Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

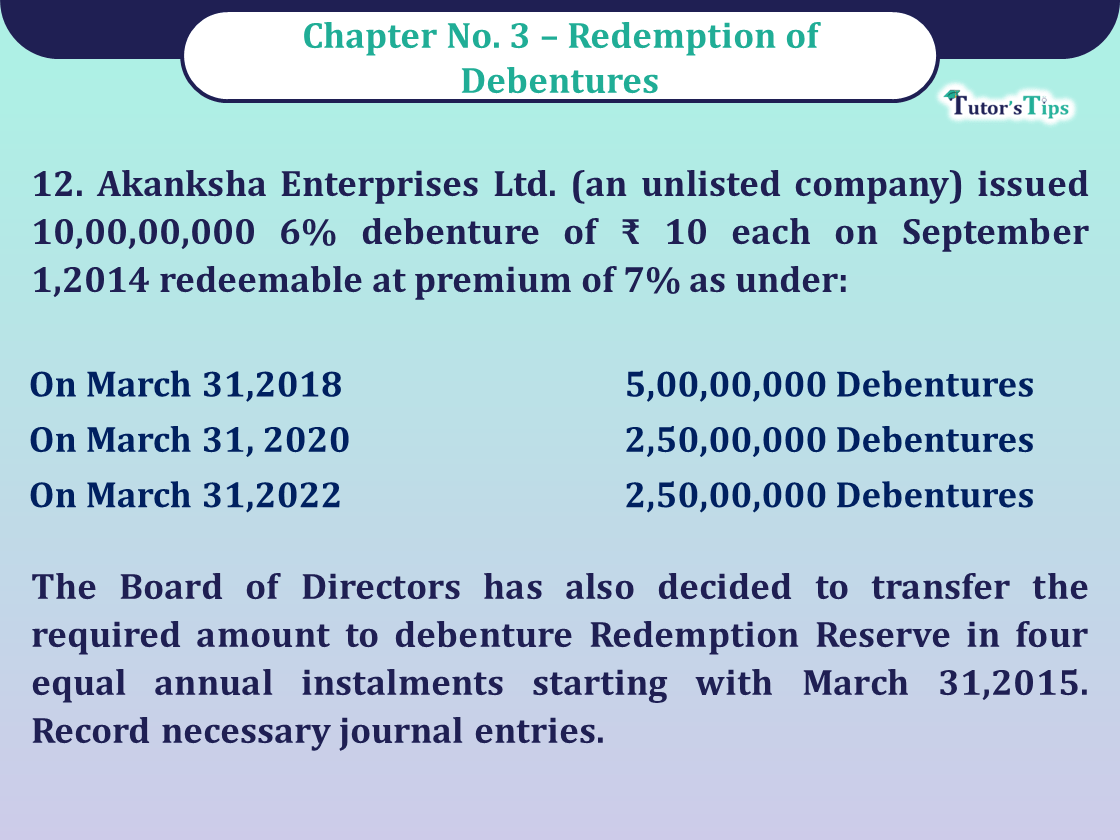

Question No 12 Chapter 3 - UNIMAX Class 12 Part 2 - 2021

Akanksha Enterprises Ltd. (an unlisted company) issued 10,00,00,000 6% debenture of ₹ 10 each on September 1,2014 redeemable at premium of 7% as under:

| On March 31,2018 | 5,00,00,000 Debentures |

| On March 31, 2020 | 2,50,00,000 Debentures |

| On March 31,2022 | 2,50,00,000 Debentures |

The Board of Directors has also decided to transfer the required amount to debenture Redemption Reserve in four equal annual instalments starting with March 31,2015. Record necessary journal entries.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 2014 | |||||

| Bank A/c | Dr. | 100.00 | |||

| To Debenture application & Allotment A/c | 100.00 | ||||

| (Being application and allotment a/c received) | |||||

| Sept. 1 | Debenture application & allotment A/c | Dr. | 100.00 | ||

| Loss on issue of debenture A/c | Dr. | 7.00 | |||

| To Debenture A/c | 100.00 | ||||

| To Premium on Redemption A/c | 7.00 | ||||

| (Being 10 crore 6% debenture issued @ ₹ 10 per debenture redeemable at premium of 7%) | |||||

| March 31 | Statement in Profit & Loss A/c | Dr. | 7.00 | ||

| To Loss on issue of Debenture A/c | 7.00 | ||||

| (Being loss on issue of debenture written off) | |||||

| 2015 March 31 | Surplus statement of Profit & Loss A/c | Dr. | 2.5 | ||

| To Debenture redemption reserve A/c | 2.5 | ||||

| (Being transfer of Profit & Loss DRR) | |||||

| 2016 March 31 | Surplus statement of Profit & Loss A/c | Dr. | 2.5 | ||

| To Debenture redemption reserve A/c | 2.5 | ||||

| (Being transfer of Profit & Loss DRR) | |||||

| 2017 March 31 | Surplus statement of Profit & Loss A/c | Dr. | 2.5 | ||

| To Debenture redemption reserve A/c | 2.5 | ||||

| (Being transfer of Profit & Loss DRR) | |||||

| April 30 | Debenture Redemption Investment A/c | Dr. | 7.5 | ||

| To Bank A/c | 7.5 | ||||

| (Being 15% of face value is invested) | |||||

| 2018 March 31 | Surplus i.e. Balance in P&L A/c | Dr. | 2.5 | ||

| To Debenture redemption reserve A/c | 2.5 | ||||

| (Being profit transferred to create debentures redemption reserve) | |||||

| 2018 March 31 | Debentures A/c | Dr. | 50.00 | ||

| Premium on redemption of debenture A/c | Dr. | 3.50 | |||

| To Debenture holder A/c | 53.50 | ||||

| (Being amount due to debenture holder on redemption of debentures @ ₹ 10 each on 5 crore debenture and premium payable @ 5%p.a.) | |||||

| March 31 | Bank A/c | Dr. | 7.5 | ||

| To Debenture redemption investment A/c | 7.5 | ||||

| (Being investment encashed) | |||||

| 2018 March 31 | Debenture holder A/c | Dr. | 53.50 | ||

| To Bank A/c | 53.50 | ||||

| (Being payment made to debenture holder on redemption of debenture) | |||||

| Debenture redemption reserve A/c | Dr. | 5 | |||

| To General reserve A/c | 5 | ||||

| (Being transfer of proportionate amount of DRR to GR) | |||||

| Apr. 30 | Debenture Redemption Investment A/c | Dr. | 3.75 | ||

| To Bank A/c | 3.75 | ||||

| (Being 15% of face value is invested) | |||||

| 2020 March 31 | Debenture A/c | Dr. | 25.00 | ||

| Premium on Redemption of Debenture A/c | Dr. | 1.75 | |||

| To Debenture holder A/c | 26.75 | ||||

| (Being amount due to debenture holder on redemption of debenture @ ₹ 10 each on 2.5 crore debenture and premium payable @ 7%p.a.) | |||||

| March 31 | Bank A/c | Dr. | 3.75 | ||

| To Debenture redemption investment A/c | 3.75 | ||||

| (Being investment encashed) | |||||

| 2020 March 31 | Debenture holder A/c | Dr. | 26.75 | ||

| To Bank A/c | 26.75 | ||||

| (Being payment made to debenture holder on redemption of debenture) | |||||

| Debenture redemption reserve A/c | Dr. | 2.5 | |||

| To General reserve A/c | 2.5 | ||||

| (Being transfer of proportionate amount of DRR to GR) | |||||

| Apr. 30 | Debenture Redemption Investment A/c | Dr. | 3.75 | ||

| To Bank A/c | 3.75 | ||||

| (Being 15% of face value is invested) | |||||

| 2022 March 31 | Debenture A/c | Dr. | 25.75 | ||

| Premium on Redemption of Debenture A/c | Dr. | 1.75 | |||

| To Debenture holder A/c | 26.50 | ||||

| (Being amount due to debenture holder on redemption of debenture @ ₹ 10 each on 2.5 crore debenture and premium payable @ 5%p.a.) | |||||

| March 31 | Bank A/c | Dr. | 3.75 | ||

| To Debenture redemption investment A/c | 3.75 | ||||

| (Being investment encashed) | |||||

| 2022 March 31 | Debenture holder A/c | Dr. | 26.75 | ||

| To Bank A/c | 26.75 | ||||

| (Being payment made to debenture holder on redemption of debenture) | |||||

| March 31 | Debenture Redemption Reserve A/c | Dr. | 2.5 | ||

| To General reserve A/c | 2.5 | ||||

| (Being transfer of Proportionate amount of DRR to GR) | |||||

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

https://tutorstips.com/share-capital-meaning-types-and-classes/

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question no 12 Chapter 3 - UNIMAX Class 12 Part 2 - 2021", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax Publication Class 12 Part 2 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question no 12 Chapter 3 - UNIMAX Class 12 Part 2 - 2021" instantly.