Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

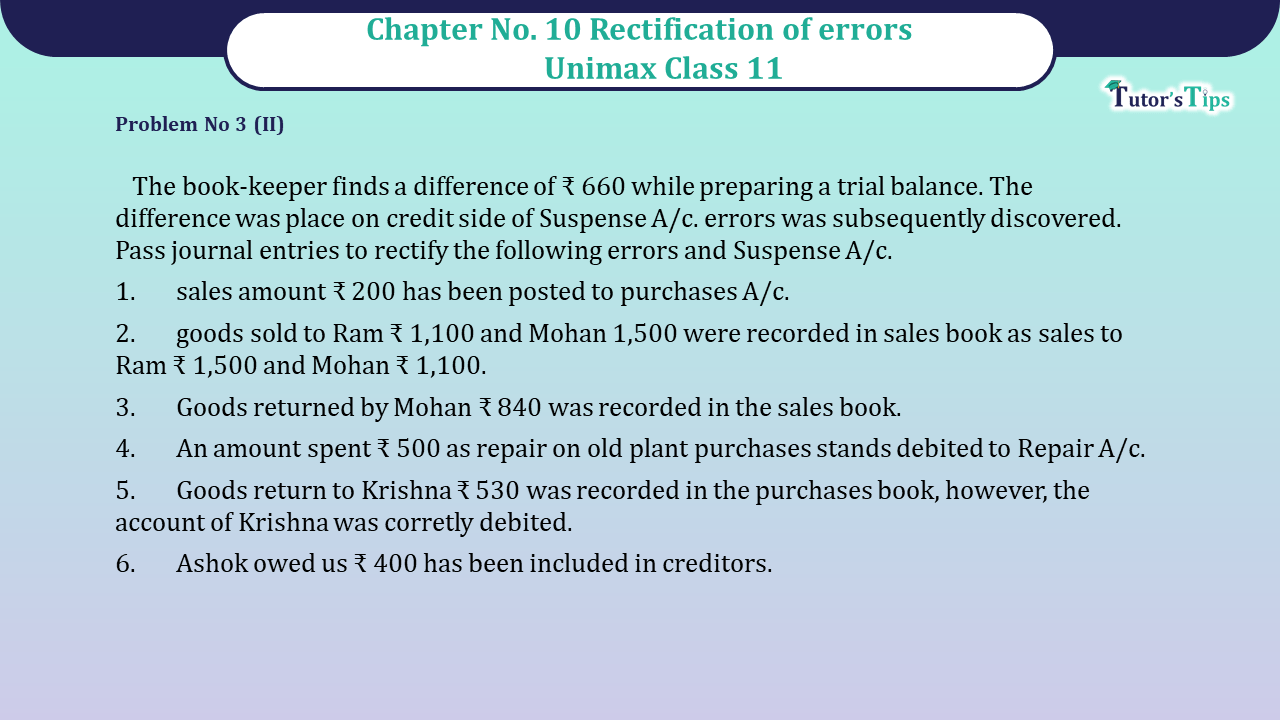

Problem No 3 (II) Chapter No 10 - Unimax Class 11

| The bookkeeper finds a difference of ₹ 660 while preparing a trial balance. The difference was place on credit side of Suspense A/c. errors was subsequently discovered. Pass journal entries to rectify the following errors and Suspense A/c. |

| 1. sales amount ₹ 200 has been posted to purchases A/c. |

| 2. goods sold to Ram ₹ 1,100 and Mohan 1,500 were recorded in sales book as sales to Ram ₹ 1,500 and Mohan ₹ 1,100. |

| 3. Goods returned by Mohan ₹ 840 was recorded in the sales book. |

| 4. An amount spent ₹ 500 as repair on old plant purchases stands debited to Repair A/c. |

| 5. Goods return to Krishna ₹ 530 was recorded in the purchases book, however, the account of Krishna was correctly debited. |

| 6. Ashok owed us ₹ 400 has been included in creditors. |

Journal

| S. No. | Particulars | L.F. | Debit | Credit | ||

|---|---|---|---|---|---|---|

| 1 | Suspense A/c | Dr. | 400 | |||

| To Sales A/c | 200 | |||||

| To Purchases A/c | 200 | |||||

| (Being sales posted to purchases A/c, now rectified) | ||||||

| 2 | Mohan’s A/c | Dr. | 400 | |||

| To Ram’s A/c | 400 | |||||

| (Being sales to Ram & Mohan of ₹ 1,100 and ₹ 1,500 respectively but amount recorded inter changebly, now rectified) | ||||||

| 3 | Sales returns A/c | Dr. | 840 | |||

| Sales A/c | Dr. | 840 | ||||

| To Mohan’s A/c | 1,680 | |||||

| (Being goods returned by Mohan wrongly entered in sales book, now rectified) | ||||||

| 4 | Plant A/c | Dr. | 500 | |||

| To Repair A/c | 500 | |||||

| (Being paid for repair of old plant purchases debited to repair a/c, now rectified) | ||||||

| 5 | Suspense A/c | Dr. | 1,060 | |||

| To Purchases A/c | 530 | |||||

| To Purchases return A/c | 530 | |||||

| (Being goods return to Krishna, recorded in purchases book, now rectified) | ||||||

| 6 | Sundry Debtors A/c | Dr. | 400 | |||

| Sundry creditors A/c | Dr. | 400 | ||||

| To Suspense A/c | 800 | |||||

| (Being owned by Ashok entered in S. creditors, now rectified) | ||||||

| Dr. | Suspense A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

|---|---|---|---|---|---|---|---|

| To Sales A/c | 200 | By Balance c/d | 660 | ||||

| To Purchases A/c | 200 | By Sundry Debtors A/c | 400 | ||||

| To Purchases A/c | 530 | By Sundry Creditors A/c | 400 | ||||

| To Purchases return A/c | 530 | ||||||

| 1,460 | 1,460 | ||||||

Read out the full article to know the meaning of Rectification of Errors

Error Rectification in accounting – Explanation with examples

Also, Check out the same article in Hindi from the following link

Error Rectification in accounting – Explanation with examples-in Hindi

Also, Check out the solved question of all Chapters: –

Part-I

Students may choose only one part from the Part II and Part III

Part-II

Part-III

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Problem No 3 (II) Chapter No 10 - Unimax 11 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax class 11 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Problem No 3 (II) Chapter No 10 - Unimax 11 Class" instantly.