Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

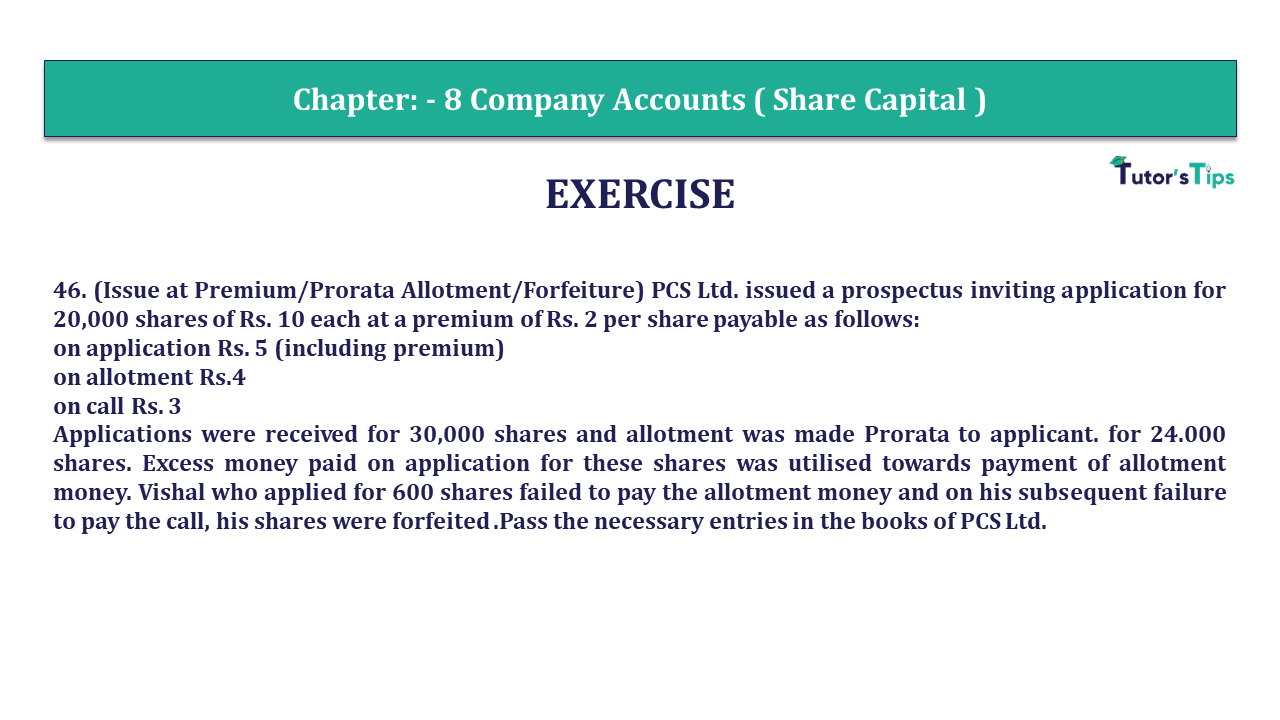

Question 46 Chapter 8 of +2-Part-1 - USHA

46. (Issue at Premium/Prorata Allotment/Forfeiture) PCS Ltd. issued a prospectus inviting application for 20,000 shares of Rs. 10 each at a premium of Rs. 2 per share payable as follows:

on application Rs. 5 (including premium)

on allotment Rs.4

on call Rs. 3

Applications were received for 30,000 shares and allotment was made Prorata to applicant. for 24.000 shares. Excess money paid on application for these shares was utilised towards payment of allotment money. Vishal who applied for 600 shares failed to pay the allotment money and on his subsequent failure to pay the call, his shares were forfeited .Pass the necessary entries in the books of PCS Ltd.

Journal

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| A) | Bank A/c | Dr. | 1,50,000 | ||

| To Share Application A/c | 1,50,000 | ||||

| (Being the receipt of application money) | |||||

| B) | Share Application A/c | Dr. | 1,50,000 | ||

| To Share capital A/c | 60,000 | ||||

| To Security Premium Reserve A/c | 40,000 | ||||

| To Share allotment A/c | 20,000 | ||||

| To Bank A/c | 30,000 | ||||

| (Being 20,000 shares allotted ) | |||||

| C) | Share allotment A/c | Dr. | 80,000 | ||

| To Share capital A/c | 80,000 | ||||

| (Being amount due on allotment) | |||||

| D) | Bank A/c | Dr. | 58,500 | ||

| Calls in arrears A/c | Dr. | 1,500 | |||

| To Share allotment A/c | 60,000 | ||||

| (Being amount received on allotment) | |||||

| E) | Share Call A/c | Dr. | 60,000 | ||

| To Share capital A/c | 60,000 | ||||

| (Being amount due on first call) | |||||

| F) | Bank A/c | Dr. | 58,500 | ||

| Calls in arrears A/c | Dr. | 1,500 | |||

| To Share allotment A/c | 60,000 | ||||

| (Being amount received on call) | |||||

| Shares applied = 24,000/20,000 X 600 = 720 shares | ||

| Excess app. money retained for allotment | ||

| (720 X 5) – (600X5) = Rs. 600 | ||

| Allotment not received on 600 shares | ||

| 600 X 4 | 2,400 | |

| Less : Retained | 600 | |

| Not received | 1,800 | |

| Allotment received: | ||

| Total amount due | 80,000 | |

| Less : Already received | 20,000 | |

| Less : not received | 1,800 | 21,800 |

| 58,200 | ||

| Amount credited to share forfeited A/c | ||

| Received on application : 720 X 5 | 3,600 | |

| Less : Adjustment on premium :600 X 2 | 1,200 | |

| 2,400 |

Note: Premium received Rs. 1,200 can’t be forfeited

This is all about the Question 46 Chapter 8 of +2-Part-1 - USHA

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 46 Chapter 8 of +2-Part-1 - USHA Publication 12 Class Part - 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to USHA Publication +2 Part 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 46 Chapter 8 of +2-Part-1 - USHA Publication 12 Class Part - 1" instantly.