Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Advertisement

Advertisement

Advertisement

Advertisement

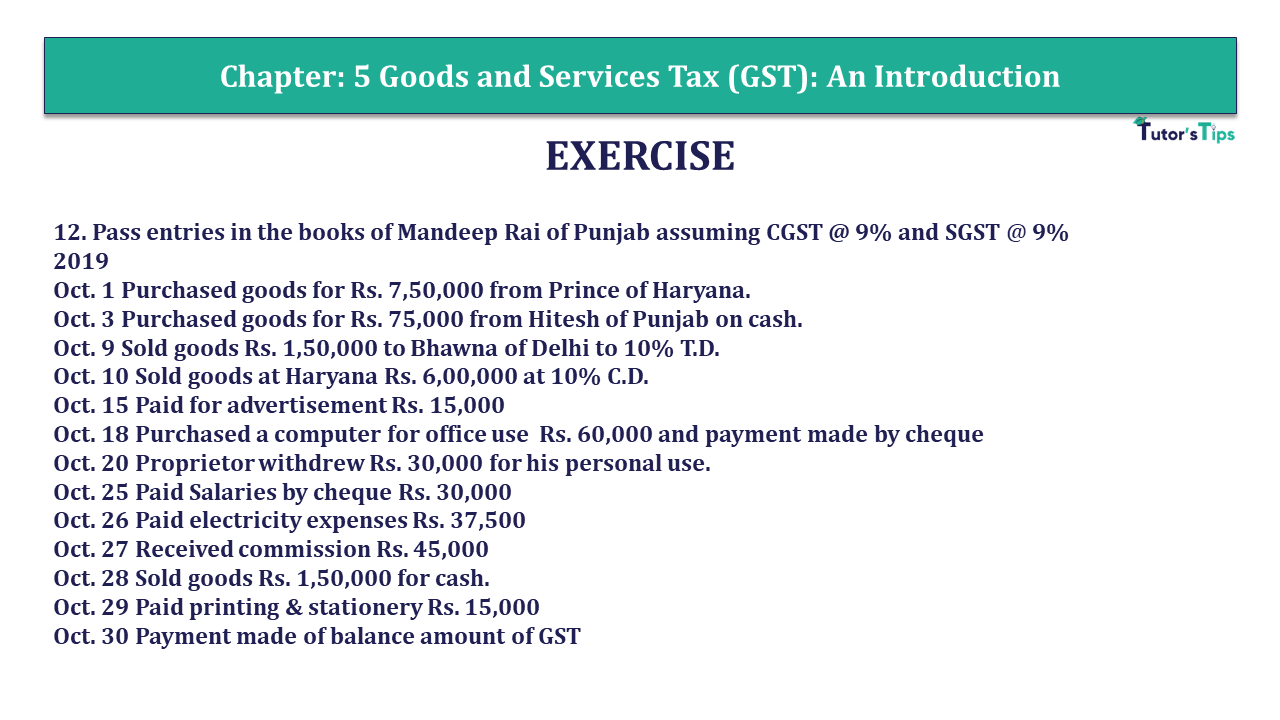

Question 12 Chapter 5 - Unimax

12. Pass entries in the books of Mandeep Rai of Punjab assuming CGST @ 9% and SGST @ 9%

2019

Oct. 1 Purchased goods for Rs. 7,50,000 from Prince of Haryana.

Oct. 3 Purchased goods for Rs. 75,000 from Hitesh of Punjab on cash.

Oct. 9 Sold goods Rs. 1,50,000 to Bhawna of Delhi to 10% T.D.

Oct. 10 Sold goods at Haryana Rs. 6,00,000 at 10% C.D.

Oct. 15 Paid for advertisement Rs. 15,000

Oct. 18 Purchased a computer for office use Rs. 60,000 and payment made by cheque

Oct. 20 Proprietor withdrew Rs. 30,000 for his personal use.

Oct. 25 Paid Salaries by cheque Rs. 30,000

Oct. 26 Paid electricity expenses Rs. 37,500

Oct. 27 Received commission Rs. 45,000

Oct. 28 Sold goods Rs. 1,50,000 for cash.

Oct. 29 Paid printing & stationery Rs. 15,000

Oct. 30 Payment made of balance amount of GST

JOURNAL OF MANDEEP RAI

| Date | Particulars | L.F. | Debit | Credit | |

|---|---|---|---|---|---|

| 2019 | |||||

| Oct. 1 | Purchases A/c | Dr. | 7,50,000 | ||

| Input IGST A/c | Dr. | 1,35,000 | |||

| To Prince A/c | 8,85,000 | ||||

| (Being goods purchased outside the state) | |||||

| Oct.3 | Purchases A/c | Dr. | 75,000 | ||

| Input CGST A/c | Dr. | 6,750 | |||

| Input SGST A/c | Dr. | 6,750 | |||

| To Cash A/c | 88,500 | ||||

| (Being goods purchased inside the state) | |||||

| Oct. 9 | Bhawna A/c | Dr. | 1,59,300 | ||

| To Sales A/c | 1,35,000 | ||||

| To Output IGST A/c | 24,300 | ||||

| (Being goods sold outside the state) (WNI) | |||||

| Oct. 10 | Cash A/c | Dr. | 6,37,200 | ||

| Discount allowed A/c | Dr. | 70,800 | |||

| To Sales A/c | 6,00,000 | ||||

| To Output IGST A/c | 1,08,000 | ||||

| (Being good sold outside the state at C.D) (WNII) | |||||

| Oct. 15 | Advertisement A/c | Dr. | 15,000 | ||

| Input CGST A/c | Dr. | 1,350 | |||

| Input SGST A/c | Dr. | 1,350 | |||

| To Cash A/c | 17,700 | ||||

| (Being advertisement paid) | |||||

| Oct. 18 | Office equipment A/c | Dr. | 60,000 | ||

| Input CGST A/c | Dr. | 5,400 | |||

| Input SGST A/c | Dr. | 5,400 | |||

| To Bank A/c | 70,800 | ||||

| (Being computer purchased) | |||||

| Oct. 20 | Drawings A/c | Dr. | 30,000 | ||

| To Cash A/c | 30,000 | ||||

| (Being proprietor withdrew for personal use) | |||||

| Oct. 25 | Salaries A/c | Dr. | 30,000 | ||

| To Bank A/c | 30,000 | ||||

| (Being salaries paid) | |||||

| Oct. 26 | Electricity Expense A/c | Dr. | 37,500 | ||

| To Cash A/c | 37,500 | ||||

| (Being electricity bill paid) | |||||

| Oct. 27 | Cash A/c | Dr. | 53,100 | ||

| To Commission Received A/c | 45,000 | ||||

| To Output CGST A/c | 4,050 | ||||

| To Output SGST A/c | 4,050 | ||||

| (Being commission received) | |||||

| Oct. 28 | Cash A/c | Dr. | 1,77,000 | ||

| To Sales A/c | 1,50,000 | ||||

| To Output CGST A/c | 13,500 | ||||

| To Output SGST A/c | 13,500 | ||||

| (Being goods sold for cash) | |||||

| Oct. 29 | Printing and Stationary A/c | Dr. | 15,000 | ||

| Input CGST A/c | Dr. | 1,350 | |||

| Input SGST A/c | Dr. | 1,350 | |||

| To Cash A/c | 17,700 | ||||

| (Being printing& stationery paid) | |||||

| Oct. 30 | Output IGST A/c | Dr. | 1,32,300 | ||

| To Input IGST A/c | 1,32,300 | ||||

| (Being IGST adjusted) (WN III) | |||||

| Output CGST A/c | Dr. | 17,550 | |||

| To Input CGST A/c | 14,850 | ||||

| To Input IGST A/c | 2,700 | ||||

| (Being CGST adjusted) (WN IV) | |||||

| Output SGST A/c | 17,550 | ||||

| To Input SGST A/c | 14,850 | ||||

| To Bank A/c | 2,700 | ||||

| (Being SGST adjusted and payment of balance amount Paid) (WN V) | |||||

Working Notes:

| 1. | List price of goods Sold | 1,50,000 |

| Less: Trade discount@ 10% | 15,000 | |

| 1,35,000 | ||

| Add: IGST@ 18% | 24,300 | |

| 1,59,300 | ||

| 2. | List price of goods sold | 6,00,000 |

| Add: IGST@ 18% | 1,08,000 | |

| 7,08,000 | ||

| Less: C.D @ 10% | 70,800 | |

| 6,37,200 | ||

| 3. | First of all output IGST will be adjusted against Input IGST | |

| Input IGST | 1,35,000 | |

| Less Output IGST (i.e 24,300+1,08,000= 1,32,300) | 1,32,300 | |

| IGST credit | 2,700 | |

| 4. | This balance of Rs. 2,700 of 1GST credit will be first applied to set off CGST and the balance IF any will be applied to set off SGST | |

| Total Output CGST (Rs. 4,050+Rs. 13,500) | 17,550 | |

| Less: Input CGST (6,750+1,350 +5,400 +1,350) | 14,850 | |

| amount adjusted against IGST credit | 2,700 | |

| 5. | Total Output CGST (Rs. 4,050+Rs. 13,500) | 17,550 |

| Less: Total Input SGST (6,750+1,350 +5,400 +1,350) | 14,850 | |

| Balance paid off | 2,700 |

This is all about the Question 12 Chapter 5 - Unimax. You can check out the following article to better understand:

Opening Journal Entry – its Rules and Examples

You Can also read all above articles in Hindi on our Hindi Website

Opening Journal Entry – its Rules and Examples - In Hindi

Thanks, Please Like and share with your friends

Comment if you have any doubt in the Question 12 Chapter 5 - Unimax.

You can also Check out the solved question of other Chapters: -

Part-I

Students may Choose only one part from the Part II and Part III

Part-II

Part-III

You can also Check out the other Books' Solution: -

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Question 12 Chapter 5 - Unimax Publications of Class 11", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to Unimax class 11 - 2021.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Question 12 Chapter 5 - Unimax Publications of Class 11" instantly.