | ||||

| (Being paid for charity) | |||||

| Jan.16 | Stationery A/c | Dr. | 420 | ||

| Postage | Dr. | 180 | |||

| To Cash A/c | 600 | ||||

| (Being paid for stationery postages) | |||||

| Jan.20 | Mr. P’s A/c | Dr. | 1,800 | ||

| To Cash A/c | 1,680 | ||||

| To Discount A/c | 120 | ||||

| (Being cash paid to Mr. P and received) | |||||

| Jan.21 | Mr. sky’ A/c | Dr. | 4,200 | ||

| To Sales A/c | 4,200 | ||||

| (Being goods sold to Mr. sky) | |||||

| Jan.25 | Mr. Earth A/c | Dr. | 243 | ||

| To Sales A/c | 243 | ||||

| (Being goods sold to Mr. Earth) | |||||

| Jan.27 | Cash A/c | Dr. | 4,020 | ||

| Discount A/c | Dr. | 180 | |||

| To Mr. Sky’s A/c | 4,200 | ||||

| (Being cash received from Mr. Sky and discount allowed) | |||||

| Jan.28 | Interest on capital A/c | Dr. | 2,240 | ||

| To Capita A/c | 2,240 | ||||

| (Being allowed interest on capital) | |||||

| Jan.31 | Salaries A/c | Dr. | 300 | ||

| Rent A/c | Dr. | 600 | |||

| To cash A/c | 900 | ||||

| (Being salaries and rent paid) |

| Cash A/c | |||||||

| Date | Particular | J.F. | Amount | Date | Particular | J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To balance b/d | 12,000 | Jan.5 | By Mr. Q’s A/c | 1,200 | ||

| Jan. 15 | To Mr. Y’s A/c | 3,420 | Jan.16 | By Charity A/c | 300 | ||

| Jan.27 | To Mr. Sky’s A/c | 4,020 | Jan.16 | By Stationery A/c | 420 | ||

| Jan.16 | By Postage A/c | 180 | |||||

| Jan.20 | By Mr. P’s A/c | 1,680 | |||||

| Jan.31 | By salaries A/c | 300 | |||||

| Jan.31 | By Rent A/c | 600 | |||||

| Jan.31 | By Balance c/d | 14,760 | |||||

| 19,440 | 19,440 | ||||||

| Feb.1 | To Balance b/d | 14,760 |

| Dr. | Furniture A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Balance b/d | 2,400 | |||||

| 2,400 | |||||||

| Dr. | W’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Balance b/d | 2,400 | |||||

| 2,400 | |||||||

| Dr. | Building A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Balance b/d | 3,600 | |||||

| 3,600 | |||||||

| Dr. | X’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Balance b/d | 2,400 | |||||

| 2,400 | |||||||

| Dr. | Y’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Balance b/d | 3,600 | Jan.15 | By Cash A/c | 3,420 | ||

| Jan.15 | By Discount Allowed A/c | 180 | |||||

| 3,600 | 3,600 | ||||||

| Dr. | Z’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Balance b/d | 3,600 | |||||

| 3,600 | |||||||

| Dr. | P’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.20 | To Cash A/c | 1,680 | Jan.1 | By Balance b/d | 3,600 | ||

| Jan.20 | To Discount received A/c | 120 | |||||

| Jan.31 | To Balance c/d | 1,800 | |||||

| 3,600 | 3,600 | ||||||

| Feb.1 | By Balance b/d | 3,600 | |||||

| Dr. | Q’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.5 | To Cash A/c | 1,200 | Jan.1 | By Balance b/d | 6,000 | ||

| Jan.31 | To Balance c/d | 4,800 | |||||

| 6,000 | 6,000 | ||||||

| Dr. | Capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.31 | To Balance c/d | 55,040 | Jan.1 | By Balance b/d | 52,800 | ||

| Jan.28 | By interest on capital A/c | 2,240 | |||||

| 55,040 | 55,040 | ||||||

| Feb.1 | By Balance b/d | 55,040 | |||||

| Dr. | Mr. Red’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Sales A/c | 1,800 | Jan.31 | By Balance c/d | 1,800 | ||

| 1,800 | 1,800 | ||||||

| Feb.1 | To Balance b/d | 1,800 | |||||

| Dr. | Sales A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.31 | To Balance c/d | 9,243 | Jan.1 | By Mr. Red’s A/c | 1,800 | ||

| Jan.1 | By Mr. White’s A/c | 1,200 | |||||

| Jan.1 | By Mr. Blue’s A/c | 1,800 | |||||

| Jan.21 | By Mr. Sky’s A/c | 4,200 | |||||

| Jan.25 | By Mr. earth’s A/c | 243 | |||||

| 9,243 | 9,243 | ||||||

| Feb.1 | By Balance b/d | 9,243 | |||||

| Dr. | Mr. white’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Sales A/c | 1,200 | Jan.31 | By Balance c/d | 1,200 | ||

| 1,200 | 1,200 | ||||||

| Feb.1 | To Balance b/d | 1,200 | |||||

| Dr. | Mr. Blue’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.1 | To Sales A/c | 1,800 | Jan.31 | By Balance c/d | 1,800 | ||

| 1,800 | 1,800 | ||||||

| Feb.1 | To Balance b/d | 1,800 | |||||

| Dr. | Discount allowed A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.15 | To Mr. Y’s A/c | 180 | Jan.31 | By Balance c/d | 360 | ||

| Jan.27 | To Mr. Sky’s A/c | 180 | |||||

| 360 | 360 | ||||||

| Feb.1 | To Balance b/d | 360 | |||||

| Dr. | Charity A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.16 | To Cash A/c | 300 | Jan.31 | By Balance c/d | 300 | ||

| 300 | 300 | ||||||

| Feb.1 | To Balance b/d | 300 | |||||

| Dr. | Stationery A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.16 | To Cash A/c | 420 | Jan.31 | By Balance c/d | 420 | ||

| 420 | 420 | ||||||

| Feb.1 | To Balance b/d | 420 | |||||

| Dr. | Postage A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.16 | To Cash A/c | 180 | Jan.31 | By Balance c/d | 180 | ||

| 180 | 180 | ||||||

| Feb.1 | To Balance b/d | 180 | |||||

| Dr. | Discount received A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.31 | To Balance c/d | 120 | Jan.20 | By Mr. P’s A/c | 120 | ||

| 120 | 120 | ||||||

| Feb.1 | By Balance b/d | 120 | |||||

| Dr. | Mr. Sky’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.21 | To Sales A/c | 4,200 | Jan.27 | By Cash A/c | 4,020 | ||

| Jan.27 | By Discount allowed A/c | 180 | |||||

| 4,200 | 4,200 | ||||||

| Dr. | Mr. Earth’s A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.25 | To Sales A/c | 243 | Jan.31 | By Balance c/d | 243 | ||

| 243 | 243 | ||||||

| Feb.1 | To Balance b/d | 243 | |||||

| Dr. | Interest on capital A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.25 | To Capital A/c | 2,240 | Jan.31 | By Balance c/d | 2,240 | ||

| 2,240 | 2,240 | ||||||

| Feb.1 | To Balance b/d | 2,240 | |||||

| Dr. | Sales A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.31 | To Cash A/c | 300 | Jan.31 | By Balance c/d | 300 | ||

| 300 | 300 | ||||||

| Feb.1 | To Balance b/d | 300 | |||||

| Dr. | Rent A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| Jan.31 | To Cash A/c | 600 | Jan.31 | By Balance c/d | 600 | ||

| 600 | 600 | ||||||

| Feb.1 | To Balance b/d | 600 | |||||

| Trail Balance A/c | ||||

| S. No. | Name of A/c | L.F. | Debit | Credit |

|---|---|---|---|---|

| 1 | Cash A/c | 14,760 | ||

| 2 | Furniture A/c | 2,400 | ||

| 3 | W’s A/c | 2,400 | ||

| 4 | Building A/c | 36,000 | ||

| 5 | X’s A/c | 2,400 | ||

| 6 | Z’s A/c | 3,600 | ||

| 7 | P’s A/c | 1,800 | ||

| 8 | Q’s A/c | 4,800 | ||

| 9 | Capital A/c | 55,040 | ||

| 10 | Mr. Red’s A/c | 1,800 | ||

| 11 | Salaries A/c | 9,243 | ||

| 12 | Mr. White A/c | 1,200 | ||

| 13 | Mr. Blue A/c | 1,800 | ||

| 14 | Discount allowed A/c | 360 | ||

| 15 | Charity A/c | 300 | ||

| 16 | Stationery A/c | 420 | ||

| 17 | Postage A/c | 180 | ||

| 18 | Discount received A/c | 120 | ||

| 19 | Mr. Earth A/c | 243 | ||

| 20 | Interest on capital A/c | 2,240 | ||

| 21 | Salaries A/c | 300 | ||

| 22 | Rent A/c | 600 | ||

| Total | 71,003 | 71,003 |

Read out the full article to know the meaning of Cash Book

Trial Balance | Explanation | Methods | Examples

Also, Check out the same article in Hindi from the following link

Trial Balance | Explanation | Methods | Examples

Also, Check out the solved question of all Chapters: –

Part-I

Students may choose only one part from the Part II and Part III

Part-II

Part-III

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 2 Chapter No 9 - Unimax Class 11", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax class 11 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 2 Chapter No 9 - Unimax Class 11" instantly.