Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

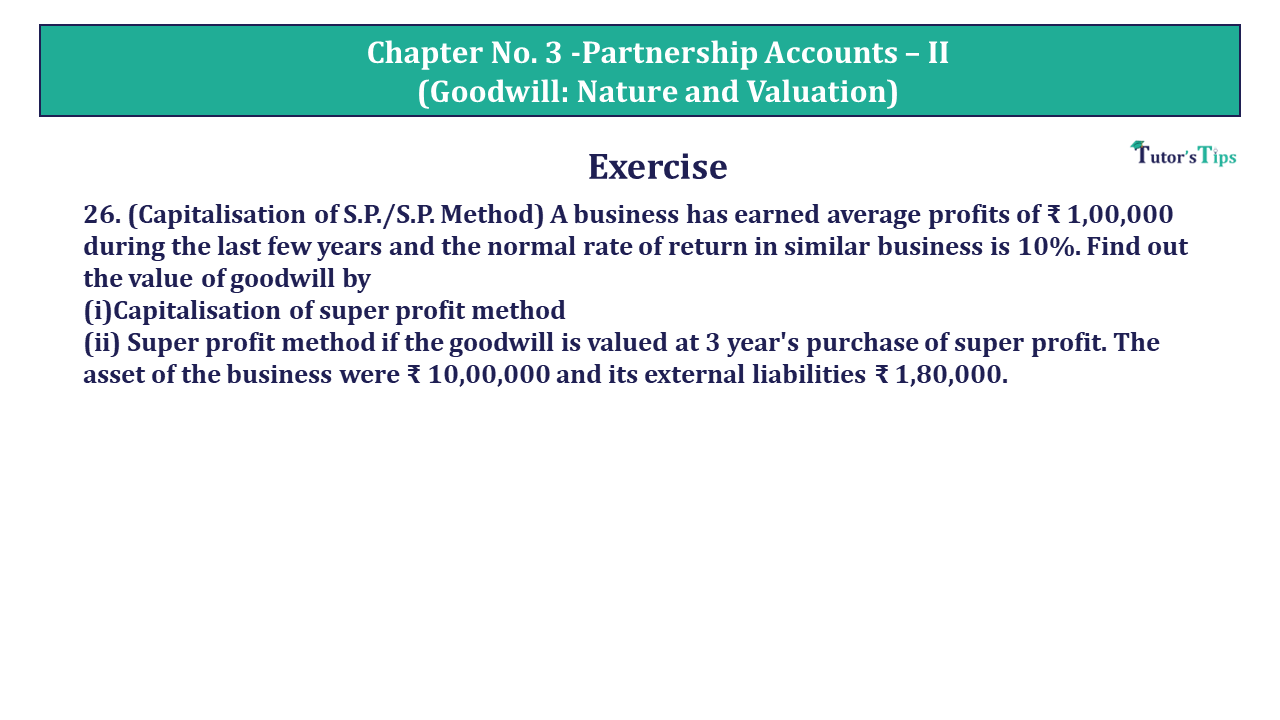

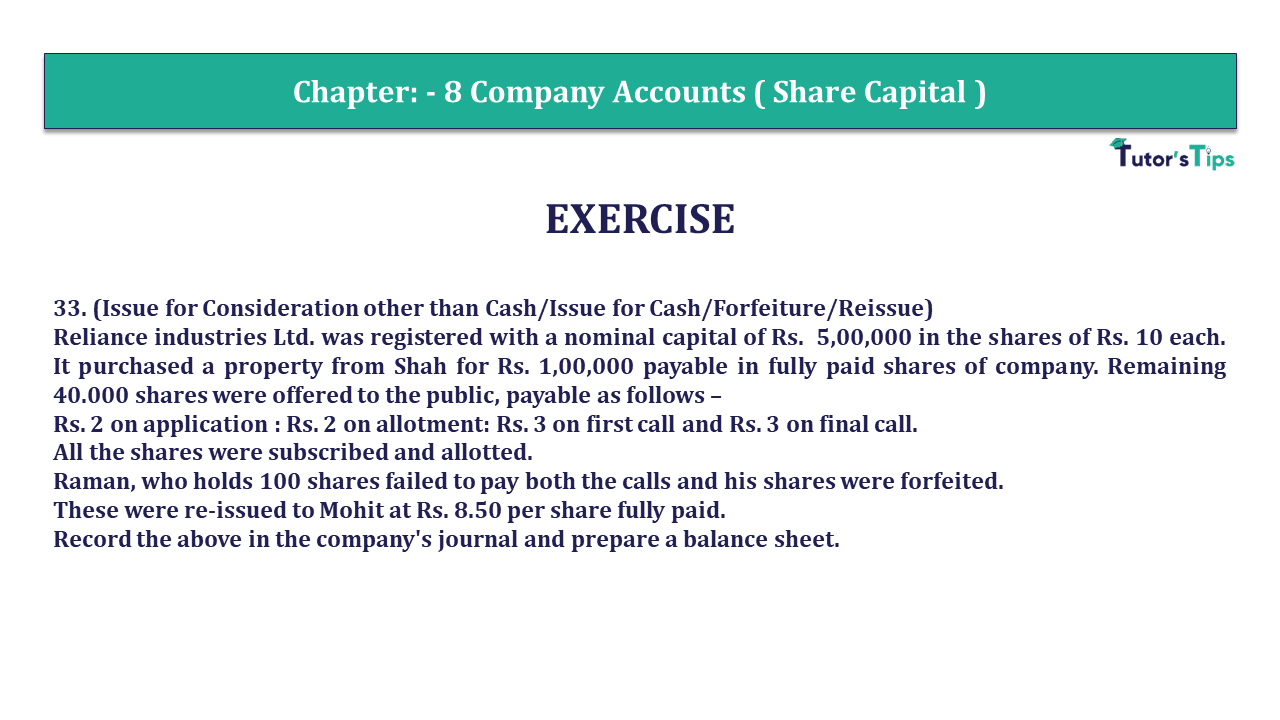

Question 33 Chapter 8 of +2-Part-1

33. (Issue for Consideration other than Cash/Issue for Cash/Forfeiture/Reissue)

Reliance industries Ltd. was registered with a nominal capital of Rs. 5,00,000 in the shares of Rs. 10 each. It purchased a property from Shah for Rs. 1,00,000 payable in fully paid shares of company. Remaining 40.000 shares were offered to the public, payable as follows –

Rs. 2 on application : Rs. 2 on allotment: Rs. 3 on first call and Rs. 3 on final call.

All the shares were subscribed and allotted.

Raman, who holds 100 shares failed to pay both the calls and his shares were forfeited.

These were re-issued to Mohit at Rs. 8.50 per share fully paid.

Record the above in the company's journal and prepare a balance sheet.

Journal

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| A) | Property A/c | Dr. | 1,00,000 | ||

| To Shah A/c | 1,00,000 | ||||

| (Being property purchased by shah ) | |||||

| B) | Shah A/c | Dr. | 1,00,000 | ||

| To Share capital A/c | 1,00,000 | ||||

| (Being issue of 10,000 shares @ Rs. 10 each fully paid in payment of property purchased ) | |||||

| C) | Bank A/c (40,000 X 2) | Dr. | 80,000 | ||

| To Share Application A/c | 80,000 | ||||

| (Being the receipt of application money on 40,000 shares @ Rs.2 per share ) | |||||

| D) | Share Application A/c (40,000 X 2) | Dr. | 80,000 | ||

| To Share capital A/c | 80,000 | ||||

| (Being the transfer of application money on 40,000 shares @ Rs. 2 per share ) | |||||

| E) | Share Allotment A/c (40,000 X 2) | Dr. | 80,000 | ||

| To Share capital A/c | 80,000 | ||||

| (Being allotment money due on allotment of 40,000 shares @ Rs. 2 per share ) | |||||

| F) | Bank A/c (40,000 X 2) | Dr. | 80,000 | ||

| To Share allotment A/c | 80,000 | ||||

| (Being allotment money received in full) | |||||

| G) | Share first Call A/c (40,000 X 3) | Dr. | 1,20,000 | ||

| To Share capital A/c | 1,50,000 | ||||

| (Being amount due on first call of 40,000 share @ Rs. 3 per share) | |||||

| H) | Bank A/c (39,900 X 3) | Dr. | 1,19,700 | ||

| Calls in arrear A/c | Dr. | 3,000 | |||

| To Share first Call A/c | 1,20,000 | ||||

| (Being amount received on first call of 39,900 share @ Rs. 3 per share ) | |||||

| I) | Share first Call A/c (40,000 X 3) | Dr. | 1,20,000 | ||

| To Share capital A/c | 1,50,000 | ||||

| (Being amount due on final call of 40,000 share @ Rs. 3 per share) | |||||

| J) | Bank A/c (39,900 X 3) | Dr. | 1,19,700 | ||

| To Share first Call A/c | 1,19,700 | ||||

| (Being amount received on final call of 39,900 share @ Rs. 3 per share ) | |||||

| k) | Share capital A/c ( 100 X 10) | Dr. | 1,000 | ||

| To Share Forfeited A/c ( 100 X 3) | 400 | ||||

| To calls in arrear A/c ( 100 X 6) | 600 | ||||

| (Being forfeitures of 100 shares for non payments of first & Final call money ) | |||||

| L) | Bank A/c (100 X 8.5 ) | Dr. | 850 | ||

| Share Fortified A/c (100X1.5) | Dr. | 150 | |||

| To Share capital A/c | 1,000 | ||||

| M) | Share Fortified A/c (400-150) | Dr. | 250 | ||

| To Capital Reserve A/c | 250 | ||||

| (Being balance in share fortified transferred to capital reserve) | |||||

| Date | Particulars |

Note No. | FIG. RELATING TO CURRENT REPORTNG PERIOD |

|---|---|---|---|

| (i) | Equity & Liability | ||

| Shareholders fund | |||

| Share Capital | 1 | 5,00,000 | |

| Reserve & surplus | 2 | 250 | |

| Non current Liabilities | |||

| Current Liabilities | |||

| Total | 5,00,250 | ||

| (ii) | Assets | ||

| Non -Current Assets | |||

| Tangible Asset | 1,00,000 | ||

| Current Assets | |||

| Cash & Cash equivalent | 4,00,250 | ||

| Total | 5,00,250 |

| Date | Particulars |

Note No. | FIG. RELATING TO CURRENT REPORTNG PERIOD | FIG. RELATING TO PREVIOUS REPORTNG PERIOD |

|---|---|---|---|---|

| 1 | Shared capital | |||

| Authorized capital | 5,00,000 | |||

| (50,000 shares of Rs. 10 each) | ||||

| 2 | Reserve & surplus | |||

| Capital Reserve | 250 | |||

| 3 | Tangible Asset | |||

| Property | 1,00,000 | |||

| 4 | Cash & Cash equivalent | |||

| Cash at bank | 4,00,250 |

It all about Question 33 Chapter 8 of +2-Part-1, If you have any problem please comment below.

https://tutorstips.com/forfeiture-of-shares-its-accounting-entries/

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 33 Chapter 8 of +2-Part-1 - USHA Publication 12 Class Part - 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to USHA Publication +2 Part 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 33 Chapter 8 of +2-Part-1 - USHA Publication 12 Class Part - 1" instantly.

12 September 2021

12 September 2021

17 September 2021