Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

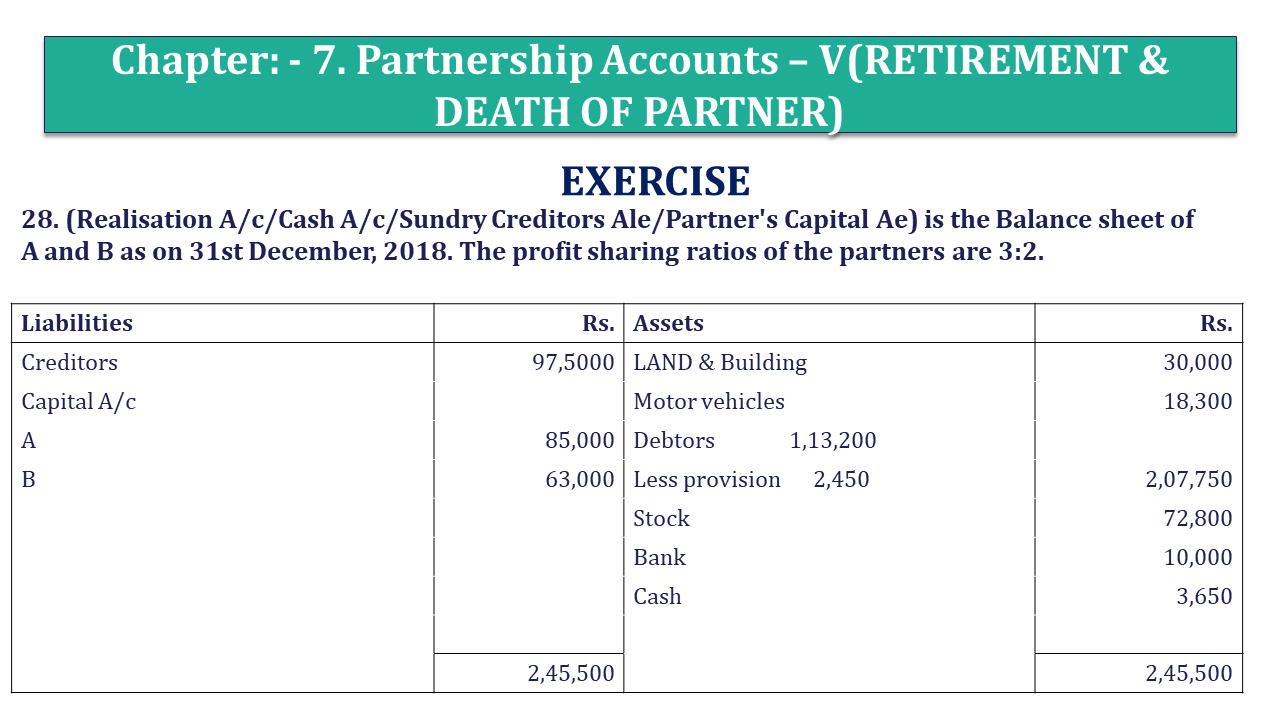

Question 28 Chapter 7 of +2-Part-1

28. (Realisation A/c/Cash A/c/Sundry Creditors Ale/Partner's Capital Ae) is the Balance sheet of A and B as on 31st December, 2018. The profit sharing ratios of the partners are 3:2.

| Liabilities | Rs. | Assets | Rs. |

| Creditors | 97,500 | LAND & Building | 30,000 |

| Capital A/c | Motor vehicles | 18,300 | |

| A | 85,000 | Debtors 1,13,200 | |

| B | 63,000 | Less provision 2,450 | 2,07,750 |

| Stock | 72,800 | ||

| Bank | 10,000 | ||

| Cash | 3,650 | ||

| 2,45,500 | 2,45,500 |

The partners decided to dissolve the firm on and from the date of the balance sheet Motor vehicles and stock were sold for cash at Rs. 16,950 and Rs. 77,600 respectively and all debtors accounts were realised in full. A took over the land and building at an agreed valuation of Rs. 43,500. Creditors were paid off subject to discount amounting to Rs. 1,700 Expenses of realisation were Rs. 1,250.

Prepare realisation account, cash account, sundry creditors account and partners capital accounts to close the books of the firm as result of its dissolution.

We are providing a solution of Question 28 Chapter 7 of +2 Part-1 in two formats. one is in Video format and another is in article format. Check out both formats as follows:

Realisation A/c

| Particulars |

Amount | Particulars | Amount | ||

|---|---|---|---|---|---|

| To Debtors A/c | 1,13,200 | By Creditors A/c | 97,500 | ||

| To Stock A/c | 72,800 | By Provision for debts A/c – | 2,450 | ||

| To motor vehicles A/c | 18,300 | By cash A/c | |||

| To land & building A/c | 30,000 | Debtors | 1,13,200 | ||

| To cash A/c | Motor vehicles | 16,950 | |||

| Realisation Expenses | 1,250 | Stock | 77,600 | 2,07,750 | |

| Creditors paid off | 95,800 | 97,050 | By A’s capital A/c | ||

| To profit on realisation | Land & Building taken over | 43,500 | |||

| A’s capital A/c | 11,910 | ||||

| B’s capital A/c | 7,940 | 19,850 | |||

| 3,51,200 | 3,51,200 | ||||

Partners’ Capital Account

| Particulars | A | B | Particulars | A | B |

|---|---|---|---|---|---|

| To Realisation A/c | By Balance b/d | 85,000 | 63,000 | ||

| LAND & BUILDING | 43,500 | By Realisation A/c | 11,910 | 7,940 | |

| To Cash A/c | 53,410 | 70,940 | |||

| 96,910 | 70,940 | 96,910 | 70,940 |

Cash A/c

| Particulars | Amount | Particulars | Amount | ||

|---|---|---|---|---|---|

| To balance b/d | 3,650 | By Realisation A/c | |||

| To Realisation A/c | Creditors & expenses paid off | 97,050 | |||

| Assets realised | 2,07,750 | By A’s capital A/c | 53,410 | ||

| To BANK A/c | 10,000 | By B’s capital A/c | 70,940 | ||

| 2,21,400 | 2,21,400 | ||||

Sundry Creditors A/c

| Particulars | Amount | Particulars | Amount | ||

|---|---|---|---|---|---|

| To Realisation A/c | 1,700 | By balance b/d | 97,500 | ||

| To Cash A/c | 95,800 | ||||

| 97,500 | 97,500 | ||||

Comment if you have any questions.

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 28 Chapter 7 of +2 Part-1 - USHA Publication 12 Class Part - 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to USHA Publication +2 Part 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 28 Chapter 7 of +2 Part-1 - USHA Publication 12 Class Part - 1" instantly.