Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

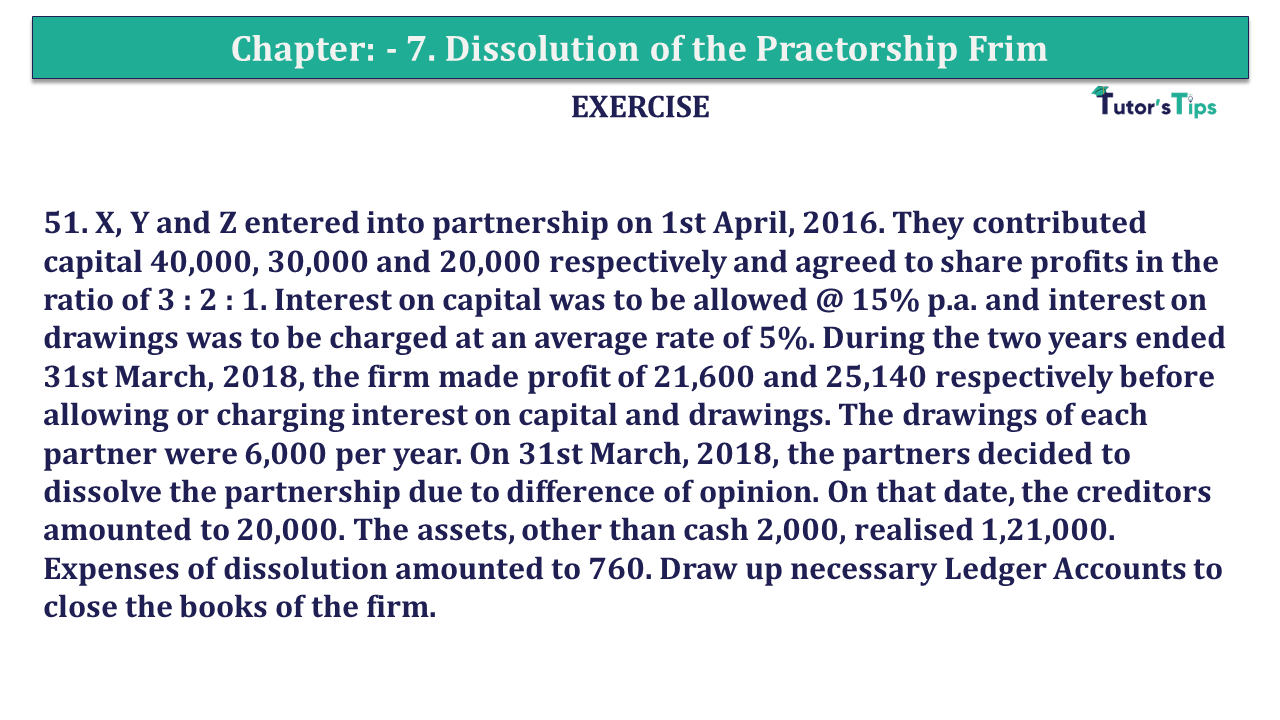

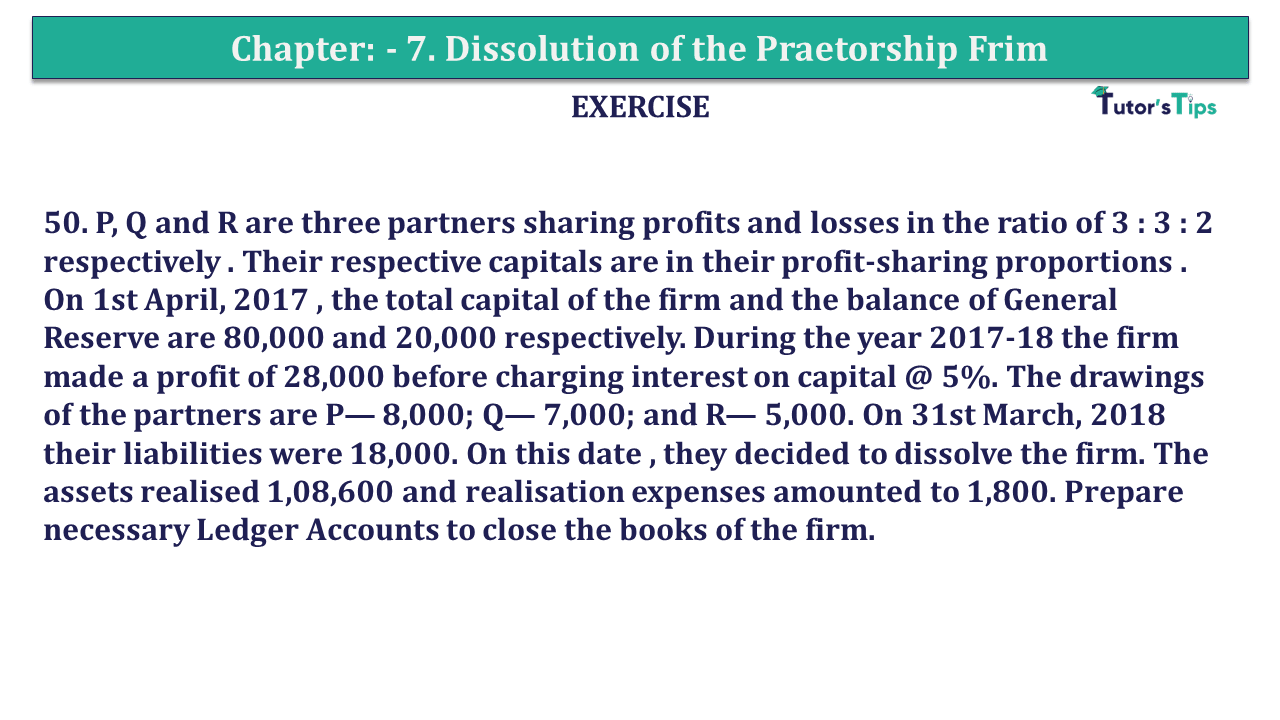

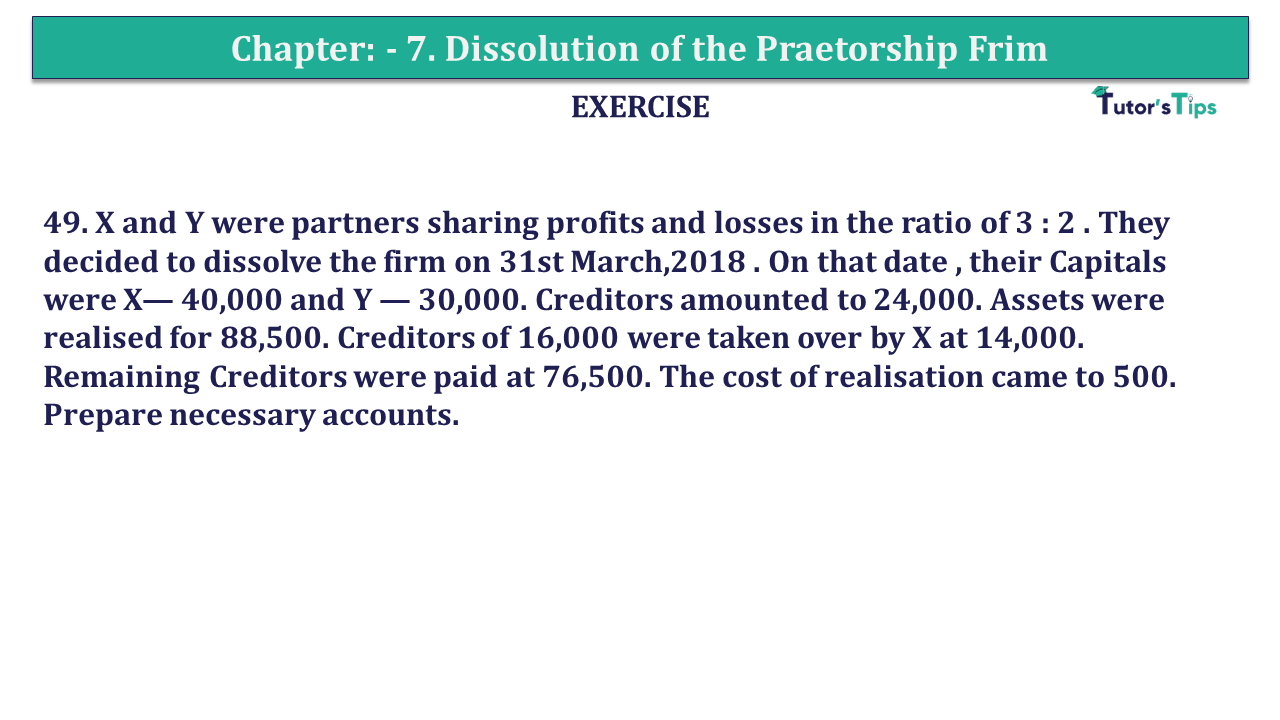

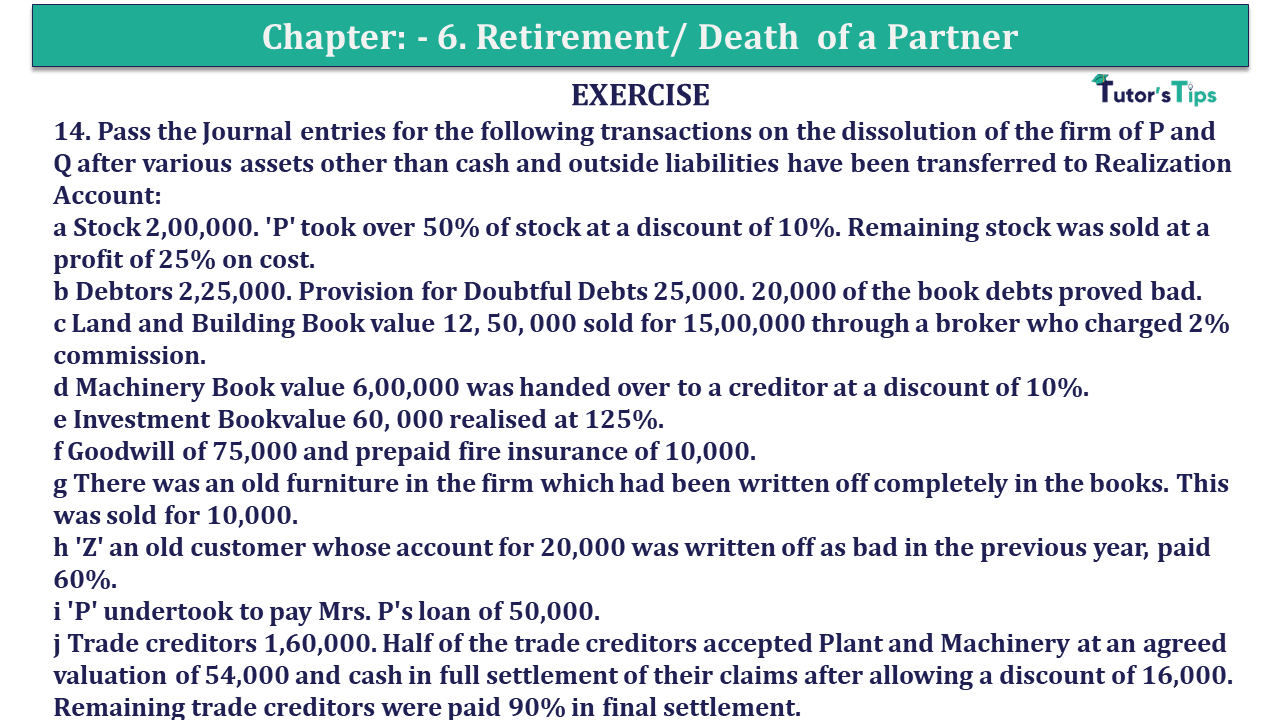

Question 14 Chapter 7 of +2-A

14. Pass the Journal entries for the following transactions on the dissolution of the firm of P and Q after various assets other than cash and outside liabilities have been transferred to Realization Account:

a Stock 2,00,000. 'P' took over 50% of stock at a discount of 10%. Remaining stock was sold at a profit of 25% on cost.

b Debtors 2,25,000. Provision for Doubtful Debts 25,000. 20,000 of the book debts proved bad.

c Land and Building Book value 12, 50, 000 sold for 15,00,000 through a broker who charged 2% commission.

d Machinery Book value 6,00,000 was handed over to a creditor at a discount of 10%.

e Investment Bookvalue 60, 000 realised at 125%.

f Goodwill of 75,000 and prepaid fire insurance of 10,000.

g There was an old furniture in the firm which had been written off completely in the books. This was sold for 10,000.

h 'Z' an old customer whose account for 20,000 was written off as bad in the previous year, paid 60%.

i 'P' undertook to pay Mrs. P's loan of 50,000.

j Trade creditors 1,60,000. Half of the trade creditors accepted Plant and Machinery at an agreed valuation of 54,000 and cash in full settlement of their claims after allowing a discount of 16,000.

Remaining trade creditors were paid 90% in final settlement.

| Date | Particulars |

L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| a | P’s Capital A/c | Dr. | 90,000 | ||

| Bank A/c | Dr. | 1,25,000 | |||

| To Realization A/c | 2,15,000 | ||||

| (Being Stock realized) | |||||

| b | Bank A/c | Dr. | 2,05,000 | ||

| To Realization A/c | 2,05,000 | ||||

| (Being Debtors realized) | |||||

| c | Bank A/c | Dr. | 14,70,000 | ||

| To Realization A/c | 14,70,000 | ||||

| ( Being Land and Building realized) | |||||

| d | No Entry | ||||

| e | Bank A/c | Dr. | 75,000 | ||

| To Realization A/c | 75,000 | ||||

| (Being Investment realized) | |||||

| f | No Entry | ||||

| g | Bank A/c | Dr. | 10,000 | ||

| To Realization A/c | 10,000 | ||||

| (Being Unrecorded furniture realized) | |||||

| h | Bank A/c | Dr. | 12,000 | ||

| To Realization A/c | 12,000 | ||||

| (Being Bad debts recovered) | |||||

| i | Realization A/c | Dr. | 50,000 | ||

| To P’s Capital A/c | 50,000 | ||||

| (Being Wife ′s loan paid by partner) | |||||

| j | Realization A/c | Dr. | 82,000 | ||

| To Bank A/c 10, 000 +72, 000 | 82,000 | ||||

| (Being Creditors paid) | |||||

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Q.No.14 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.14 | Chapter 7 – Dissolution of a Partnership Firm | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.