Advertisement

Question 84 Chapter 5 of +2-A

Advertisement

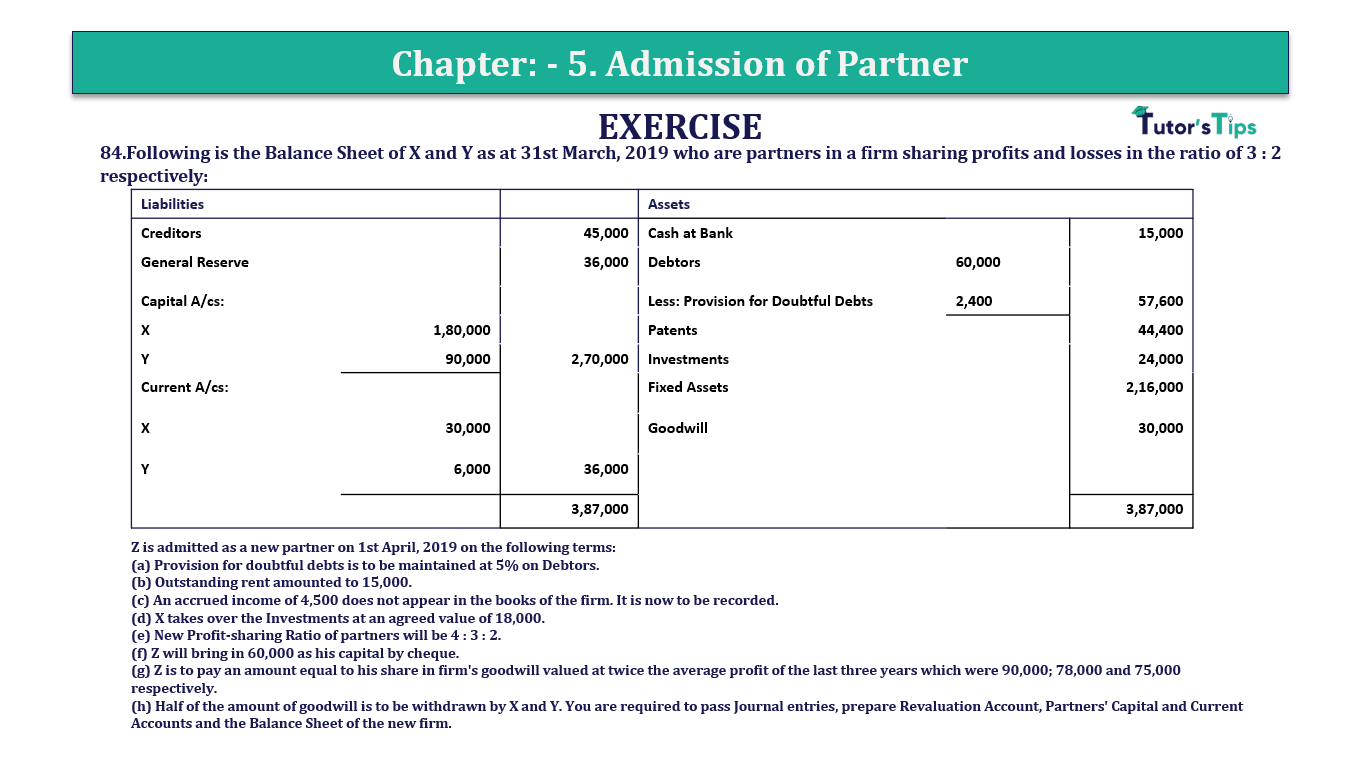

84.Following is the Balance Sheet of X and Y as at 31st March, 2019 who are partners in a firm sharing profits and losses in the ratio of 3 : 2 respectively:

| Liabilities | Assets | ||||

| Creditors | 45,000 | Cash at Bank | 15,000 | ||

| General Reserve | 36,000 | Debtors | 60,000 | ||

| Capital A/cs: | Less: Provision for Doubtful Debts | 2,400 | 57,600 | ||

| X | 1,80,000 | Patents | 44,400 | ||

| Y | 90,000 | 2,70,000 | Investments | 24,000 | |

| Current A/cs: | Fixed Assets | 2,16,000 | |||

| X | 30,000 | Goodwill | 30,000 | ||

| Y | 6,000 | 36,000 | |||

| 3,87,000 | 3,87,000 |

Z is admitted as a new partner on 1st April, 2019 on the following terms:

(a) Provision for doubtful debts is to be maintained at 5% on Debtors.

(b) Outstanding rent amounted to 15,000.

(c) An accrued income of 4,500 does not appear in the books of the firm. It is now to be recorded.

(d) X takes over the Investments at an agreed value of 18,000

.(e) New Profit-sharing Ratio of partners will be 4 : 3 : 2.

(f) Z will bring in 60,000 as his capital by cheque.

(g) Z is to pay an amount equal to his share in firm’s goodwill valued at twice the average profit of the last three years which were 90,000; 78,000 and 75,000 respectively.

(h) Half of the amount of goodwill is to be withdrawn by X and Y. You are required to pass Journal entries, prepare Revaluation Account, Partners’ Capital and Current Accounts and the Balance Sheet of the new firm.

The solution of Question 84 Chapter 5 of +2-A: –

| Revaluation Account | |||||

| Particular | Amount | Particular | Amount | ||

| Prov. for D. Debts | 600 | Accrued Income | 4,500 | ||

| Outstanding Rent | 15,000 | ||||

| Investment | 6,000 | ||||

| Loss transferred to | |||||

| X’s Current A/c | 10,260 | ||||

| Y’s Current A/c | 6,840 | 17,100 | |||

| 21,600 | 21,600 | ||||

Advertisement-X

| Partners’ Capital Account | |||||||

| Parti culars | X | Y | Z | Partic | X | Y | Z |

| By Balance B/d | 1,80,000 | 90,000 | – | ||||

| By Bank A/c A/c | – | – | 60,000 | ||||

| To Balance c/d | 1,80,000 | 90,000 | 60,000 | ||||

| 1,80,000 | 90,000 | 60,000 | 30,000 | 90,000 | 60,000 | ||

| Partners’ Capital Account | |||||||

| Parti culars | X | Y | Z | Partic | X | Y | Z |

| To Revaluation A/c | 10,260 | 6,840 | – | By Balance B/d | 30,000 | 6,000 | – |

| To Goodwill A/c | 18,000 | 12,000 | – | By General Reserve | 21,600 | 14,400 | |

| To Bank A/c | 12,600 | 5,400 | – | By Premium for Goodwill | 25,200 | 10,800 | |

| To Investments A/c | 18,000 | – | – | ||||

| To Balance c/d | 17,940 | 6,960 | – | – | |||

| 76,800 | 31,200 | – | 76,800 | 31,200 | – | ||

| Balance Sheet | |||||

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 45,000 | Patents | 44,400 | ||

| Outstanding Rent | 15,000 | Fixed Assets | 2,16,000 | ||

| Capital A/cs: | Accrued Income | 4,500 | |||

| X | Debtors | 60,000 | |||

| Y | 1,80,000 | Less: 5% Reserve for D. Debts | 3,000 | 57,000 | |

| Z | 90,000 | Cash at Bank | (15,000 + 96,000 – 18,000) | 93,000 | |

| C | 60,000 | 3,30,000 | |||

| Current A/cs: | |||||

| X | 17,940 | ||||

| Y | 6,960 | 24,900 | |||

| 4,14,900 | 4,14,900 | ||||

| Date | Particulars | L.F. | Debit | Credit | |

| Cash A/c | Dr | 96,000 | |||

| To Z’s Capital | 60,000 | ||||

| To Premium for Goodwill A/c | 36,000 | ||||

| (Z brought Capital and share of goodwill) | |||||

| Premium for Goodwill A/c | Dr | 36,000 | |||

| To X’s Current A/c | 25,200 | ||||

| To Y’s Current A/c | 10,800 | ||||

| (Premium for Goodwill transferred to partners current account in sacrificing ratio i.e. 7:3) | |||||

| X’s Current A/c | Dr | 12,600 | |||

| Y’s Current A/c | Dr | 5,400 | |||

| To Bank A/c | 18,000 | ||||

| (Half of goodwill withdrawn by partners) | |||||

Working Note:-

Calculation of Z’s Share of Premium for Goodwill

| Average Profit | = | 90,000+78,000+75,000/3 |

| = | Rs 81,000 | |

| Firm’s Goodwill | = | 81,000×2 |

| = | Rs 1,62,000 | |

| Z’s share | = | 1,62,000×2/9 |

| = | Rs 36,000 |

Advertisement-Y

Advertisement-X

Calculation of Sacrificing Ratio

Sacrificing Ratio=Old Ratio-New

| X’s Sacrificing Ratio | = | 3 | – | 4 |

| 5 | 9 |

| = | 27 – 20 | |

| 45 |

| = | 7 | ||

| 45 |

| Y’s Sacrificing Ratio | = | 2 | – | 4 |

| 5 | 9 |

| = | 18 – 15 | |

| 45 |

| = | 3 | |

| 45 |

Sacrificing Ratio of X and Y= 7 : 3

Calculation of Share of Premium of Goodwill

Distribution of Premium for Goodwill

| X will get | = | 36,000 | X | 7 |

| 10 | ||||

| = | 25,200 |

| Y will get | = | 36,000 | X | 3 |

| 10 | ||||

| = | 10,800 |

Advertisement-Y

Valuation of Goodwill

| X will get | = | 17,100 | X | 3 |

| 5 | ||||

| = | 10,260 |

| Y will get | = | 17,100 | X | 2 |

| 5 | ||||

| = | 6,840 |

Advertisement-X

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication