Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1 | Tutorstips

Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1

By Sarbjit Singh (B.Com and M.Com)|Published: 24 November 2020|Last Updated: 23 June 2026|T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1Chapter No. 7 - Dissolution of a Partnership Firm

Focus Topic:Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1

Estimated Reading Time:3 mins

Comprehensive academic guide covering core concepts of Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

Syllabus-aligned study material with detailed definitions, formats, and practical examples.

Interactive check: Includes a custom practice quiz at the bottom of the article to self-evaluate knowledge.

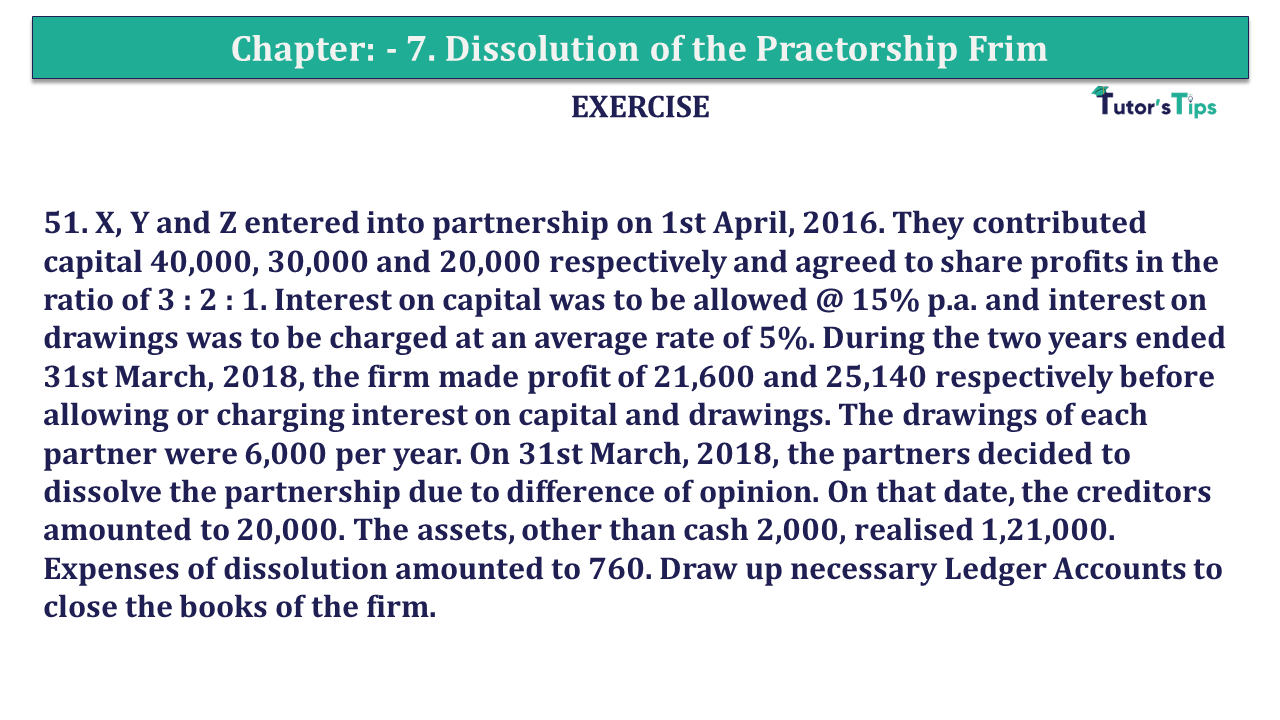

Question 20 Chapter 7 of +2-A

20. Bale and Yale are equal partners of a firm. They decide to dissolve their partnership on 31st March 2018 at which date their Balance Sheet stood as:

Liabilities

Amount

Assets

Amount

Capital A/cs:

Building

45,000

Bale

50,000

Machinery

15,000

Yale

40,000

90,000

Furniture

12,000

General Reserve

8,000

Debtors

8,000

Bale's Loan A/c

3,000

Stock

24,000

Creditors

14,000

Bank

11,000

1,15,000

1,15,000

a The assets realized were: Stock 22,000; Debtors 7,500; Machinery 16,000; Building 35,000. b Yale took over the Furniture at 9,000. c Bale agreed to accept 2,500 in full settlement of his Loan Account . d Dissolution Expenses amounted to 2,500. Prepare the: i Realization Account; ii Capital Accounts of Partners; iii Bale's Loan Account; iv Bank Account

The solution of Question 20 Chapter 7 of +2-A: -

Realization Account

Particular

Amount

Particular

Amount

Building

45,000

Sundry Creditors

14,000

Machinery

15,000

Bank A/c:

Furniture

12,000

Stock

22,000

Debtors

8,000

Debtors

7,500

Stock

24,000

Machinery

16,000

Bank A/c:

Building

35,000

80,500

Creditors

14,000

Bale’s Loan

500

Expenses

2,500

16,500

Yale’s Capital A/c Furniture

9,000

Realization Loss

Bale’s Capital A/c

8,250

Yale’s Capital A/c

8,250

16,500

1,20,500

1,20,500

Partners’ Capital Account

Part.

Bale

Yale

Part.

Bale

Yale

To Realization loss

8,250

8,250

By Balance B/d

50,000

40,000

To Realization A/c

-

9,000

By General Reserve Old Ratio

4,000

4,000

-

To Balance c/d

45,750

26,750

54,000

44,000

54,000

44,000

Bale’s Loan Account

Particular

Amount

Particular

Amount

Bank A/c

2,500

Balance b/d

3,000

Realization A/c

500

3,000

3,000

Bank Account

Particular

Amount

Particular

Amount

Balance b/d

11,000

Bale’s Loan

2,500

Realization A/c

80,500

Realization A/c

16,500

Bale’s Capital A/c

45,750

Yale’s Capital A/c

26,750

91,500

91,500

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms

👤

Author & Educator

Sarbjit SinghB.Com and M.Com

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

❓ Frequently Asked Questions

What is the main topic of "Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1"?

This guide covers "Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

Who can benefit from this guide on "Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1"?

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

Where can I practice questions related to "Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1"?

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.20 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.