Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

Question 60 Chapter 5 of +2-B

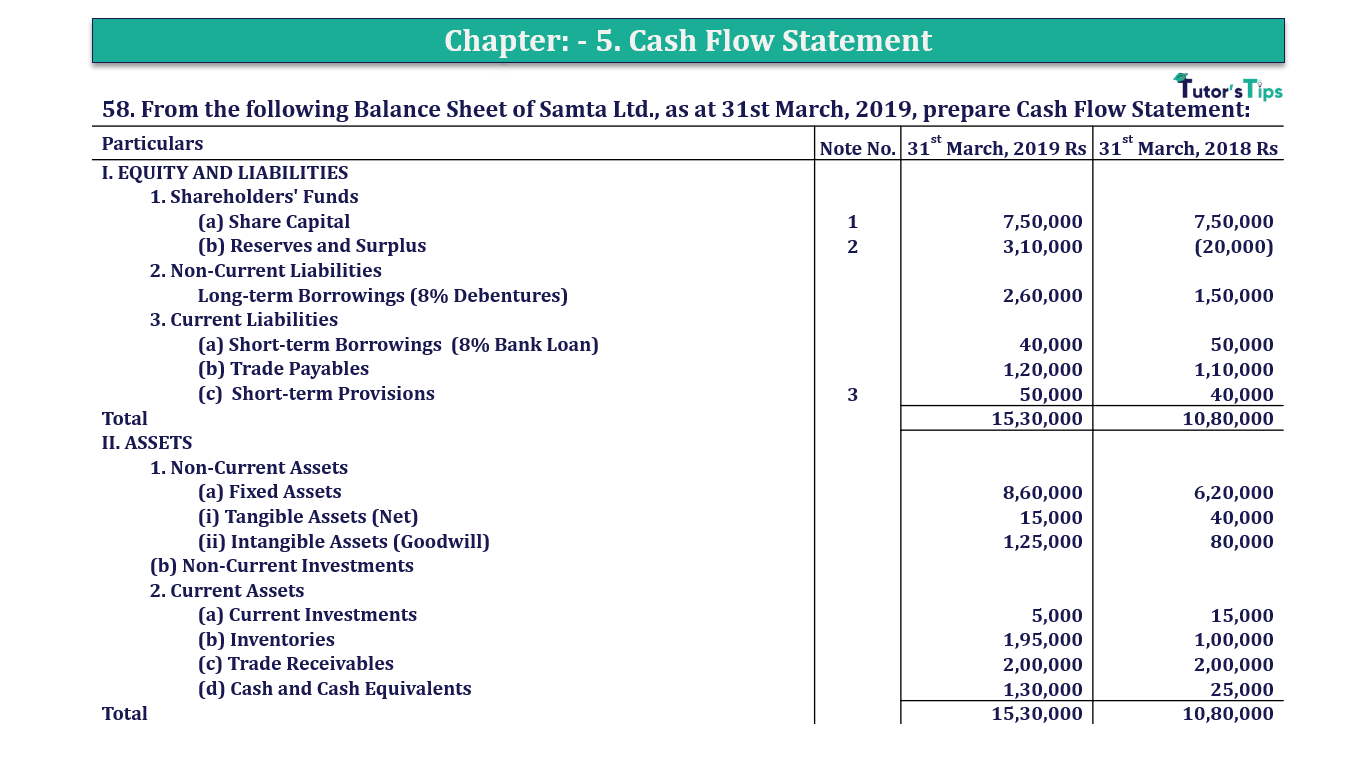

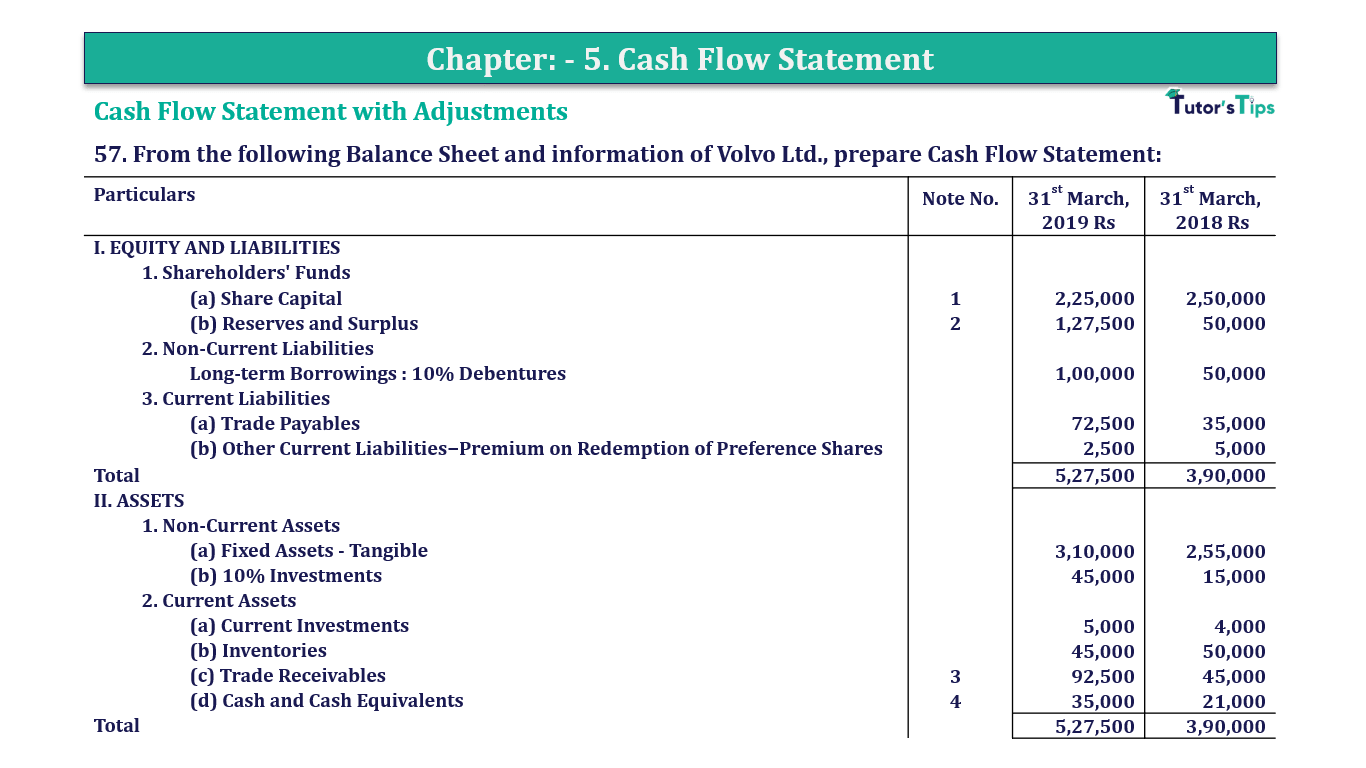

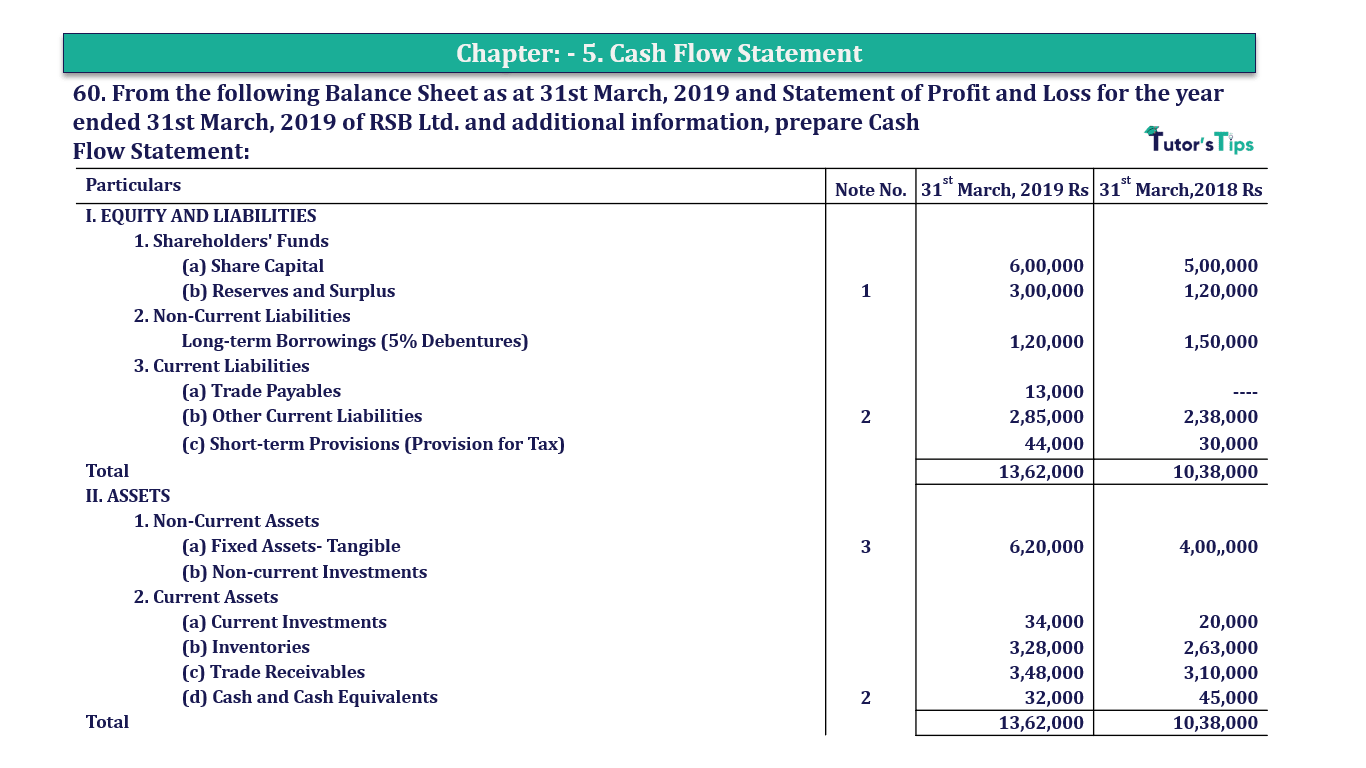

60. From the following Balance Sheet as at 31st March, 2019 and Statement of Profit and Loss for the year ended 31st March, 2019 of RSB Ltd. and additional information, prepare Cash Flow Statement:

| Particulars | Note No. | 31st March, 2019 Rs | 31st March,2018 Rs |

| I. EQUITY AND LIABILITIES | |||

| 1. Shareholders' Funds | |||

| (a) Share Capital | 6,00,000 | 5,00,000 | |

| (b) Reserves and Surplus | 1 | 3,00,000 | 1,20,000 |

| 2. Non-Current Liabilities | |||

| Long-term Borrowings (5% Debentures) | 1,20,000 | 1,50,000 | |

| 3. Current Liabilities | |||

| (a) Trade Payables | 13,000 | ---- | |

| (b) Other Current Liabilities | 2 | 2,85,000 | 2,38,000 |

| (c) Short-term Provisions (Provision for Tax) | 44,000 | 30,000 | |

| Total | 13,62,000 | 10,38,000 | |

| II. ASSETS | |||

| 1. Non-Current Assets | |||

| (a) Fixed Assets- Tangible | 3 | 6,20,000 | 4,00,,000 |

| (b) Non-current Investments | |||

| 2. Current Assets | |||

| (a) Current Investments | 34,000 | 20,000 | |

| (b) Inventories | 3,28,000 | 2,63,000 | |

| (c) Trade Receivables | 3,48,000 | 3,10,000 | |

| (d) Cash and Cash Equivalents | 2 | 32,000 | 45,000 |

| Total | 13,62,000 | 10,38,000 |

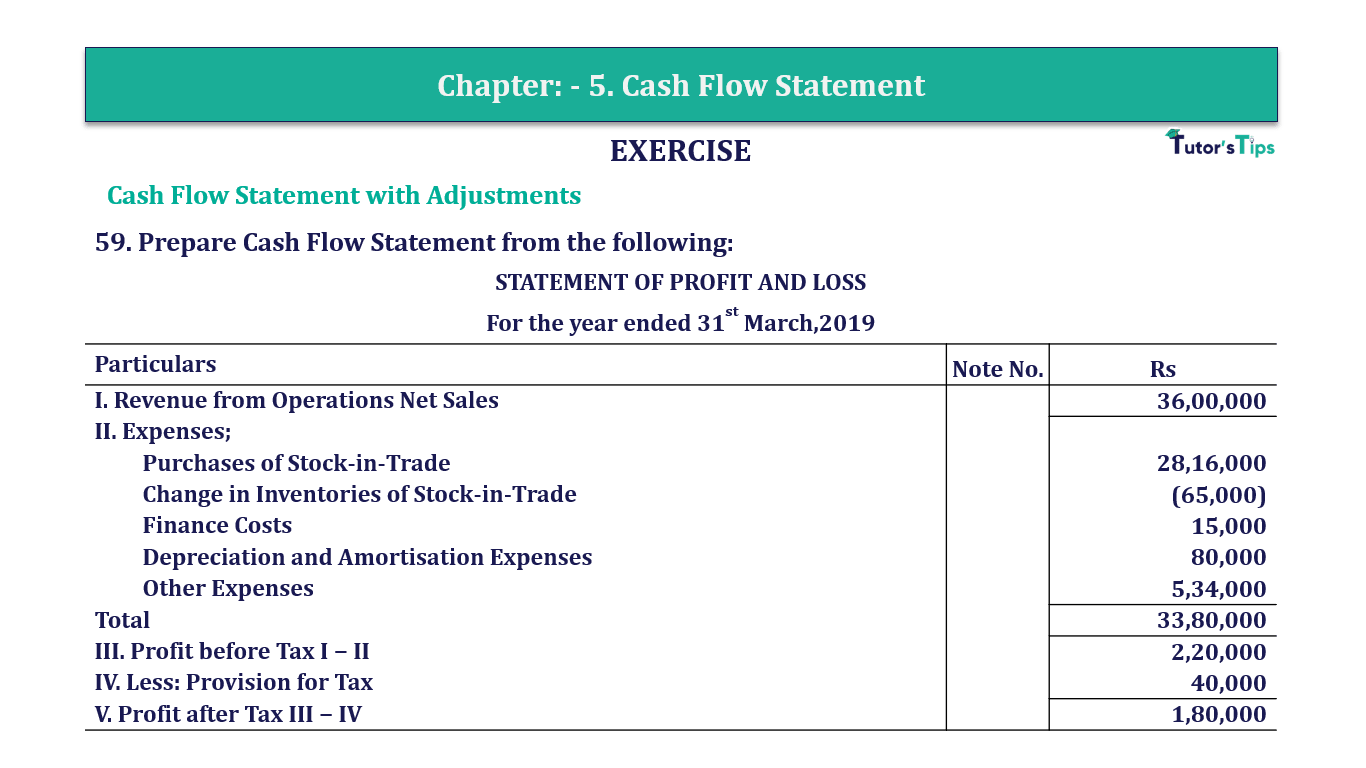

STATEMENT OF PROFIT AND LOSS For the year ended 31st March,2019

| Particulars | Note No. | 31st March, | 31st March, |

| 2019 Rs | 2018 Rs | ||

| I. Revenue from Operations Net Sales | 4 | 40,00,000 | 35,00,000 |

| II. Other Income | 5 | 35,000 | 30,000 |

| III. Total Revenue I + II | 40,35,000 | 35,30,000 | |

| IV. Expenses; | |||

| Purchases of Stock-in-Trade | 27,00,000 | 24,70,000 | |

| Change in Inventories of Stock-in-Trade | 6 | 1,00,000 | 50,000 |

| Finance Costs | 27,500 | 20,000 | |

| Depreciation | 40,000 | 45,000 | |

| Other Expenses | 22,500 | 20,000 | |

| Total | 28,90,000 | 26,05,000 | |

| III. Profit before Tax III− IV | 11,45,000 | 9,25,000 | |

| VI. Less: Tax | 3,45,000 | 2,25,000 | |

| V. Profit after Tax (V − VI) | 8,00,000 | 7,00,000 |

Notes to Accounts

| Particulars | 31st March, 2019 Rs | 31st March,2018 Rs |

| 1. Reserves and Surplus | ||

| Debenture Redemption Reserve | 1,00,000 | 1,00,000 |

| Surplus, i.e., Balance in Statement of Profit and Loss | 8,50,000 | 2,00,000 |

| 9,50,000 | 3,00,000 | |

| 2. Other Current Liabilities | ||

| Interest on Debentures | 35,000 | 20,000 |

| Outstanding Expenses | 4,000 | 5,000 |

| 39,000 | 25,000 | |

| 3. Fixed Assets–Tangible | ||

| Cost | 8,90,000 | 9,90,000 |

| Less: Accumulated Depreciation | 2,05,000 | 2,45,000 |

| 6,85,000 | 7,45,000 | |

| 4. Revenue from Operations | ||

| Sales | 42,00,000 | 35,75,000 |

| Less: Sales Return | 2,00,000 | 75,000 |

| 40,00,000 | 35,00,000 | |

| 5. Other Income | ||

| Interest on Deposits | 15,000 | 12,500 |

| Dividend on Investments | 10,000 | 17,500 |

| Gain Profit on Sale of Fixed Assets | 10,000 | ---- |

| 35,000 | 30,000 | |

| Particulars | 31st March, | 31st March, |

| 2019 Rs | 2018 Rs | |

| 6. Change in Inventories of Stock-in-Trade | ||

| Opening Stock | 2,00,000 | 2,50,000 |

| Less: Closing Stock | 1,00,000 | 2,00,000 |

| 1,00,000 | 50,000 |

Cash Flow Statement for the year ended 31st March,2019

| Particulars |

Rs |

|

|---|---|---|

| I. Cash Flow from Financing Activities | ||

| Profit as per Statement of Profit and Loss : | 8,00,000 | |

| Provision for Tax | 3,45,000 | 11,45,000 |

| Net Profit before tax and extraordinary items | 11,45,000 | |

| Items to be Added: | ||

| Finance Cost | 27,500 | |

| Depreciation and Amortisation Expenses | 40,000 | 95,000 |

| Items to be Deducted: | ||

| Interest on Deposits | 15,000 | |

| Dividend received on Investments | 10,000 | |

| Gain on sale of fixed asset | 10,000 | 35,000 |

| Net Profit before working capital changes | 11,77,500 | |

| Add : Increase in Current Liabilities | ||

| Trade Payables | 20,000 | |

| Add : Decrease in Current Assets | ||

| Inventories | 1,00,000 | |

| Less: Decrease in Current Liabilities | ||

| Outstanding expenses | 1,000 | |

| Add: Increase in Current Liabilities | ||

| Trade Receivable | 2,50,000 | 10,46,500 |

| Cash Generated from Operations | 10,46,500 | |

| Less: Tax Paid (WN 3) | 3,10,000 | |

| Net Cash Flow from Operating Activities | 7,36,500 | |

| II. Cash Flow from Financing Activities | ||

| Sale of Fixed Asset (WN 1(b)) | 30,000 | |

| Purchase of Investments | 5,00,000 | |

| Dividend received on Investments | 10,000 | |

| Interest Received on deposits | 15,000 | |

| Net Cash Used in Investing Activities | 4,45,000 | |

| III: Cash Flow from Financing Activities | ||

| Proceeds from Issue of shares | 2,50,000 | |

| Proceeds from Issue of debentures | 5,00,000 | |

| Redemption of debentures (WN 2) | 2,00,000 | |

| Finance Cost paid | 12,500 | |

| Interim Dividend paid | 1,00,000 | |

| Proposed Dividend Paid | 50,000 | 3,87,500 |

| Net Cash Flow from Financing Activities | 3,87,500 | |

| IV. Net Decrease in Cash and Cash Equivalents |

6,79,000 | |

| Add: Cash and Cash Equivalents in the beginning of the period |

1,95,000 |

|

| Cash and Cash Equivalents at the end of the period |

8,74,000 | |

Accumulated Depreciation Account

| Particulars |

Rs | Particular | Rs |

|---|---|---|---|

| To Fixed Asset A/c (On Sale of machinery) |

80,000 | By Balance b/d | 2,45,000 |

| To Balance c/d | 2,05,000 | By Profit and Loss A/c | 40,000 |

| 2,85,000 | 2,85,000 |

Accumulated Depreciation Account

| Particulars |

Rs | Particular | Rs |

|---|---|---|---|

| To Balance b/d | 9,90,000 | By Accumulated Depreciation A/c | 80,000 |

| To Statement of Profit & Loss A/c | 10,000 | By Bank A/c (Sale of Machine) (Bal. Fig.) | 30,000 |

| By Balance c/d | 8,90,000 | ||

| 10,00,000 | 10,00,000 |

5% Debentures Account

| Particulars |

Rs | Particular | Rs |

|---|---|---|---|

| To Bank A/c (Redemption Bal. Fig.) | 2,00,000 | By Balance b/d | 2,45,000 |

| To Balance c/d | 2,05,000 | By Bank A/c (Issue of Debentures) | 40,000 |

| 2,85,000 | 2,85,000 |

Provision for Tax Account

| Particulars |

Rs | Particular | Rs |

|---|---|---|---|

| To Bank A/c- Tax Paid | 3,10,000 | By Balance b/d | 2,25,000 |

| To Balance c/d | 2,60,000 | By Profit and Loss A/c | 3,45,000 |

| 5,70,000 | 5,70,000 |

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of previous Chapters: -

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 60 Chapter 5 of +2-B - T.S. Grewal 12 Class", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - B - T.S. Grewal - XII.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 60 Chapter 5 of +2-B - T.S. Grewal 12 Class" instantly.