Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

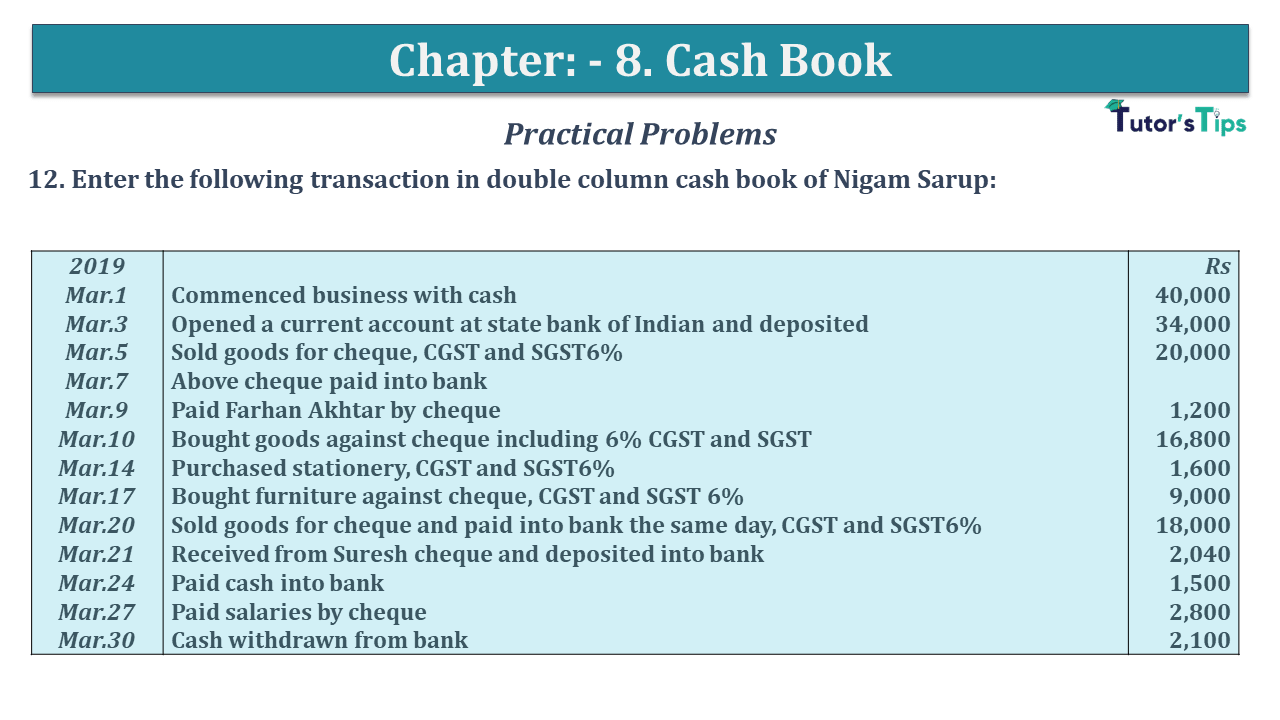

Question No 12 Chapter No 8 - USHA

12. Enter the following transaction in double column cash book of Nigam Sarup:

| 2019 | Rs | |

| Mar.1 | Commenced business with cash | 40,000 |

| Mar.3 | Opened a current account at state bank of Indian and deposited | 34,000 |

| Mar.5 | Sold goods for cheque, CGST and SGST6% | 20,000 |

| Mar.7 | Above cheque paid into the bank | |

| Mar.9 | Paid Farhan Akhtar by cheque | 1,200 |

| Mar.10 | Bought goods against cheque including 6% CGST and SGST | 16,800 |

| Mar.14 | Purchased stationery, CGST and SGST6% | 1,600 |

| Mar.17 | Bought furniture against cheque, CGST and SGST 6% | 9,000 |

| Mar.20 | Sold goods for a cheque and paid into the bank the same day, CGST and SGST6% | 18,000 |

| Mar.21 | Received from Suresh cheque and deposited into bank | 2,040 |

| Mar.24 | Paid cash into the bank | 1,500 |

| Mar.27 | Paid salaries by cheque | 2,800 |

| Mar.30 | Cash is withdrawn from a bank | 2,100 |

| Dr. | Cash Book | Cr. | |||||||

| Date | Parti culars |

L. F. |

Cash | Bank | Date | Partic ulars |

L. F. |

Cash | Bank |

|---|---|---|---|---|---|---|---|---|---|

| 2019 | 2019 | ||||||||

| Mar.1 | To Capital A/c | 40,000 | Mar.1 | By Balance b/d | 34,000 | ||||

| Mar.4 | To Cash A/c | 34,000 | Mar.9 | By Farhan Akhtar A/c | 1,200 | ||||

| Mar.7 | To cheque in hand A/c | 22,400 | Mar.10 | By Purchases A/c | 15,000 | ||||

| Mar.20 | To Sale A/c | 18,000 | Mar.10 | By Input CGST A/c | 900 | ||||

| Mar.20 | To Output CGST A/c | 1,080 | Mar.10 | By Input SGST A/c | 900 | ||||

| Mar.20 | To Output SGST A/c | 1,080 | Mar.14 | By Stationary A/c | 1,600 | ||||

| Mar.21 | To Suresh A/c | 2,040 | Mar.14 | By Input CGST A/c | 96 | ||||

| Mar.24 | To Cash A/c | 1,500 | Mar.14 | By Input SGST A/c | 96 | ||||

| Mar.30 | To Bank A/c | 2,100 | Mar.17 | By Furniture A/c | 9,000 | ||||

| Mar.17 | By Input CGST A/c | 540 | |||||||

| Mar.17 | By Input SGST A/c | 540 | |||||||

| Mar.24 | By Bank A/c | 540 | |||||||

| Mar.27 | By Salaries A/c | 2,800 | |||||||

| Mar.30 | By Cash A/c | 2,100 | |||||||

| Mar.31 | By Balance C/d | 4,080 | 47,120 | ||||||

| 42,100 | 80,100 | 42,100 | 80,100 | ||||||

This is all about the Question No 12 Chapter No 8 - Usha.

You can check out the following article to better understand:

https://tutorstips.com/cash-book/

You Can also read all above articles in Hindi on our Hindi Website

Cash Book | Types of Cash Book – In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in the Question No 12 Chapter No 8 - Usha.

You can also Check out the solved question of other Chapters: -

Chapter No. 2 - Theory Base of Accounting

Chapter No. 3 - Origin of Transactions

Chapter No. 4 - Vouchers and transactions

Chapter No. 6 - Accounting for Goods and Services Tax(GST)

Chapter No. 9 - Other Subsidiary Books

Chapter No. 10 - Journal Proper

Chapter No. 11 - Trial Balance

Chapter No. 12 - Bank Reconciliation Statement

Chapter No. 14 - Provisions and Reserves

Chapter No. 15 - Bills of Exchange

Chapter No. 16 - Rectification of Errors

Chapter No. 17 - Financial Statements - (Without Adjustments)

Chapter No. 18 - Financial Statements - (With Adjustments)

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question No 12 Chapter No 8 - USHA Publication 11 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to USHA Publication +1 Elements of Book-Keeping.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question No 12 Chapter No 8 - USHA Publication 11 Class" instantly.