Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1 | Tutorstips

Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1

By Sarbjit Singh (B.Com and M.Com)|Published: 29 November 2020|Last Updated: 23 June 2026|T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1Chapter No. 7 - Dissolution of a Partnership Firm

Focus Topic:Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1

Estimated Reading Time:3 mins

Comprehensive academic guide covering core concepts of Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

Syllabus-aligned study material with detailed definitions, formats, and practical examples.

Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

Question 45 Chapter 7 of +2-A

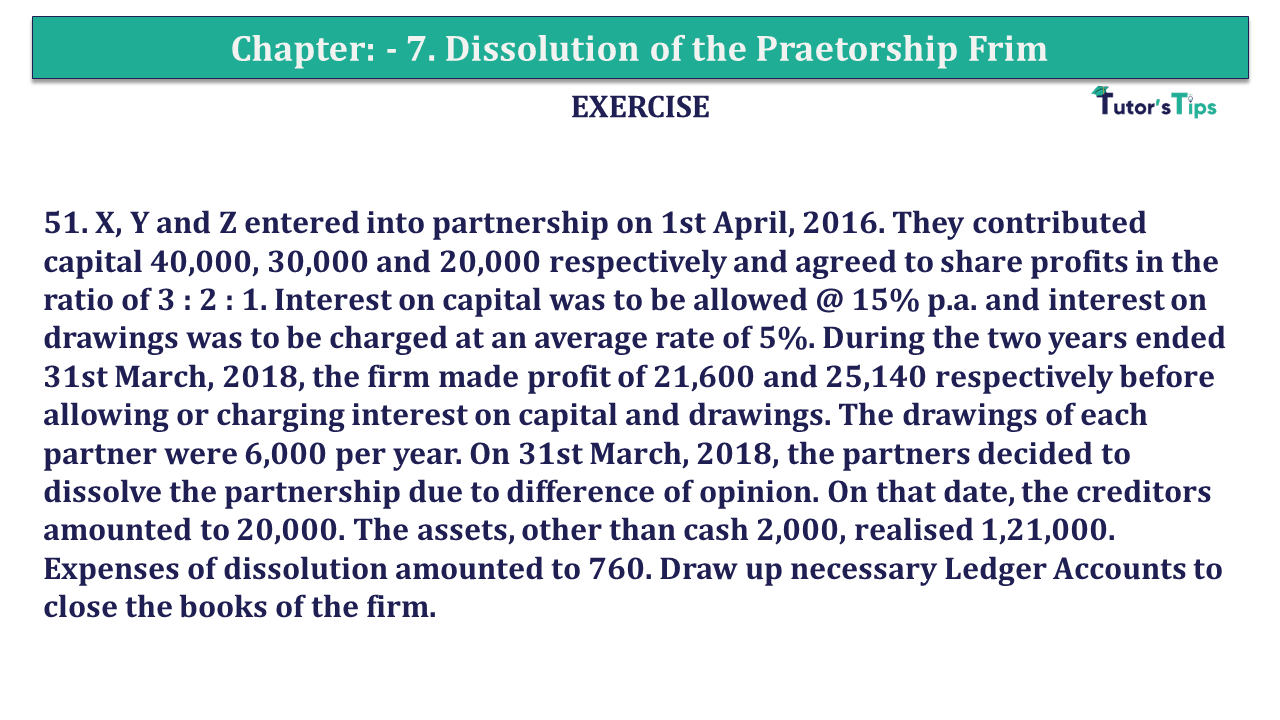

45. A, B and C started business on 1st April, 2016 with capitals of 1,00,000; 80,000 and 60,000 respectively sharing profits losses in the ratio of 4 : 3 : 3 . For the year ended 31st March, 2017, the firm suffered a loss of 50,000 . Each of the partners withdrew 10,000 during the year. On 31st March, 2017, the firm was dissolved, the creditors of the firm stood at 24,000 on that date and Cash in Hand was 4,000. The assets realised 3,00,000 and Creditors were paid 23,500 in full settlement of their claims . Prepare Realisation Account and show your workings clearly.

The solution of Question 45 Chapter 7 of +2-A: -

Realization Account

Particular 5

Amount

Particular

Amount

Sundry Assets (WN 2)

1,80,000

Sundry Creditors

24,000

Cash A/c Creditors

23,500

Cash A/c Assets

3,00,000

Profit transferred to:

A’s Capital A/c

48,200

B’s Capital A/c

36,150

C’s Capital A/c

36,150

1,20,500

3,20,000

3,20,000

Partners’ Capital Account

Part.

A

B

C

Part.

A

B

C

By Balance B/d

70,000

55,000

35,000

By Realization Profit A/c

48,200

36,150

36,150

To Cash A/c

1,18,200

91,150

71,150

1,18,200

91,150

71,150

1,18,200

91,150

71,150

Cash Account

Particular

Amount

Particular

Amount

Realization A/c

4,000

Realization A/c

23,500

Realization A/c

3,00,000

A’s Capital A/c

1,18,200

B’s Capital A/c

91,150

C’s Capital A/c

71,150

3,04,000

3,04,000

Working Note:

Memorandum Balance Sheet

Particular

A

B

C

Capital as on April 01, 2016

1,00,000

80,000

60,000

Less : Drawings

10,000

10,000

10,000

Less: Share of Loss 4 : 3 : 3

20,000

15,000

15,000

Capital as on April 01, 2017

70,000

55,000

35,000

Memorandum Balance Sheet

Particular

Amount

Particular

Amount

Creditors

24,000

Cash in Hand

4,000

Capital A/cs

Sundry Assets (Balancing figure)

1,80,000

A’s Capital A/c

70,000

B’s Capital A/c

55,000

C's Capital A/c

35,000

1,60,000

1,84,000

1,84,000

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms

👤

Author & Educator

Sarbjit SinghB.Com and M.Com

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

❓ Frequently Asked Questions

What is the main topic of "Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1"?

This guide covers "Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

Who can benefit from this guide on "Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1"?

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

Where can I practice questions related to "Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1"?

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.45 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.