Loading Tutorstips...

✦ FREE LEARNING — CLASS 11 & 12 — CBSE · PSEB — ACCOUNTS · ECONOMICS · BST ✦

Question 101 Chapter 5 of +2-A

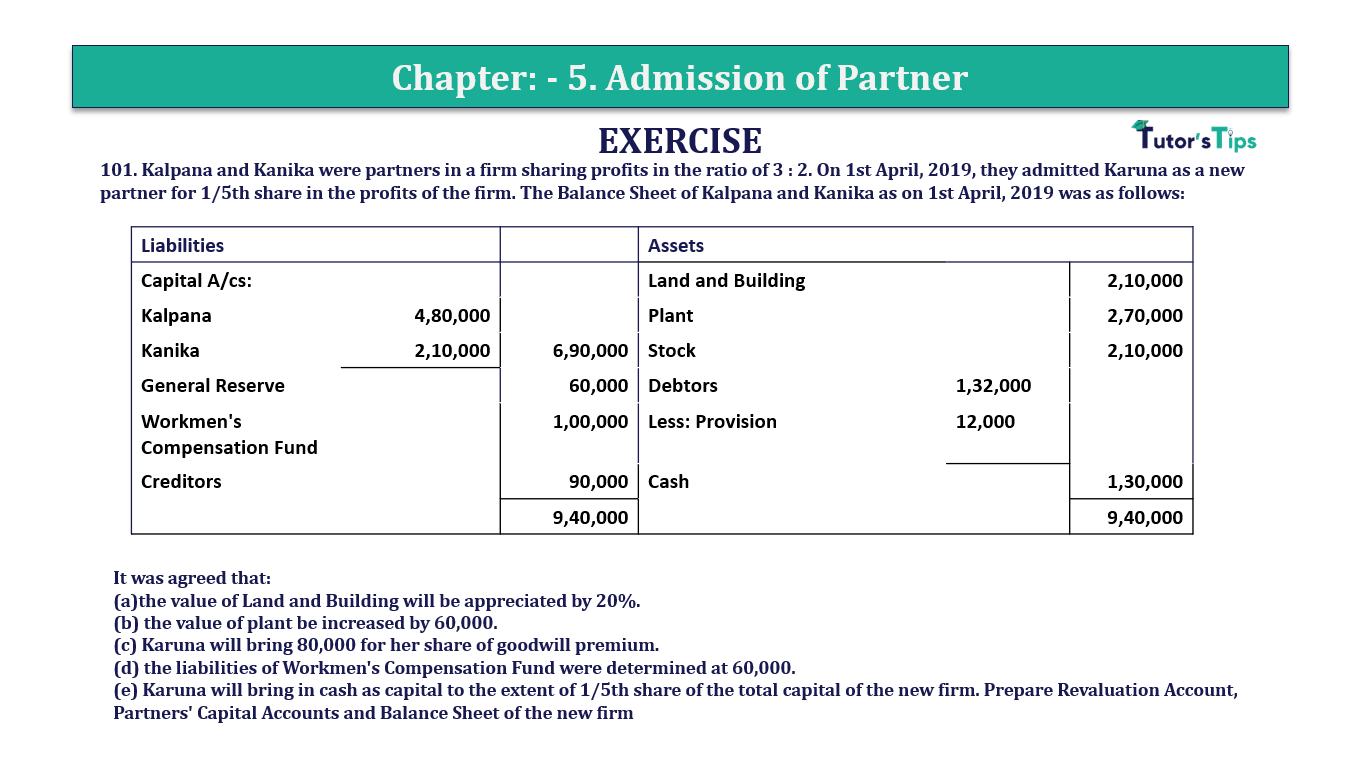

101. Kalpana and Kanika were partners in a firm sharing profits in the ratio of 3 : 2. On 1st April, 2019, they admitted Karuna as a new partner for 1/5th share in the profits of the firm. The Balance Sheet of Kalpana and Kanika as on 1st April, 2019 was as follows:

| Liabilities | Assets | ||||

| Capital A/cs: | Land and Building | 2,10,000 | |||

| Kalpana | 4,80,000 | Plant | 2,70,000 | ||

| Kanika | 2,10,000 | 6,90,000 | Stock | 2,10,000 | |

| General Reserve | 60,000 | Debtors | 1,32,000 | ||

| Workmen's Compensation Fund | 1,00,000 | Less: Provision | 12,000 | ||

| Creditors | 90,000 | Cash | 1,30,000 | ||

| 9,40,000 | 9,40,000 |

It was agreed that:

(a)the value of Land and Building will be appreciated by 20%.

(b) the value of plant be increased by 60,000.

(c) Karuna will bring 80,000 for her share of goodwill premium.

(d) the liabilities of Workmen's Compensation Fund were determined at 60,000.

(e) Karuna will bring in cash as capital to the extent of 1/5th share of the total capital of the new firm. Prepare Revaluation Account, Partners' Capital Accounts and Balance Sheet of the new firm

Revaluation Account

| Particular |

Amount | Particular | Amount | ||

|---|---|---|---|---|---|

| Land and Building A/c | 42,000 | ||||

| Plant A/c | 60,000 | ||||

| Profit on Revaluation | |||||

| Kalpana’s Capital A/c | 61,200 | ||||

| Kanika’s Capital A/c | 40,800 | 1,02,000 | |||

| 1,02,000 | 1,02,000 | ||||

Partners’ Capital Account

| Parti culars |

Kalpana | Kanika | Karuna |

Partic |

Kalpana | Kanika | Karuna |

|---|---|---|---|---|---|---|---|

| By Balance B/d | 4,80,000 | 2,10,000 | - | ||||

| By Cash | - | - | 2,43,000 | ||||

| By General Reserve | 36,000 | 24,000 | - | ||||

| By Workmen’s Compensation Fund | 24,000 | 16,000 |

- |

||||

| By Premium for Goodwill | 48,000 | 32,000 | - | ||||

| By Revaluation | 61,200 | 40,800 | - | ||||

| To Balance c/d | 6,49,200 | 3,22,800 | 2,43,000 | ||||

| 6,49,200 | 3,22,800 | 2,43,000 | 6,49,200 | 3,22,800 | 2,43,000 |

Balance Sheet

| Liabilities |

Amount | Assets | Amount | ||

|---|---|---|---|---|---|

| Creditors | 90,000 | Cash in Hand | 4,53,000 | ||

| Liability for Workmen Compensation | 60,000 | Debtors | 1,32,000 | ||

| Capital: | Less: Provision for debtors | 12,000 | 1,20,000 | ||

| Kalpana | 6,49,200 | Stock | 2,10,000 | ||

| Kanika | 3,22,800 | Land and Building | 2,52,000 | ||

| Karuna | 2,43,000 | 12,15,000 | Plant | 3,30,000 | |

| 13,65,000 | 13,65,000 | ||||

Working Note:-

Karuna is admitted for 1/5th share

Let the total share of the business = 1

| Remaining share | = | 1 | - | 1 |

| 5 |

| = | 5 - 1 |

| 5 |

| = | 4 |

| 5 |

To Calculate to New Ratio distribute the remaining share in the old ratio of old partners’

New Ratio = Combined share of Kalpana and Kanika X Old Ratio

| Kalpana's Share | = | 4 | X | 3 |

| 5 | 5 |

| = | 12 |

| 25 |

| Kanika's Share | = | 4 | X | 2 |

| 5 | 5 |

| = | 8 |

| 25 |

New Profit sharing Ratio = 12 : 8 : 5

Calculation of Sacrificing Ratio

| Kalpana's Share | = | 3 | - | 12 |

| 5 | 15 |

| = | 15 -12 |

| 25 |

| = | 3 |

| 25 |

| Kanika | = | 2 | - | 8 |

| 5 | 25 |

| = | 10- 8 |

| 25 |

| = | 2 |

| 25 |

Sacrificing Ratio = 3 : 2

Calculate of Karuna's Capital

| Adjusted Capital of Kalpana | = | 6,49,200 |

| Adjusted Capital of Kanika | = | 3,22,800 |

| Total Adjusted Capital | = | 9,72,000 (6,49,200+3,22,800) |

Karuna's Capital = Total Adjusted Capital X Karna’s Profit Share X Reciprocal of combined new Share of Old Partner

| Karuna’s Share of Goodwill | = | 9,72,000 | x | 1 | x | 5 |

| 5 | 4 | |||||

| = | 2,43,000 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication

Accounting & Commerce Educator

Sarbjit Singh holds a B.Com and M.Com degree and has over 12 years of teaching experience in double entry bookkeeping, financial accounting, and business studies.

This guide covers "Q.No.101 | Chapter 5 – Admission of Partner | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1", focusing on key definitions, step-by-step concepts, applications, and revision guidelines relevant to T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1.

It is primarily curated for Class 11 and Class 12 high school commerce, accounting, and economics students, as well as aspirants preparing for board exams or CA Foundation.

You can take our custom-built interactive practice quiz directly on this page to test your understanding of "Q.No.101 | Chapter 5 – Admission of Partner | T.S. Grewal 12 Class Book Keeping Part - A - Vol. 1" instantly.