Advertisement

Question 61 Chapter 5 of +2-A

Advertisement

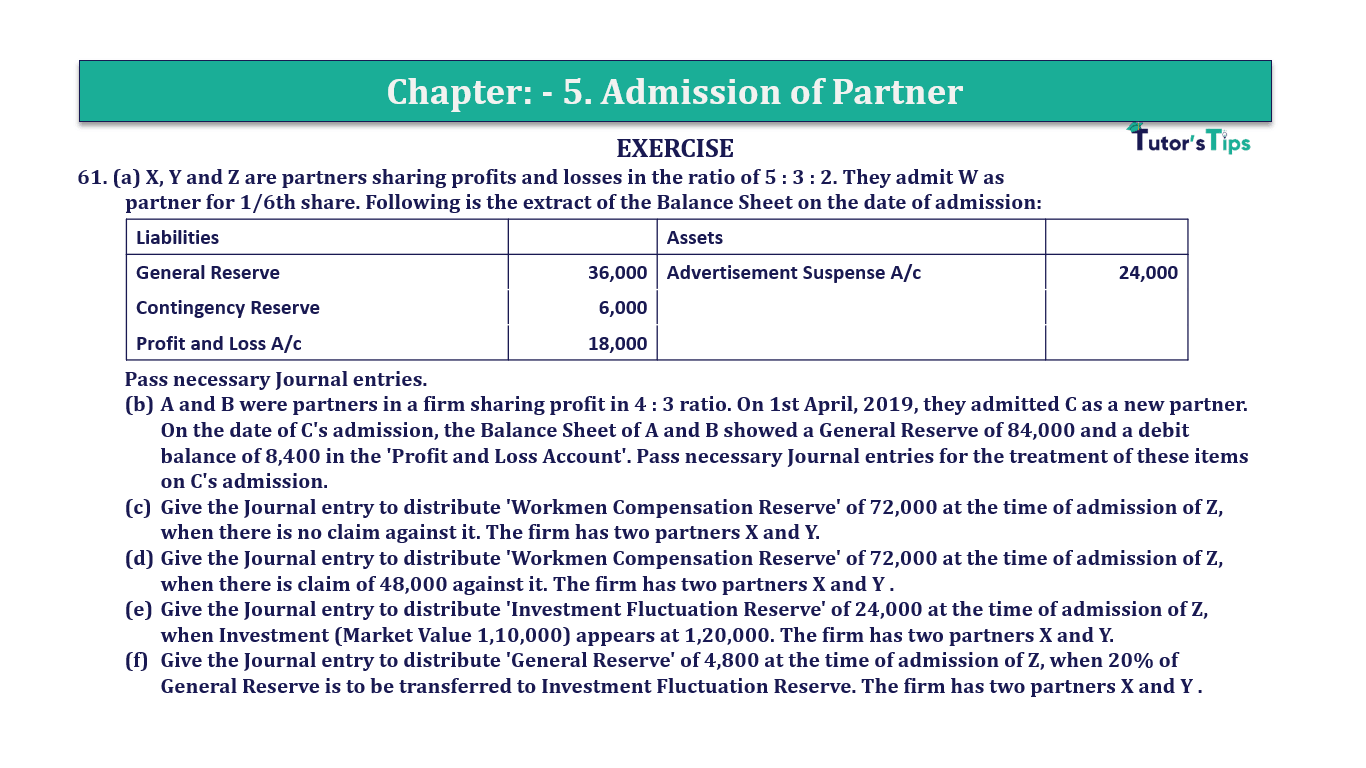

61. (a) X, Y and Z are partners sharing profits and losses in the ratio of 5 : 3 : 2. They admit W as partner for 1/6th share. Following is the extract of the Balance Sheet on the date of admission:

| Liabilities | Assets | ||

| General Reserve | 36,000 | Advertisement Suspense A/c | 24,000 |

| Contingency Reserve | 6,000 | ||

| Profit and Loss A/c | 18,000 |

Pass necessary Journal entries.

b. A and B were partners in a firm sharing profit in 4 : 3 ratio. On 1st April, 2019, they admitted C as a new partner. On the date of C’s admission, the Balance Sheet of A and B showed a General Reserve of 84,000 and a debit balance of 8,400 in the ‘Profit and Loss Account’. Pass necessary Journal entries for the treatment of these items on C’s admission.

c. Give the Journal entry to distribute ‘Workmen Compensation Reserve’ of 72,000 at the time of admission of Z, when there is no claim against it. The firm has two partners X and Y.

d. Give the Journal entry to distribute ‘Workmen Compensation Reserve’ of 72,000 at the time of admission of Z, when there is claim of 48,000 against it. The firm has two partners X and Y .

e. Give the Journal entry to distribute ‘Investment Fluctuation Reserve’ of 24,000 at the time of admission of Z, when Investment (Market Value 1,10,000) appears at 1,20,000. The firm has two partners X and Y.

f. Give the Journal entry to distribute ‘General Reserve’ of 4,800 at the time of admission of Z, when 20% of General Reserve is to be transferred to Investment Fluctuation Reserve. The firm has two partners X and Y .

g. A, B and C were partners sharing profits and losses in the ratio of 6 : 3 : 1. They decide to take D into partnership with effect from 1st April, 2019. The new profit-sharing ratio between A, B, C and D will be 3 : 3 : 3 : 1. They also decide to record the effect of the following without affecting their book values, by passing a single adjustment entry:

| Book Values ( ) | |

| General Reserve | 1,50,000 |

| Contingency Reserve | 60,000 |

| Profit and Loss A/c (Cr.) | 90,000 |

| Advertisement Suspense A/c (Dr.) | 1,20,000 |

Pass the necessary single adjustment entry, through the Partner’s Current Account

The solution of Question 61 Chapter 5 of +2-A: –

Advertisement-X

Case A

| Date | Particulars | L.F. | Debit | Credit | |

| General Reserve A/c | Dr | 36,000 | |||

| Contingency Reserve A/c | Dr | 6,000 | |||

| Profit and Loss A/c | Dr | 18,000 | |||

| To X’s Capital A/c | 30,000 | ||||

| To Y’s Capital A/c | 18,000 | ||||

| To Z’s Capital A/c | 12,000 | ||||

| (Being distributed the balance of general reserve, Contingency Reserve and profit and loss account among the old partners in their old profit sharing ratio i.e. 5:3:2) | |||||

| X’s Capital A/c | Dr | 12,000 | |||

| Y’s Capital A/c | Dr | 7,200 | |||

| Z’s Capital A/c | Dr | 4,800 | |||

| To Advertisement Suspense A/c | 24,000 | ||||

| (Being distributed the balance of Advertisement Suspense among the old partners in their old profit sharing ratio i.e. 5:3:2) | |||||

| Revaluation A/c | Dr | 270 | |||

| To Motors A/c | 250 | ||||

| To Furniture A/c | 20 | ||||

| (Being Decrease in value of Motors and Furniture transferred to Revaluation Account) | |||||

Case B

| Date | Particulars | L.F. | Debit | Credit | |

| General Reserve A/c | Dr | 84,000 | |||

| To A’s Capital A/c | 48,000 | ||||

| To B’s Capital A/c | 36,000 | ||||

| (Being distributed the balance of general reserve among the old partners in their old profit sharing ratio i.e. 4:3) | |||||

| A’s Capital A/c | Dr | 4,800 | |||

| B’s Capital A/c | Dr | 3,600 | |||

| To Profit & Loss A/c | 8,400 | ||||

| (Being distributed the balance of Profit & Loss among the old partners in their old profit sharing ratio i.e. 4:3 | |||||

Case C

| Date | Particulars | L.F. | Debit | Credit | |

| Workmen Compensation Reserve A/c | Dr | 72,000 | |||

| To X’s Capital A/c | 36,000 | ||||

| To Y’s Capital A/c | 36,000 | ||||

| (Being distributed the balance of Workmen Compensation Reserve among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case D

| Date | Particulars | L.F. | Debit | Credit | |

| Workmen Compensation Reserve A/c | Dr | 72,000 | |||

| To Workmen Compensation Reserve claim A/c | 48,000 | ||||

| To X’s Capital A/c | 12,000 | ||||

| To Y’s Capital A/c | 12,000 | ||||

| (Being distributed the balance of Workmen Compensation Reserve among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case E

| Date | Particulars | L.F. | Debit | Credit | |

| Investment Fluctuation Reserve A/c | Dr | 24,000 | |||

| To Investment A/c | 10,000 | ||||

| To X’s Capital A/c | 7,000 | ||||

| To Y’s Capital A/c | 7,000 | ||||

| (Being distributed the balance of Workmen Compensation Reserve among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Advertisement-X

Advertisement-Y

Case F

| Date | Particulars | L.F. | Debit | Credit | |

| General Reserve A/c | Dr | 4,800 | |||

| To Investment Fluctuation Reserve A/c | 960 | ||||

| To X’s Capital A/c | 1,920 | ||||

| To Y’s Capital A/c | 1,920 | ||||

| (Being distributed the balance of General Reserve after transfer to the Investment Fluctuation Reserve from it among the old partners in equal ratio because profit sharing ratio is not given.) | |||||

Case G

| Date | Particulars | L.F. | Debit | Credit | |

| C’s Current A/c | Dr | 36,000 | |||

| D’s Current A/c | Dr | 18,000 | |||

| To A’s Current A/c | 54,000 | ||||

| (Being adjustment made at the time of admission of A) | |||||

| Old Ratio of A,B, and C | = | 6 : 3 : 3 |

| New Ratio of A,B, C, and D | = | 3 : 3 : 3 : 1 |

Sacrificing Share = Old Ratio – New Ratio

| X’s Sacrificing/Gaining Share | = | 6 | – | 3 |

| 10 | 10 |

| = | 6 – 3 | |

| 10 |

| = | 3 | Sacrifice | |

| 10 |

| Y’s Sacrificing/Gaining Share | = | 3 | – | 3 |

| 10 | 10 |

| = | 3 – 3 | |

| 10 |

| = | 0 | |

| 10 |

Advertisement-Y

| Z’s Sacrificing/Gaining Share | = | 1 | – | 3 |

| 10 | 10 |

| = | 1 – 3 | |

| 10 |

| = | -2 | Gains | |

| 10 |

Advertisement-X

| W’s Sacrificing/Gaining Share | = | 1 |

| 10 |

Calculation of Net Effect

| General Reserve | 1,50,000 | |

| Add: – Contingency Reserve | 60,000 | |

| Add: -Profit and Loss A/c (Cr.) | 90,000 | |

| 3,00,000 | ||

| Less: Advertisement Suspense A/c (Dr.) | – 1,20,000 | |

| 1,80,000 | ||

Adjustment of Revaluation Profit

| A will Get from C & D | = | 1,80,000 | X | 3 |

| 10 | ||||

| = | 54,000 |

| C will pay to A | = | 1,80,000 | X | 2 |

| 10 | ||||

| = | 36,000 |

| D will pay to Z | = | 1,80,000 | X | 1 |

| 10 | ||||

| = | 18,000 |

Advertisement-Y

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Advertisement-X

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication