Advertisement

Question 47 Chapter 1 of +2-Part-1

Advertisement

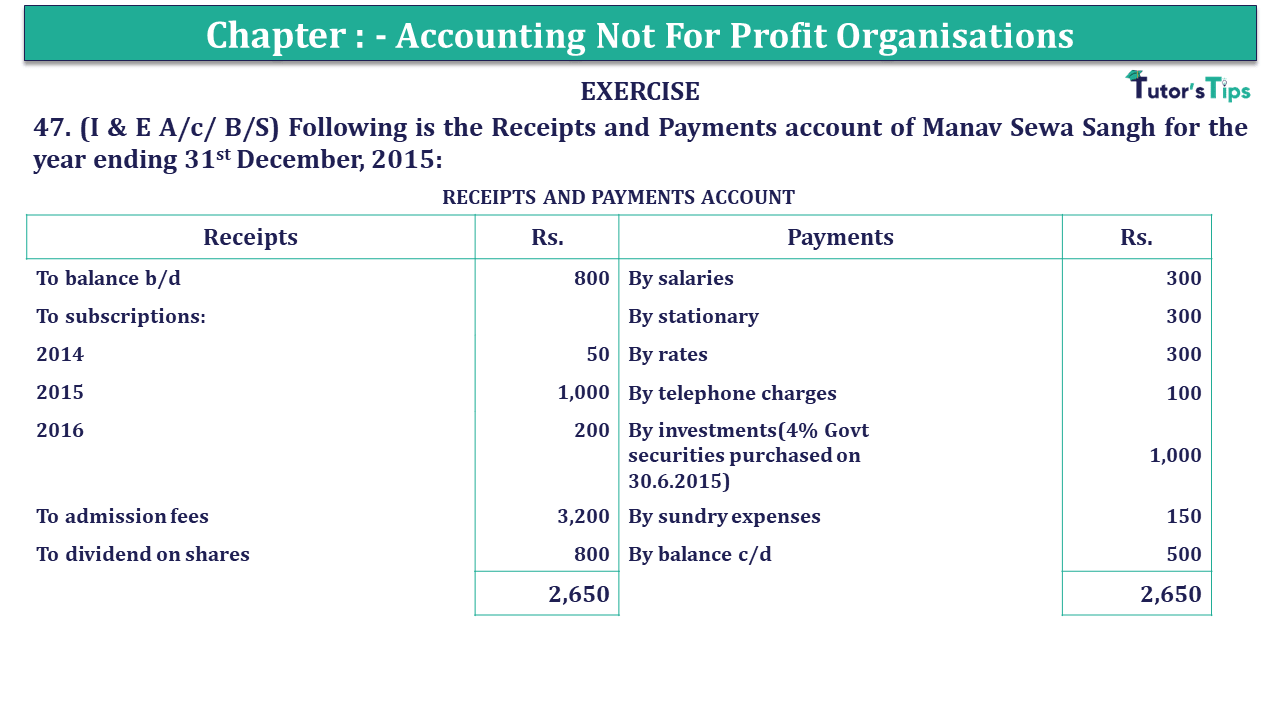

47. (I & E A/c/ B/S) Following is the Receipts and Payments account of Manav Sewa Sangh for the year ending 31st December 2015:

| RECEIPTS AND PAYMENTS ACCOUNT | |||

| Receipts | Rs. | Payments | Rs. |

| To balance b/d – Cash in hand | 800 | By salaries | 300 |

| To subscriptions: | By stationary | 300 | |

| 2014 (previous year) | 50 | By rates | 300 |

| 2015 | 1,000 | By telephone charges | 100 |

| 2016(new year) | 200 | By investments(4% Govt securities purchased on 30.6.2015) | 1,000 |

| To admission fees | 3,200 | By sundry expenses | 150 |

| To dividend on shares | 800 | By balance c/d | 500 |

| 2,650 | 2,650 | ||

Further information:

1) There are 600 members paying annual subscription Of Rs. 2 per head, Rs.90 being in arrear for 2014 at the beginning of 2015.

2) Stock of stationery on 31st December 2014 was Rs.200, on 31st December, 2015-Rs.100.

3) The rates were paid for 15 months up to 31st March 2016.

4) Sundry expenses outstanding on 31st December 2014 were Rs.50.

5) Telephone charges for 3 months outstanding, the amount due is Rs.40.

6) At 31st December 2014 – investments in shares were Rs.4,000.

7) At 31st December 2014 – the building stood in the books at Rs.10,000 and it is required to write off depreciation at 5% p.a.

You are required to prepare:

(a) the Income and Expenditure Account for the year ended 31st December 2015 and

(b) the balance sheet as on that date.

The solution of Question 47 Chapter 1 of +2 Part-1: –

| Income and Expenditure account of Manav Sewa Sangh For the year ending 31st December 2015 | |||||

| Expenditure | Amount | Income | Amount | ||

| To salaries | 300 | By subscriptions | 1,000 | ||

| To stationary | 300 | Add: outstanding (600*2)-1,000 | 200 | 1,200 | |

| Add: opening stock | 200 | By dividend on shares | 200 | ||

| Less: closing stock | 100 | 400 | By interest on investments (1,000 x 4/100 x 6/12) | 20 | |

| To rates | 300 | By excess of expenditure over income (deficit) | 260 | ||

| Less: Prepaid 1/5 | 60 | 360 | |||

| To telephone charges | 100 | ||||

| Add: outstanding | 40 | 140 | |||

| To sundry expenses | 150 | ||||

| Less: paid for 2014 | 50 | 100 | |||

| To depreciation on building @5% | 500 | ||||

| 1,680 | 1,680 | ||||

| Balance Sheet As on 31st March 2015 | |||||

| Liabilities | Amount | Assets | Amount | ||

| Capital Fund: | Cash in hand | 500 | |||

| -Opening Balance | 15,040 | Outstanding Subscriptions: | |||

| Add: Admission fees | 400 | -2014 (90 – 50) | 40 | ||

| Less: Deficiency | 260 | 15,180 | -2015 | 200 | 240 |

| Outstanding telephone charges | 40 | Stock of stationary | 100 | ||

| Subscriptions received in advance | 200 | Prepaid rates (300 x 3/15) | 60 | ||

| Investments in shares | 4,000 | ||||

| 4% Investments | 1,000 | ||||

| Accrued interest | 20 | ||||

| Building | 10,000 | ||||

| Less: Depreciation | 500 | 9,500 | |||

| 15,420 | 15,420 | ||||

Working Note:

1. Opening Capital Fund:

| Balance Sheet As on 1st January 2015 | |||||

| Liabilities | Amount | Assets | Amount | ||

| Outstanding sundry expenses | 50 | Outstanding Subscriptions | 90 | ||

| Capital Fund (Balancing Figure) | 15,040 | Cash in hand | 800 | ||

| Stock of stationary | 200 | ||||

| Building | 10,000 | ||||

| Investments in shares | 4,000 | ||||

| 15,090 | 15,090 | ||||

Note: In the absence of any instructions, the legacy has been treated as revenue income as the amount was very small.

Advertisement-X

Thanks, Please Like and share with your friends

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication