Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

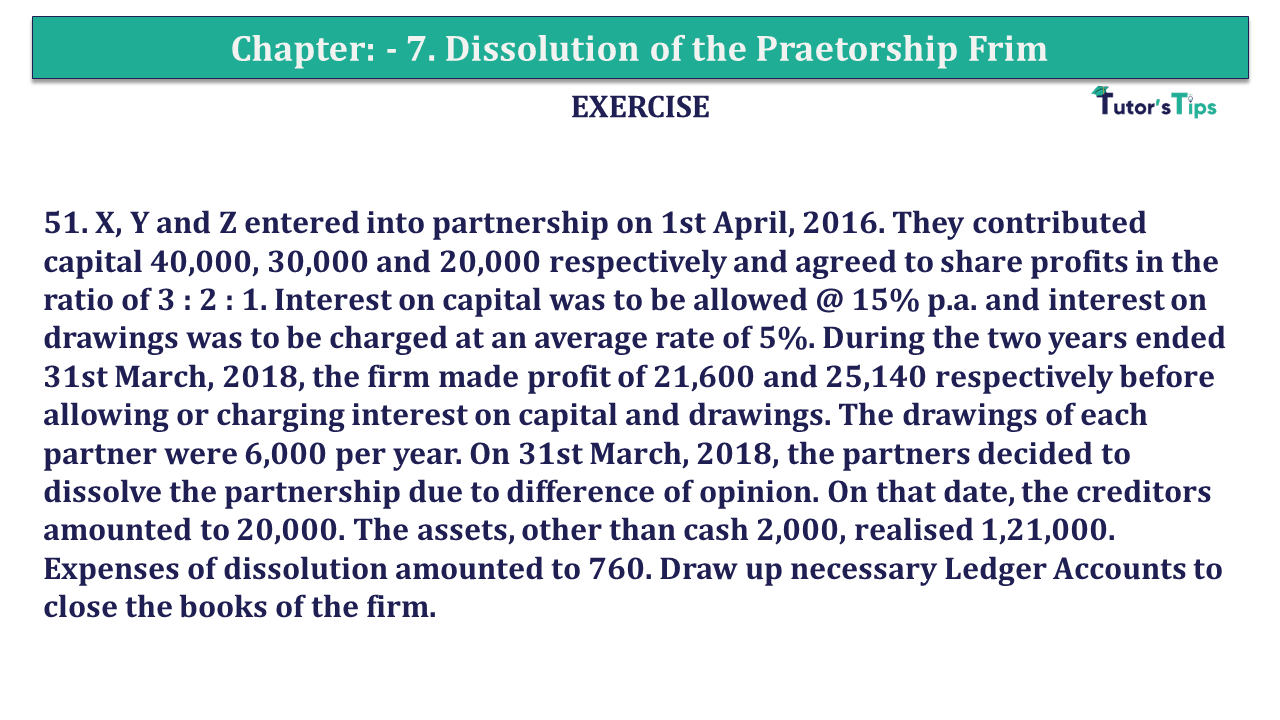

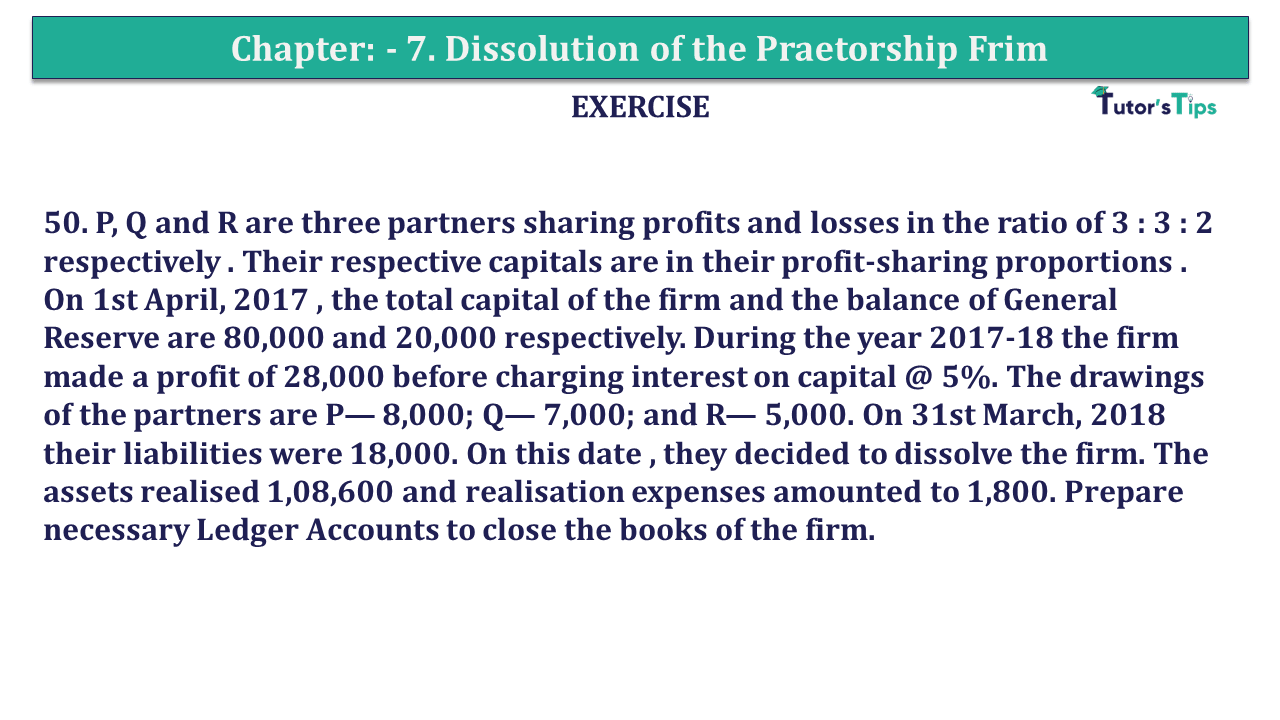

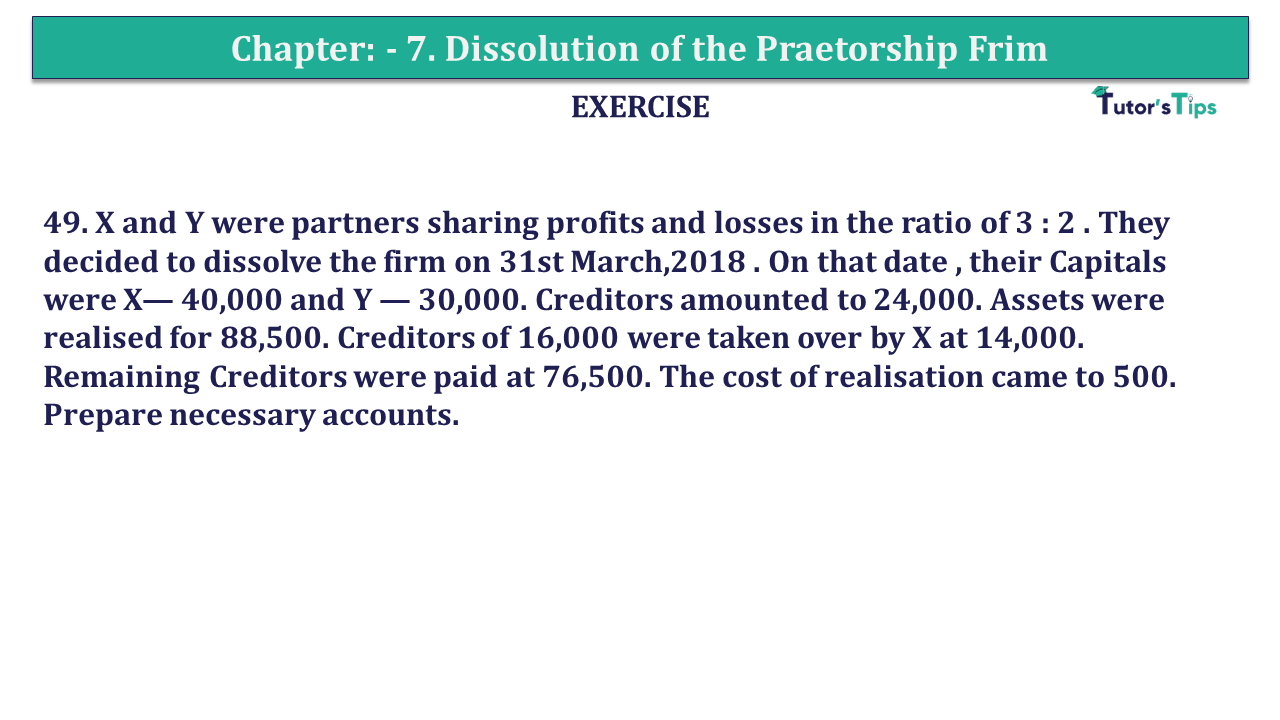

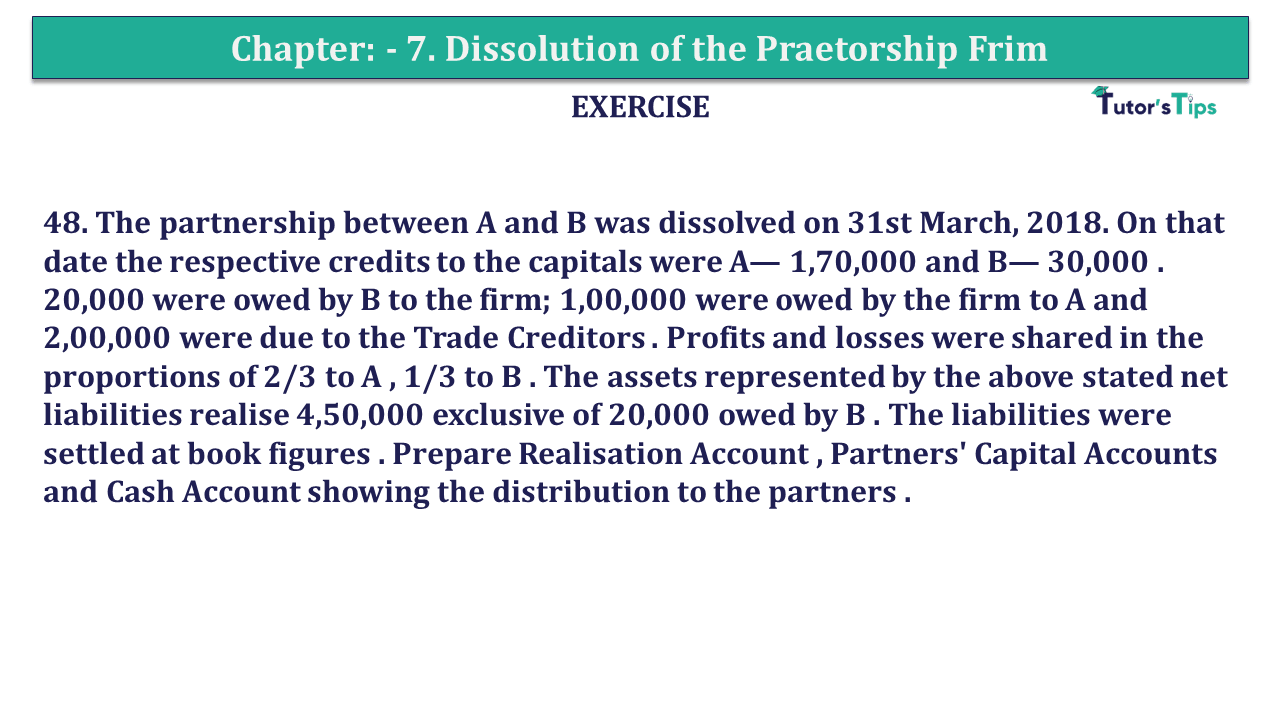

Question 48 Chapter 7 of +2-A

48. The partnership between A and B was dissolved on 31st March, 2018. On that date, the respective credits to the capitals were A— 1,70,000 and B— 30,000. 20,000 were owed by B to the firm; 1,00,000 were owed by the firm to A and 2,00,000 were due to the Trade Creditors. Profits and losses were shared in the proportions of 2/3 to A, 1/3 to B. The assets represented by the above stated net liabilities realise 4,50,000 exclusive of 20,000 owed by B. The liabilities were settled at book figures. Prepare Realisation Account, Partners' Capital Accounts and Cash Account showing the distribution to the partners.

Revaluation Account

| Particular 5 |

Amount | Particular | Amount | ||

|---|---|---|---|---|---|

| Sundry Assets (WN) | 4,80,000 | Trade Creditors | 2,00,000 | ||

| B’s Loan | 20,000 | Cash Assets realized | 4,50,000 | ||

| Cash A/c Creditors | 2,00,000 | B’s Capital A/c B’s Loan | 20,000 | ||

| Loss transferred to: | |||||

| A’s Capital A/c | 20,000 | ||||

| B’s Capital A/c | 10,000 | 30,000 | |||

| 7,00,000 | 7,00,000 | ||||

Partners’ Capital Account

| Part. | A | B |

Part. |

A | B |

|---|---|---|---|---|---|

| To Realization A/c | - | 20,000 | By Balance B/d | 1,70,000 | 30,000 |

| To Realization Loss A/c | 20,000 | 20,000 | |||

| To Cash A/c | 1,50,000 | - | |||

| 1,70,000 | 30,000 | 1,70,000 | 30,000 |

Cash Account

| Particular |

Amount | Particular | Amount | ||

|---|---|---|---|---|---|

| Realization A/c Asset | 4,50,000 | Realization A/c Creditors | 2,00,000 | ||

| A’s Capital A/c | 1,50,000 | ||||

| A’s Loan A/c | 1,00,000 | ||||

| 4,50,000 | 4,50,000 | ||||

Working Note:

Memorandum Balance Sheet

| Particular |

Amount | Particular | Amount | ||

|---|---|---|---|---|---|

| Sundry Assets (Balancing figure) | 20,000 | ||||

| Capital A/cs | Sundry Assets (Balancing figure) | 4,80,000 | |||

| A’s Capital A/c | 1,70,000 | ||||

| B’s Capital A/c | 30,000 | 2,00,000 | |||

| A’s Loan | 1,00,000 | ||||

| Trade Creditors | 2,00,000 | ||||

| 5,00,000 | 5,00,000 | ||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Q.No.48 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.48 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.