Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

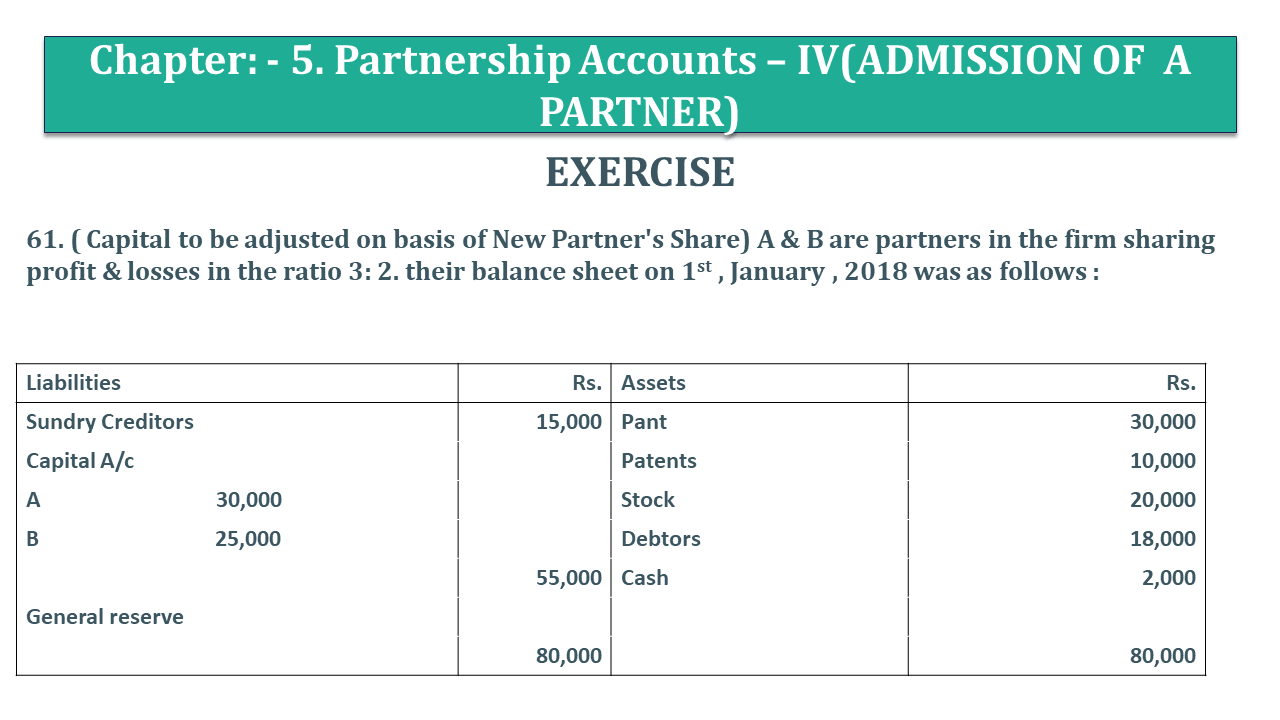

Question 61 Chapter 5 of +2-Part-1

61. ( Capital to be adjusted on the basis of New Partner's Share) A & B are partners in the firm sharing profit & losses in the ratio 3: 2. their balance sheet on 1st, January 2018 was as follows :

| Liabilities | Rs. | Assets | Rs. | |

| Sundry Creditors | 15,000 | Pant | 30,000 | |

| Capital A/c | Patents | 10,000 | ||

| A | 30,000 | Stock | 20,000 | |

| B | 25,000 | Debtors | 18,000 | |

| 55,000 | Cash | 2,000 | ||

| General reserve | 10,000 | |||

| 80,000 | 80,000 |

C is admitted as a partner on the above date on the following terms: (1) He will pay Rs. 10,000 as goodwill for one-fourth share in the profits of the firm.

(ii) The assets are to be valued as under. Plant at Rs. 32,000; Stock at Rs. 18,000; Debtors at book figure less a provision of 5per cent for doubtful debts.

(iii) It was found that creditors included a sum of Rs. 1,400 which was not to be paid. But it was also found that there was a liability for compensation to workers amounting to Rs. 2,000.

(iv) C was to introduce 20,000 as capital and the capitals of the other partners were to be adjusted in the new profit-sharing ratio. For this purpose, current accounts were to be opened. Give journal entries to record the above and the balance sheet after C's admission (ledger accounts are not required).

We are providing a solution of Question 61 Chapter 5 of +2 Part-1 in two formats. one is in Video format and another is in article format. Check out both formats as follows:

The video consists solution of question numbers from 61 to 62 Chapter no. 5 class 12 of Usha publication. To check the direct solution of question no. 61 from the following video by using time stamps of the video.

Journal

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Cash A/c | Dr. | 30,000 | |||

| To C’s capital A/c | 20,000 | ||||

| To Premium for Goodwill A/c | 10,000 | ||||

| (Being amount brought in by C as his capital and share of goodwill) | |||||

| Premium A/c | Dr. | 10,000 | |||

| To A’s Capital A/c | 6,000 | ||||

| To B’s Capital A/c | 4,000 | ||||

| (Being amount of goodwill transferred to the capital A/c of old partners in the ratio of their sacrifice Ratio i.e., 3:2) | |||||

| Revaluation A/c | Dr. | 4,900 | |||

| To Workers Compensation Payable A/c | 2,000 | ||||

| To Stock | 900 | ||||

| To provisional for doubtful debts A/c) | 2,000 | ||||

| (Being decrease in the value of various assets on C’s admission) | |||||

| Plant A/c | Dr. | 2,000 | |||

| Sundry creditors | Dr. | 1,400 | |||

| To Revaluation A/c | 3,400 | ||||

| (Being the increase in the value of the plant & decrease in the value of liabilities on C’s admission ) | |||||

| A’s Capital A/c | Dr. | 900 | |||

| B’s Capital A/c | Dr. | 600 | |||

| To Revaluation A/c | 1,500 | ||||

| (Being the profit on revaluation transferred to capital A/c of the old partners in the old sharing ratio ) | |||||

| General reserve | Dr. | 10,000 | |||

| To A’s capital A/c | 6,000 | ||||

| To B’s Capital A/c | 4,000 | ||||

| (Being general reserve distributed among old partners in their old profit sharing ratio ) | |||||

| A’s capital A/c | Dr. | 5,100 | |||

| To A’s current A/c | 5,100 | ||||

| (Being General reserve distributed) | |||||

| B’s capital A/c | Dr. | 8,400 | |||

| To B’s current A/c | 8,400 | ||||

| (Being excess of the capital A/c transferred to the current A/c | |||||

Balance Sheet

| Liabilities |

Amount | Assets | Amount | ||

|---|---|---|---|---|---|

| Sundry Creditors | 13,600 | 32,000 | |||

| Work compensation payable A/c | 2,000 | Debtors | 18,000 | ||

| Current A/c s | (-) Prov. For D/D | 900 | 17,100 | ||

| A | 5,100 | Stock | 18,000 | ||

| B | 8,400 | 13,500 | Patents | 10,000 | |

| Capital A/c | Cash | 32,000 | |||

| A | 36,000 | ||||

| B | 24,000 | ||||

| C | 20,000 | 80,000 | |||

| 1,09,100 | 1,09,100 | ||||

Working Note:

Calculation of New Profit Sharing Ratio:

Remaining Share for Old partners = Total Profit - Share of New Partner

= 1 - 1/4

=4-1/4

=3/4

Now, Distribute the remaining share among old Partners :

New Share of Partner = Remaining Share X Old Share of Partner

New Share of A = 3/4 X 3/5

= 9/20

New Share of B = 3/4 X 2/5

= 6/20

Now make the same denominator of All partners

So, C's New Ratio = 1/4 X 5/5

= 5/20

New Profit Sharing Ratio = 9:6:5

Now, Calculate the Closing balance of A and B capital according to the new profit-sharing ratio

So, Firstly Calculate:

Total Capital of Firm = Amount invested by the New Partner X Reciprocal of Share of New Partner

= 20,000 X 4/1

= 80,000/-

Now Calculate:

A's New Capital Balance = Total Capital of Firm X A's New Share

= 80,000 X 9/20

= 36,000/-

B's New Capital Balance = Total Capital of Firm X B's New Share

= 80,000 X 6/20

= 24,000/-

Now according to the question, we have to adjust the capital balance with the current account.

Partner's Capital A/c

| Particulars | A | B | C | Particulars | A | B | C |

|---|---|---|---|---|---|---|---|

|

To P/L App. (Loss) |

900 |

600 |

- |

By Bal. B/d |

30,000 |

25,000 |

- |

|

By Bank a/c |

- |

- |

20,000 |

||||

|

By Goodwill |

6,000 |

4,000 |

- |

||||

|

By General Res. |

6,000 |

4,000 |

- |

||||

|

To Current A/c (B.Fig) |

5,1,00 |

8,400 |

- |

||||

|

To Bal. c/d |

36,000 |

24,000 |

20,000 |

||||

|

42,000 |

33,000 |

20,000 |

42,000 |

33,000 |

20,000 |

Comment if you have any questions.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 61 Chapter 5 of +2 Part-1 - USHA Publication 12 Class Part - 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to USHA Publication +2 Part 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 61 Chapter 5 of +2 Part-1 - USHA Publication 12 Class Part - 1" instantly.

16 June 2023

19 June 2023