Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Question 6 Chapter 5 - Unimax

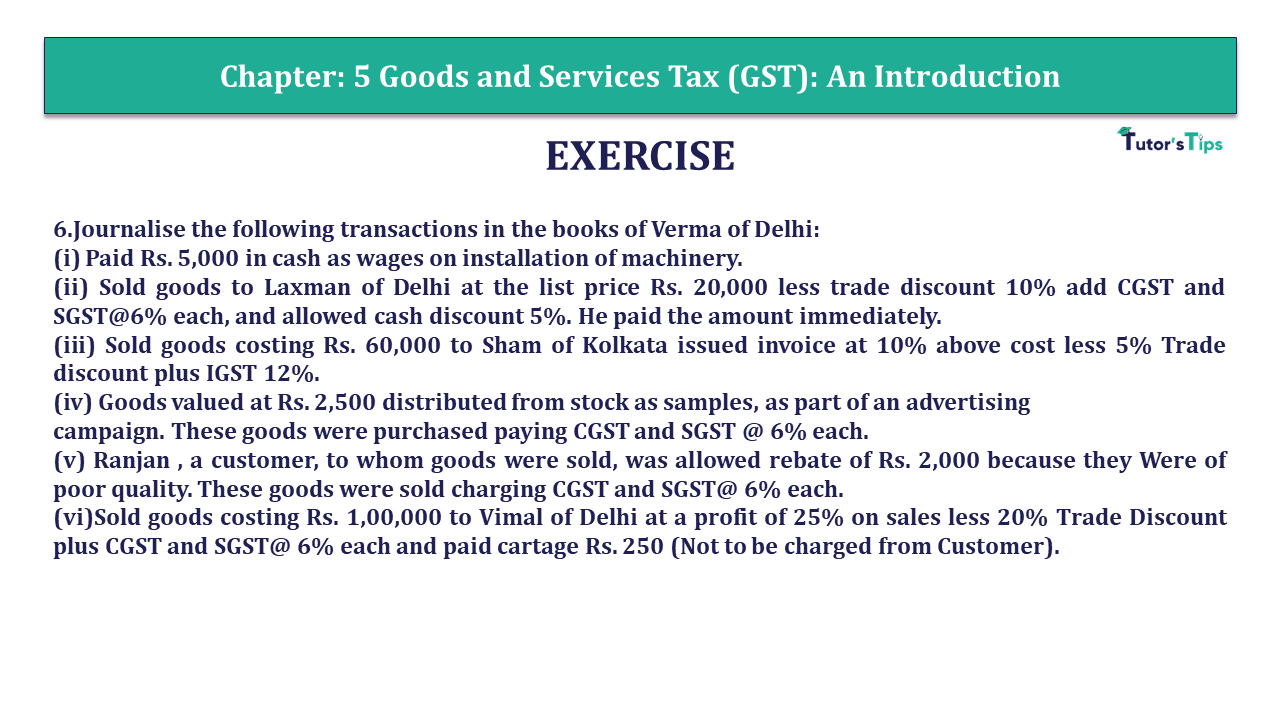

6.Journalise the following transactions in the books of Verma of Delhi:

(i) Paid Rs. 5,000 in cash as wages on installation of machinery.

(ii) Sold goods to Laxman of Delhi at the list price Rs. 20,000 less trade discount 10% add CGST and SGST@6% each, and allowed cash discount 5%. He paid the amount immediately.

(iii) Sold goods costing Rs. 60,000 to Sham of Kolkata issued invoice at 10% above cost less 5% Trade discount plus IGST 12%.

(iv) Goods valued at Rs. 2,500 distributed from stock as samples, as part of an advertising

campaign. These goods were purchased paying CGST and SGST @ 6% each.

(v) Ranjan , a customer, to whom goods were sold, was allowed rebate of Rs. 2,000 because they Were of poor quality. These goods were sold charging CGST and SGST@ 6% each.

(vi)Sold goods costing Rs. 1,00,000 to Vimal of Delhi at a profit of 25% on sales less 20% Trade Discount plus CGST and SGST@ 6% each and paid cartage Rs. 250 (Not to be charged from Customer).

JOURNAL OF VERMA

| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| (i) | Machinery A/c * | Dr. | 5,000 | ||

| To Cash A/c | 5,000 | ||||

| (Being the wages paid on installation of a machinery) | |||||

| (ii) | Cash A/c (WN 1) | Dr. | 19,152 | ||

| Discount Allowed A/c | Dr. | 1,008 | |||

| To Sales A/c | 18,000 | ||||

| To Output CGST A/c | 1,080 | ||||

| To Output SGST A/c | 1,080 | ||||

| (Being the goods worth 20,000 sold, charged CGST and SGST 6% each, allowed 10% trade discount and 5% Cash discount) | |||||

| (iii) | Sham A/c | Dr. | 70,224 | ||

| To Sales A/c | 62,700 | ||||

| To Output IGST A/c | 7,524 | ||||

| (Being the goods supplied of 66,000 (i.e., 60,000+ 10% Of 60,000 plus IGST 12%) allowed 5% trade discount (i.e., 66,000- 3,300)) | |||||

| (iv) | Advertisement A/c | Dr. | 2,800 | ||

| To Purchases A/c | 2,500 | ||||

| To Input CGST A/c | 150 | ||||

| To Input SGST A/c | 150 | ||||

| (Being the goods distributed as free samples, Input CGST and Input SGST reversed) | |||||

| (v) | Rebate A/c | Dr. | 2,000 | ||

| Output CGST A/c | Dr. | 120 | |||

| Output SGST A/c | Dr. | 120 | |||

| To Ranjan A/c | 2,240 | ||||

| (Being the rebate allowed, Output CGST and SGST Reversed) | |||||

| (vi) | Vimal A/c | Dr. | 1,12,000 | ||

| To Sales A/c | 1,00,000 | ||||

| To Output CGST A/c | 6,000 | ||||

| To Output SGST A/c | 6,000 | ||||

| (Being the goods sold on credit, charging CGST and SGST 6% each) | |||||

| Cartage Outwards A/c | Dr. | 250 | |||

| To Cash A/c | 250 | ||||

| (Being the cartage paid) | |||||

Note: Installation charge is a capital expenditure, thus, is debited to the Machinery Account not paid, it being wages paid, which is not subject to levy of GST.

Working Notes :

1. Sale of Goods to Laxman, Delhi :

| Trade discount is not shown separately in the books of account. | ₹ |

| List Price | 20,000 |

| Less : Trade Discount @ 10% | 2,000 |

| 18,000 | |

| Add: CGST @ 6% | 1,080 |

| SGST @ 6% | 1,080 |

| 20,160 | |

| Less : Cash Discount @ 5% | 1,008 |

| Net Amount | 19,152 |

2. Calculation of Sales Price for Transaction (vi)

| ₹ | |

| Cost of Goods Sold | 1,00,000 |

| Add: Profit (25%) | 25,000 |

| 1,25,000 | |

| Less: Trade Discount (20%) | 25,000 |

| Sale Value | 1,00,000 |

This is all about the Question 6 Chapter 5 - Unimax. You can check out the following article to better understand:

Opening Journal Entry – its Rules and Examples

You Can also read all above articles in Hindi on our Hindi Website

Opening Journal Entry – its Rules and Examples - In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in the Question 6 Chapter 5 - Unimax.

You can also Check out the solved question of other Chapters: -

Part-I

Students may Choose only one part from the Part II and Part III

Part-II

Part-III

You can also Check out the other Books' Solution: -

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 6 Chapter 5 - Unimax Publications of Class 11", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax class 11 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 6 Chapter 5 - Unimax Publications of Class 11" instantly.