Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Question 61 Chapter 5 of +2-A

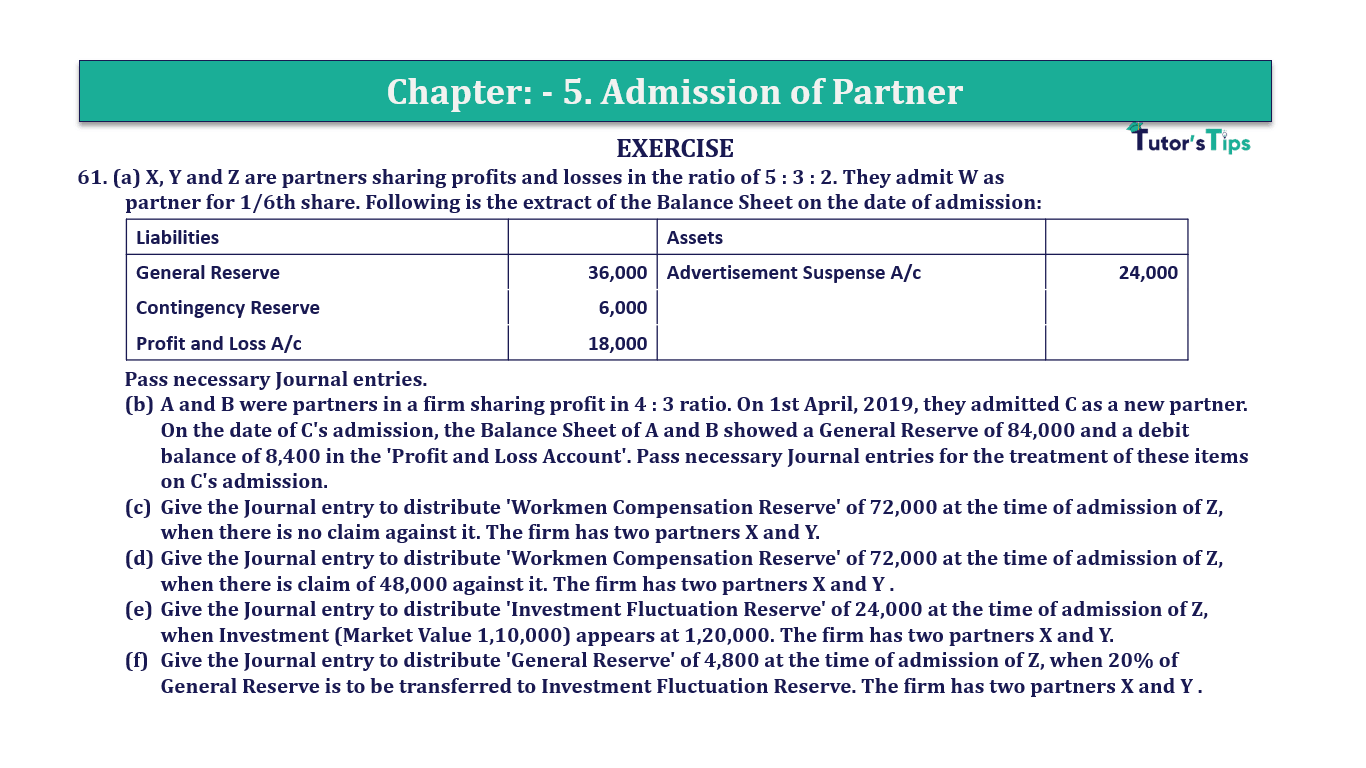

61. (a) X, Y and Z are partners sharing profits and losses in the ratio of 5 : 3 : 2. They admit W as partner for 1/6th share. Following is the extract of the Balance Sheet on the date of admission:

| Liabilities | Assets | ||

| General Reserve | 36,000 | Advertisement Suspense A/c | 24,000 |

| Contingency Reserve | 6,000 | ||

| Profit and Loss A/c | 18,000 |

Pass necessary Journal entries.

b. A and B were partners in a firm sharing profit in 4 : 3 ratio. On 1st April, 2019, they admitted C as a new partner. On the date of C's admission, the Balance Sheet of A and B showed a General Reserve of 84,000 and a debit balance of 8,400 in the 'Profit and Loss Account'. Pass necessary Journal entries for the treatment of these items on C's admission.

c. Give the Journal entry to distribute 'Workmen Compensation Reserve' of 72,000 at the time of admission of Z, when there is no claim against it. The firm has two partners X and Y.

d. Give the Journal entry to distribute 'Workmen Compensation Reserve' of 72,000 at the time of admission of Z, when there is claim of 48,000 against it. The firm has two partners X and Y .

e. Give the Journal entry to distribute 'Investment Fluctuation Reserve' of 24,000 at the time of admission of Z, when Investment (Market Value 1,10,000) appears at 1,20,000. The firm has two partners X and Y.

f. Give the Journal entry to distribute 'General Reserve' of 4,800 at the time of admission of Z, when 20% of General Reserve is to be transferred to Investment Fluctuation Reserve. The firm has two partners X and Y .

g. A, B and C were partners sharing profits and losses in the ratio of 6 : 3 : 1. They decide to take D into partnership with effect from 1st April, 2019. The new profit-sharing ratio between A, B, C and D will be 3 : 3 : 3 : 1. They also decide to record the effect of the following without affecting their book values, by passing a single adjustment entry:

| Book Values ( ) | |

| General Reserve | 1,50,000 |

| Contingency Reserve | 60,000 |

| Profit and Loss A/c (Cr.) | 90,000 |

| Advertisement Suspense A/c (Dr.) | 1,20,000 |

Pass the necessary single adjustment entry, through the Partner's Current Account

Case A

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| General Reserve A/c | Dr | 36,000 | |||

| Contingency Reserve A/c | Dr | 6,000 | |||

| Profit and Loss A/c | Dr | 18,000 | |||

| To X’s Capital A/c | 30,000 | ||||

| To Y’s Capital A/c | 18,000 | ||||

| To Z’s Capital A/c | 12,000 | ||||

| (Being distributed the balance of general reserve, Contingency Reserve and profit and loss account among the old partners in their old profit sharing ratio i.e. 5:3:2) | |||||

| X’s Capital A/c | Dr | 12,000 | |||

| Y’s Capital A/c | Dr | 7,200 | |||

| Z’s Capital A/c | Dr | 4,800 | |||

| To Advertisement Suspense A/c | 24,000 | ||||

| (Being distributed the balance of Advertisement Suspense among the old partners in their old profit sharing ratio i.e. 5:3:2) | |||||

| Revaluation A/c | Dr | 270 | |||

| To Motors A/c | 250 | ||||

| To Furniture A/c | 20 | ||||

| (Being Decrease in value of Motors and Furniture transferred to Revaluation Account) | |||||

Case B

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| General Reserve A/c | Dr | 84,000 | |||

| To A’s Capital A/c | 48,000 | ||||

| To B’s Capital A/c | 36,000 | ||||

| (Being distributed the balance of general reserve among the old partners in their old profit sharing ratio i.e. 4:3) | |||||

| A’s Capital A/c | Dr | 4,800 | |||

| B’s Capital A/c | Dr | 3,600 | |||

| To Profit & Loss A/c | 8,400 | ||||

| (Being distributed the balance of Profit & Loss among the old partners in their old profit sharing ratio i.e. 4:3 | |||||

Case C

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Workmen Compensation Reserve A/c | Dr | 72,000 | |||

| To X’s Capital A/c | 36,000 | ||||

| To Y’s Capital A/c | 36,000 | ||||

| (Being distributed the balance of Workmen Compensation Reserve among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case D

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Workmen Compensation Reserve A/c | Dr | 72,000 | |||

| To Workmen Compensation Reserve claim A/c | 48,000 | ||||

| To X’s Capital A/c | 12,000 | ||||

| To Y’s Capital A/c | 12,000 | ||||

| (Being distributed the balance of Workmen Compensation Reserve among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case E

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| Investment Fluctuation Reserve A/c | Dr | 24,000 | |||

| To Investment A/c | 10,000 | ||||

| To X’s Capital A/c | 7,000 | ||||

| To Y’s Capital A/c | 7,000 | ||||

| (Being distributed the balance of Workmen Compensation Reserve among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case F

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| General Reserve A/c | Dr | 4,800 | |||

| To Investment Fluctuation Reserve A/c | 960 | ||||

| To X’s Capital A/c | 1,920 | ||||

| To Y’s Capital A/c | 1,920 | ||||

| (Being distributed the balance of General Reserve after transfer to the Investment Fluctuation Reserve from it among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case G

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| C’s Current A/c | Dr | 36,000 | |||

| D’s Current A/c | Dr | 18,000 | |||

| To A’s Current A/c | 54,000 | ||||

| (Being adjustment made at the time of admission of A) | |||||

| Old Ratio of A,B, and C | = | 6 : 3 : 3 |

| New Ratio of A,B, C, and D | = | 3 : 3 : 3 : 1 |

Sacrificing Share = Old Ratio - New Ratio

| X’s Sacrificing/Gaining Share | = | 6 | - | 3 |

| 10 | 10 |

| = | 6 - 3 |

| 10 |

| = | 3 | Sacrifice |

| 10 |

| Y’s Sacrificing/Gaining Share | = | 3 | - | 3 |

| 10 | 10 |

| = | 3 - 3 |

| 10 |

| = | 0 |

| 10 |

| Z’s Sacrificing/Gaining Share | = | 1 | - | 3 |

| 10 | 10 |

| = | 1 - 3 |

| 10 |

| = | -2 | Gains |

| 10 |

| W’s Sacrificing/Gaining Share | = | 1 |

| 10 |

Calculation of Net Effect

| General Reserve | 1,50,000 | |

| Add: - Contingency Reserve | 60,000 | |

| Add: -Profit and Loss A/c (Cr.) | 90,000 | |

| 3,00,000 | ||

| Less: Advertisement Suspense A/c (Dr.) | - 1,20,000 | |

| 1,80,000 | ||

Adjustment of Revaluation Profit

| A will Get from C & D | = | 1,80,000 | X | 3 |

| 10 | ||||

| = | 54,000 |

| C will pay to A | = | 1,80,000 | X | 2 |

| 10 | ||||

| = | 36,000 |

| D will pay to Z | = | 1,80,000 | X | 1 |

| 10 | ||||

| = | 18,000 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Q.No.61 | Chapter 5 – Admission of Partner | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.61 | Chapter 5 – Admission of Partner | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.