Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

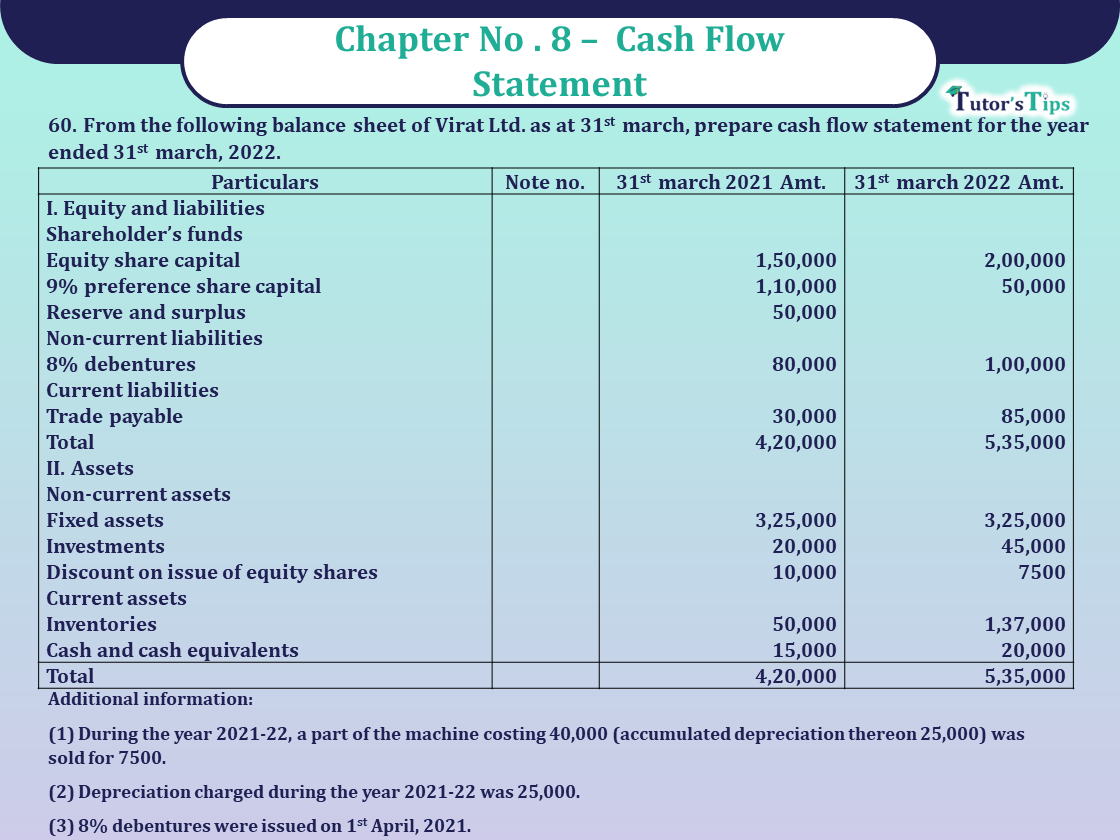

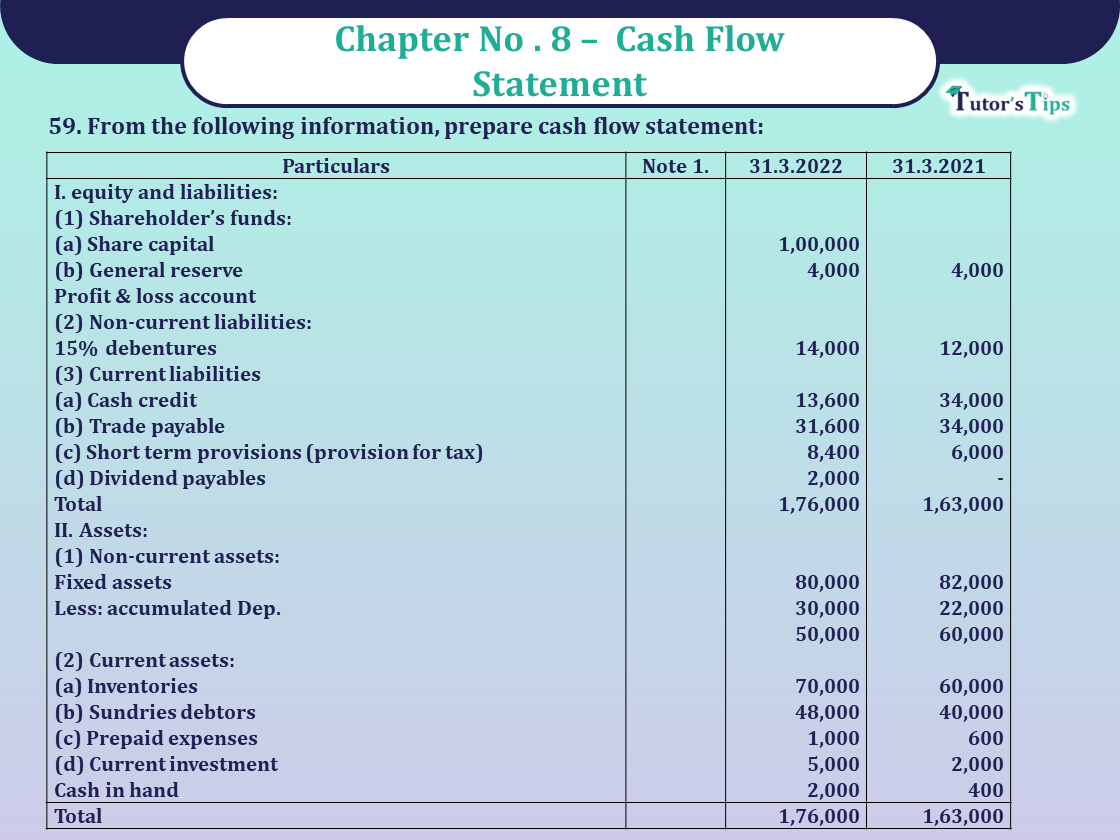

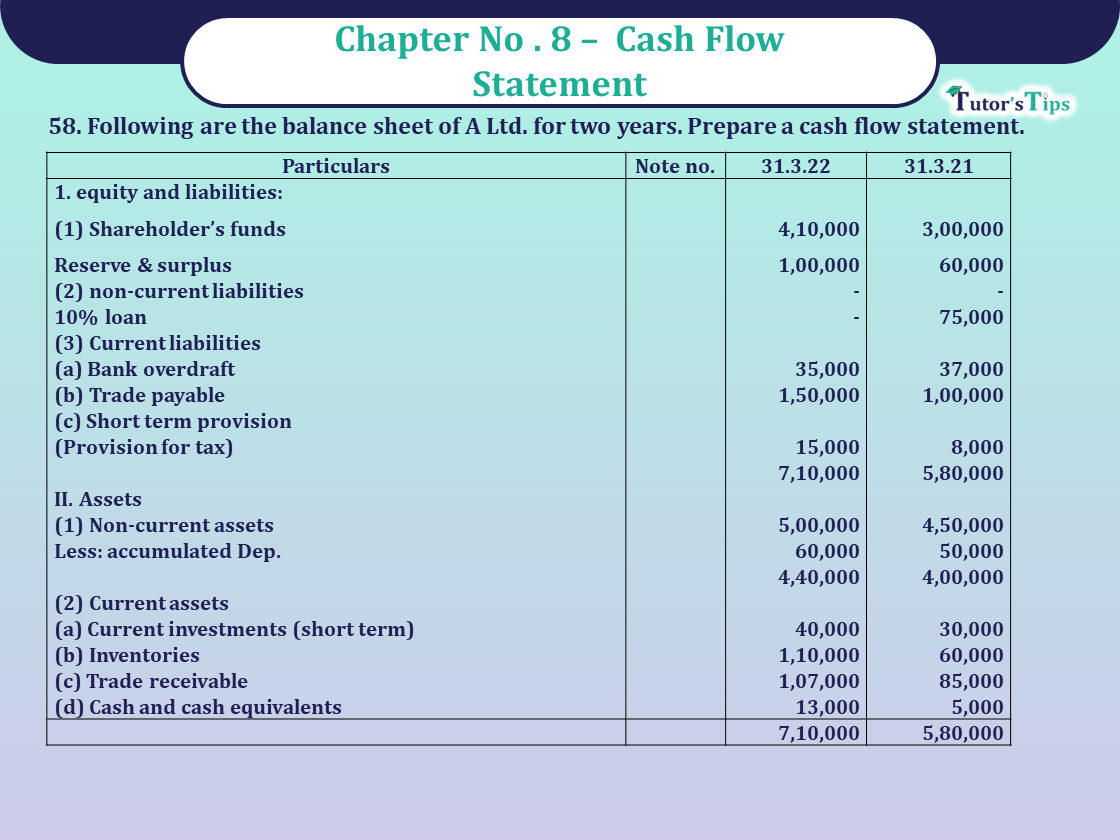

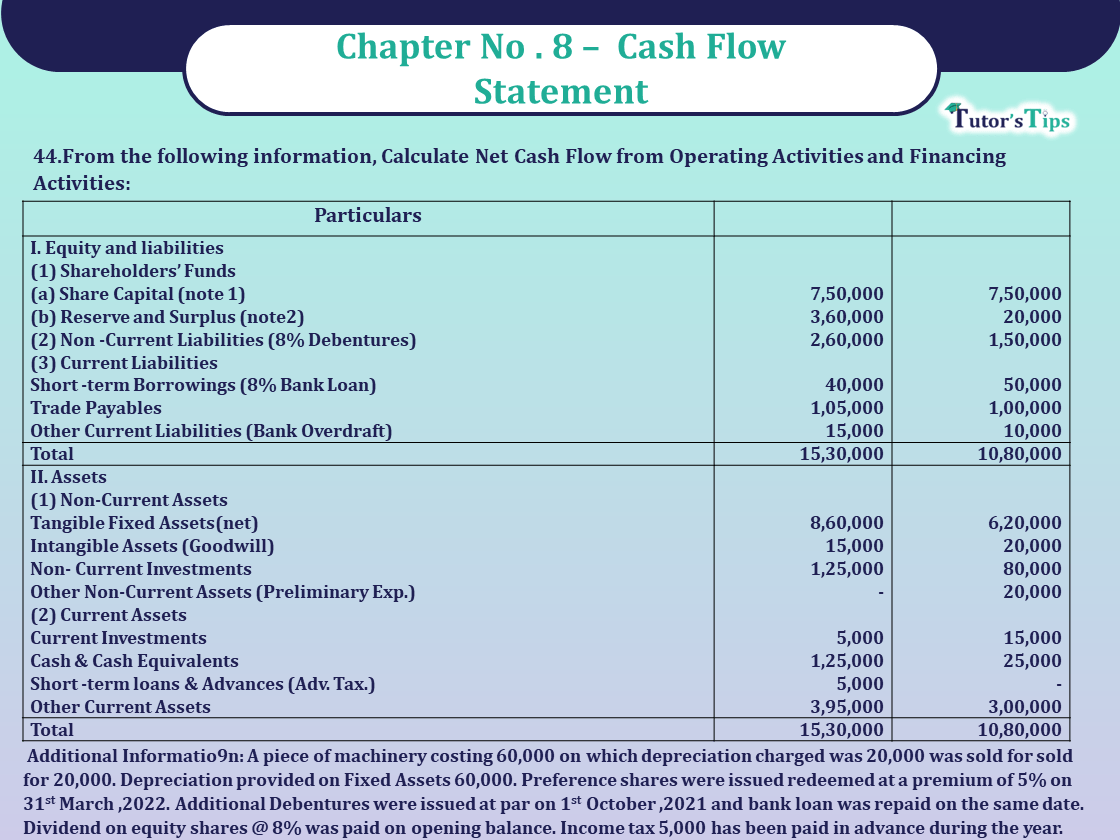

Question 44 Chapter 8 - Unimax Publication Class 12 Part 2 - 2021

44.From the following information, Calculate Net Cash Flow from Operating Activities and Financing Activities:

BALANCE SHEETS AS AT…….

| Particulars | 31.3.2022 | 31.3.2021 |

|---|---|---|

| I. Equity and liabilities | ||

| (1) Shareholders’ funds | ||

| (a)Share Capital (Note1) | 7,50,000 | 7,50,000 |

| (b)Reserves and surplus (note2) | 3,60,000 | 20,000 |

| (2) Non- Current Liabilities (18% Debentures) | 2,60,000 | 1,50,000 |

| (3) Current Liabilities | ||

| Short -term Borrowings (8% Bank Loan) | 40,000 | 50,000 |

| Trade Payables | 1,05,000 | 1,00,000 |

| Other Current Liabilities (Bank Overdraft) | 15,000 | 10,000 |

| Total | 15,30,000 | 10,80,000 |

| B. Assets | ||

| (1) Non-Current Assets | ||

| Tangible Fixed Assets (Net) | 8,60,000 | 6,20,000 |

| Intangible Assets (Goodwill) | 15,000 | 20,000 |

| Non- Current Investments | 1,25,000 | 80,000 |

| Non- Current Investments | - | 20,000 |

| (2) Current Assets | ||

| Current Investments | 5,000 | 15,000 |

| Cash & Cash Equivalents | 1,25,000 | 25,000 |

| Short -term loans & Advances (Adv. Tax.) | 5,000 | - |

| Other Current Assets | 3,95,000 | 3,00,000 |

| Total | 15,30,000 | 10,80,000 |

NOTE 1: SHARE CAPITAL

| Particulars | 31.3.2022 ₹ | 31.3.2021 ₹ |

|---|---|---|

| Equity Share Capital | 5,50,000 | 4,50,000 |

| 5% Pref. Share Capital | 2,00,000 | 3,00,000 |

| 7,50,000 | 7,50,000 |

NOTE 2: RESERVES AND SURPLUS

| Particulars | 31.3.2022 ₹ | 31.3.2021 ₹ |

|---|---|---|

| General Reserve | 1,50,000 | 1,20,000 |

| Profit and Loss A/c | 2,00,000 | (1,00,000) |

| Securities premium | 10,000 | - |

| 1,70,000 | 20,000 |

Additional Information: A piece of machinery costing 60,000 on which depreciation charged was 20,000 was sold for sold for 20,000. Depreciation provided on Fixed Assets 60,000. Preference shares were issued redeemed at a premium of 5% on 31st March ,2022. Additional Debentures were issued at par on 1st October ,2021 and bank loan was repaid on the same date. Dividend on equity shares @ 8% was paid on opening balance. Income tax 5,000 has been paid in advance during the year.

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31st MARCH . 2022

| Particulars | ₹ | ₹ |

|---|---|---|

| I. cash flow from operating activities | ||

| Net profit before tax | 3,81,000 | |

| Adjustment for Non-Cash and Non-Operating Activities | ||

| Dep. on Fixed Assets | 60,000 | |

| Loss on sale of machinery | 20,000 | |

| Interest on Debentures | ||

| (1,50,000 x 8/100) +(1,10,000 x 8/100 x 6/12) | 16,400 | |

| Interest on Bank Loan | ||

| (50,000 x 8/100 x 6/12) +(40,000 x 8/100 x 6/12) | 3,600 | |

| Goodwill Amort | 5,000 | |

| Preliminary Exp. written off | 20,000 | |

| Premium on Redemption of Preference Shares | 5,000 | 1,30,000 |

| Operating Profit before Working Capital Changes | 5,11,000 | |

| Change in CA &CL | ||

| Increase in other CA | (95,000) | |

| Increase in CL | 5,000 | (90,000) |

| Net Cashflow from Op. Activities before Tax | 4,21,000 | |

| Less Tx Paid | (5,000) | |

| Net Cashflow from Op. Activities after Tax | 4,16,000 | |

| II. Cash Flow from Investing Activities: | ||

| Sale | 20,000 | |

| Purchase | (3,40,000) | (3,65,000) |

| Investment Purchase | (45,000) | |

| III. Cash Flow from Financing Activities: | ||

| Issue of Share Capital (1,00,000+10,000) | 1,10,000 | |

| Issue of Debentures | 1,10,000 | |

| Interest on Debentures | (16,400) | |

| Interest on Bank Loan | (3,600) | |

| Dividend on Equity Shares | (36,000) | |

| Dividend on Preference Shares | (15,000) | |

| Redemption of Preference Shares (1,00,000+5,000) | (1,05,000) | |

| Bank Loan Repaid | (5,000) | |

| Net Cash used from Financing Activities | (39,000) |

Working Notes: (1)

| 1.Calculation of net profit before tax | ₹ |

| Closing Balance of profit &loss A/c | 2,00,000 |

| Add: Opening Balance of P&L A/c (Dr.) | 1,00,000 |

| Add: Transfer to Reserves | 30,000 |

| Add: Dividend on Equity Shares | 36,000 |

| Add: Dividend on Pref. Shares | 15,000 |

| Net profit before tax | 3,81,000 |

Working Notes: (2)

2. FIXED ASSETS ACCCOUNT

| Particulars | ₹ | Particulars | ₹ |

|---|---|---|---|

| TO Balance b/d | 6,20,000 | By Dep A/c | 60,000 |

| To Bank A/c (Purchase) (b. f) | By Bank A/c Sales | 20,000 | |

| (Purchased B. fig) | 3,40,000 | By P& L A/c Loss | 20,000 |

| By Balance c/d | 8,60,000 | ||

| 9,60,000 | 9,60,000 |

Thanks, Please Like and share with your friends

Comment if you have any Doubts.

https://tutorstips.com/what-is-the-cash-flow-statement-why-do-we-need-prepare/

Check out T.S. Grewal +2 Book 2023@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 44 Chapter 8 -Unimax Publication Class 12 Part 2 - 2021", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax Publication Class 12 Part 2 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 44 Chapter 8 -Unimax Publication Class 12 Part 2 - 2021" instantly.