Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Question 45 Chapter 1 of +2-A

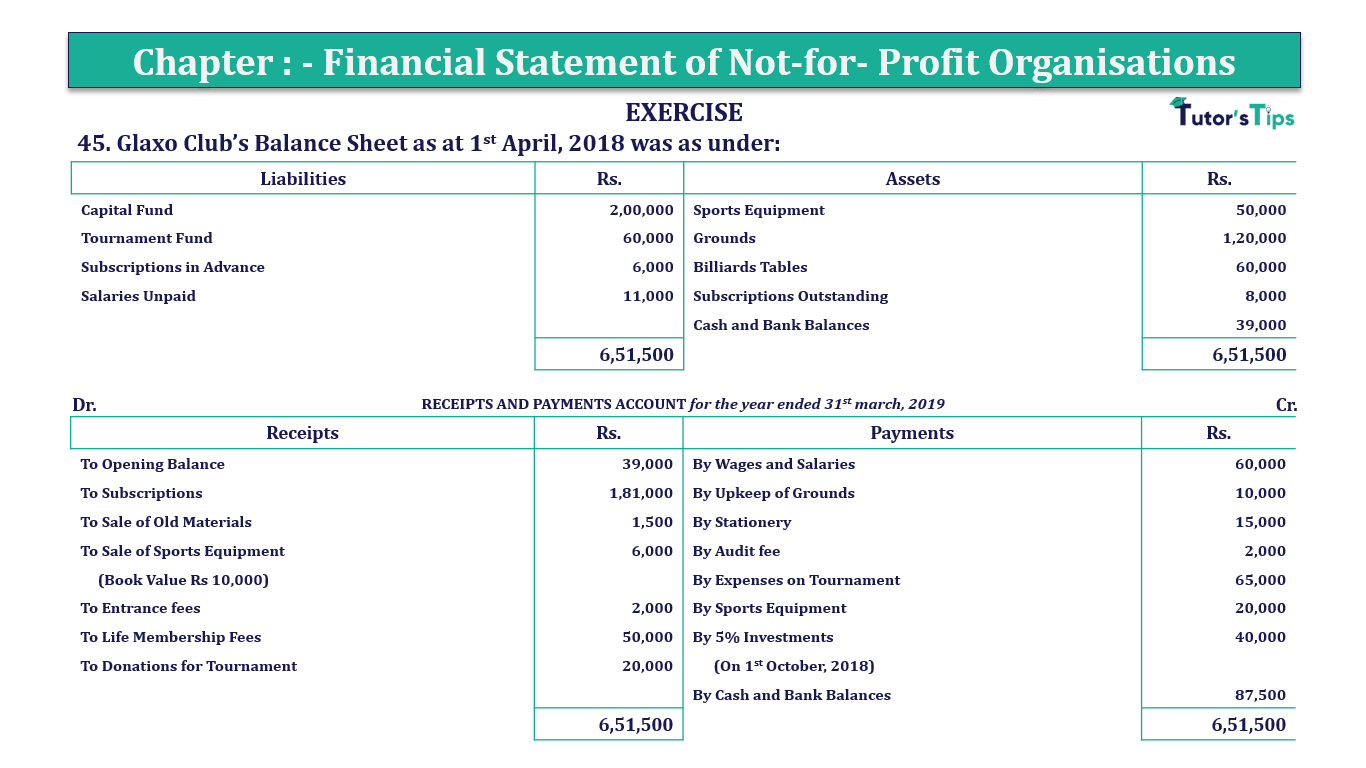

45. Glaxo Club’s Balance Sheet as at 1st April 2018 was as under:

| Liabilities | Rs. | Assets | Rs. |

| Capital Fund | 2,00,000 | Sports Equipment | 50,000 |

| Tournament Fund | 60,000 | Grounds | 1,20,000 |

| Subscriptions in Advance | 6,000 | Billiards Tables | 60,000 |

| Salaries Unpaid | 11,000 | Subscriptions Outstanding | 8,000 |

| Cash and Bank Balances | 39,000 | ||

| 6,51,500 | 6,51,500 |

RECEIPTS AND PAYMENTS ACCOUNT for the year ended 31st March 2019

| Receipts | Rs. | Payments | Rs. |

| To Opening Balance | 39,000 | By Wages and Salaries | 60,000 |

| To Subscriptions | 1,81,000 | By Upkeep of Grounds | 10,000 |

| To Sale of Old Materials | 1,500 | By Stationery | 15,000 |

| To Sale of Sports Equipment | 6,000 | By Audit fee | 2,000 |

| (Book Value Rs 10,000) | By Expenses on Tournament | 65,000 | |

| To Entrance fees | 2,000 | By Sports Equipment | 20,000 |

| To Life Membership Fees | 50,000 | By 5% Investments | 40,000 |

| To Donations for Tournament | 20,000 | (On 1st October 2018) | |

| By Cash and Bank Balances | 87,500 | ||

| 6,51,500 | 6,51,500 |

Additional Information:

Subscriptions still to be received are Rs 5,500 but subscriptions already received include Rs 4,000 for next year. Salaries still unpaid are Rs 6,000. Sports Equipment is now valued at Rs 45,000. Prepare Income and Expenditure Account and the Balance sheet, after charging 10% depreciation on Billiards Tables.

Income and Expenditure Account (for the year ended 31st March 2019)

| Expenditure |

Amount | Income |

Amount | ||

|---|---|---|---|---|---|

| To Wages and Salaries | 60,000 | By Subscription 2018-19* | 1,81,000 | ||

| Add: - Closing Unpaid Salaries | 6,000 | Add O/s Sub. at the end | 5,500 | ||

| Less: - Opening Unpaid Salaries | 11,000 | 55,000 | Adv. Sub. In the Beginning | 6,000 | |

| To Upkeep of Grounds | 10,000 | Less: O/s. Sub. In the Beginning | 8,000 | ||

| To Stationery | 15,000 | Adv. Sub. at the end | 4,000 | 1,80,500 | |

| To Audit fee | 2,000 | By Sale of Old Materials | 1,500 | ||

| To Loss on sale of Sports Equipment* | 4,000 | By Entrance Fees | 2,000 | ||

| To Consumption of Sport Equipment* | 15,000 | By Accrued Interest on investment* | 1,000 | ||

| To Depreciation on Billiards Tables* | 6,000 | ||||

| To Surplus(Balancing Figure) | 33,000 | ||||

| 1,85,000 | 1,85,000 | ||||

Balance Sheet (for the year ended 31st March 2018)

| Liabilities |

Amount | Assets | Amount | ||

|---|---|---|---|---|---|

| Capital Fund | 2,00,000 | Cash in Hand | 87,500 | ||

| Add: - Surplus | 33,000 | 2,33,000 | Cash at Bank | ||

| Outstanding Salaries | 6,000 | Grounds | 1,20,000 | ||

| Advance Subscription for 19-20 | 4,000 | Billiards Tables | 60,000 | ||

| Tournament Fund* | 15,000 | Less: Depreciation | 6,000 | 54,000 | |

| Life Membership Fees | 50,000 | Outstanding Subscription | 5,500 | ||

| 5% of Investments | 40,000 | ||||

| Accrued Interest | 1,000 | ||||

| 3,08,000 | 3,08,000 | ||||

Working Note: -

Calculation of Amount of Subscriptions

| Subscription received During the year | 1,81,000 |

| Add: - Subscription outstanding at the end of the year | 5,500 |

| Subscription received in advance at the beginning of the year | 6,000 |

| 1,92,500 | |

| Less: - Subscription outstanding at the beginning of the year | 8,000 |

| Subscription received in advance at the end of the year | 4,000 |

| The amount for subscription credited to the Income and Expenditure A/c | 1,80,500 |

Calculation of Total Interest on Investment

Interest on Investment = Value of Investment X Rate of Interest X Period

Value of Asset = 40,000

Rate of Interest = 10%

Period = from 01/10/18 to 31/03/19 i.e. 6 months

(from the date of purchase to the end of the financial year)

= 40,000 X 10/100 X 6/12

Total Interest on Investment = 1,000/-

| Calculation of the Accrued amount of Interest on Investment | |

| Total Amount of Interest on Investment For the F/Y 19-20 | 1,000 |

| Less: - Total Amount Interest on Investment received For the F/Y 19-20 | 0 |

| Accrued amount of Interest on Investment For the F/Y 19-20 | 1,000 |

| Calculation of the amount of Profit/loss on the sale of Sports Equipment | |

| Sale Value of Sports Equipment | 6,000 |

| Less: - Book Value of Sports Equipment | 10,000 |

| Loss on sale of Sports Equipment | - 4,000 |

| Calculation of the amount of consumption of Sports Equipment | |

| Opening Balance of Sports Equipment | 50,000 |

| Add: - Purchase of Sports Equipment during the year | 20,000 |

| Less: - Book Value of Sports Equipment | 10,000 |

| 60,000 | |

| Less: - Closing Value of Sports Equipment | 45,000 |

| Loss on sale of Sports Equipment | 15,000 |

Calculate Depreciation on Billiards Table

Depreciation = Value of Asset X Rate of Depreciation X Period

Value of Asset = 60,000

Rate of Depreciation = 10%

Period = from 01/04/18 to 31/03/19 i.e. 12 months

(from the date of purchase/Beginning balance to the end of the financial year)

= 60,000 X 10/100 X 12/12

Depreciation = 6,000/-

| Calculate Tournament Fund | |

| Opening Tournament Fund | 60,000 |

| Add: - Received Donation for tournament | 20,000 |

| Less: - Tournament Expenses | 65,000 |

| Closing Tournament Fund | 15,000 |

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: -

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Q.No.45 | Chapter 1 – Financial Statements of Not-for-Profit Organisations | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.45 | Chapter 1 – Financial Statements of Not-for-Profit Organisations | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.