Advertisement

Question 44 Chapter 5 of +2-B

Advertisement

Table of Contents

PREPARING OF CASH FLOW STATEMENT (WITHOUT ADJUSTMENT)

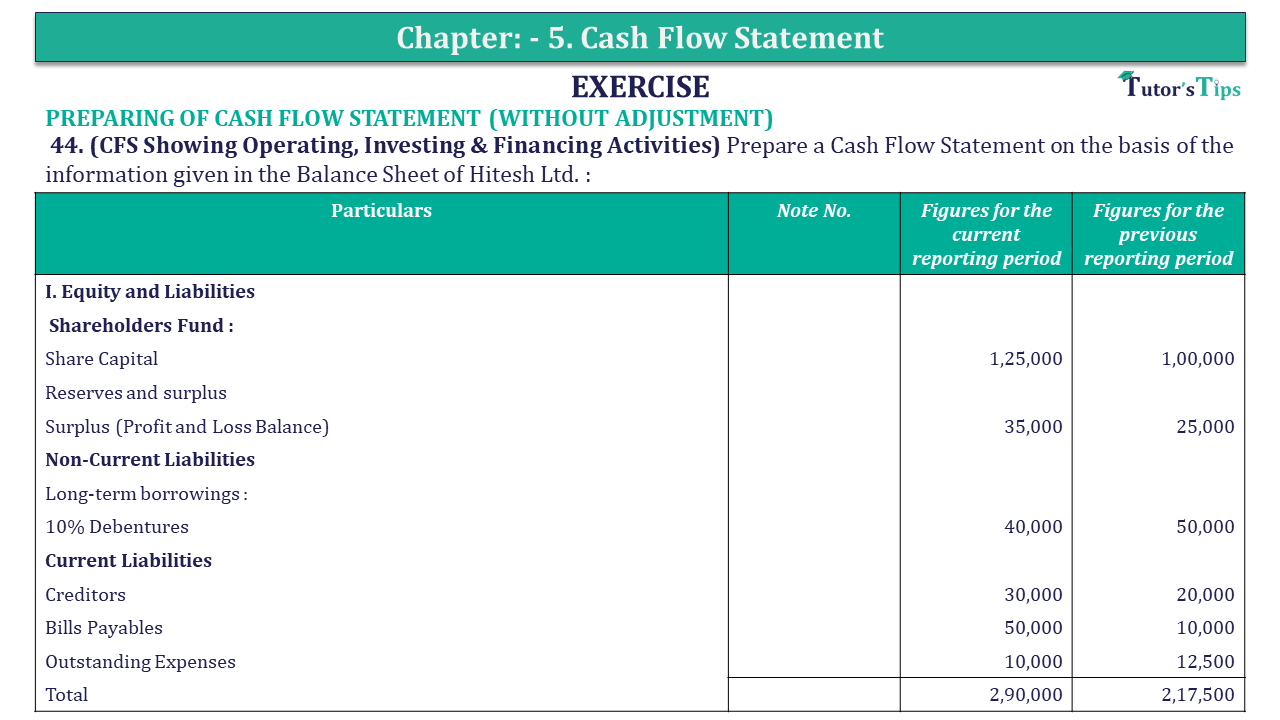

44. (CFS Showing Operating, Investing & Financing Activities) Prepare a Cash Flow Statement on the basis of the information given in the Balance Sheet of Hitesh Ltd. :

| Particulars | Note No. | Figures for the current reporting period | Figures for the previous reporting period |

| I. Equity and Liabilities | |||

| Shareholders Fund : | |||

| Share Capital | 1,25,000 | 1,00,000 | |

| Reserves and surplus | |||

| Surplus (Profit and Loss Balance) | 35,000 | 25,000 | |

| Non-Current Liabilities | |||

| Long-term borrowings : | |||

| 10% Debentures | 40,000 | 50,000 | |

| Current Liabilities | |||

| Creditors | 30,000 | 20,000 | |

| Bills Payables | 50,000 | 10,000 | |

| Outstanding Expenses | 10,000 | 12,500 | |

| Total | 2,90,000 | 2,17,500 | |

| II. Assets | |||

| Non –Current Assets | |||

| Tangible Assets | |||

| Land end Building | 1,40,000 | 1,00,000 | |

| Machinery | 65,000 | 50,000 | |

| Intangible Assets : | |||

| Goodwill | 1,000 | 5,000 | |

| Current Assets | |||

| Inventories | 25,000 | 35,000 | |

| Trade Receivable | 20,000 | 10,000 | |

| Input IGST | 6,000 | 2,000 | |

| Input CGST | 12,000 | 4,000 | |

| Input SGST | 12,000 | 4,000 | |

| Cash and cash equivalents : | |||

| Cash | 9,000 | 7,500 | |

| Total | 2,90,000 | 2,17,500 |

The solution of Question 44 Chapter 5 of +2-B: –

| Cash Flow Statement of Hitesh Ltd. | ||

| Particulars | Rs | |

| (A) Cash Flow from Operating Activities | ||

| Add: General Reserve | 10,000 | |

| Goodwill Written off | 4,000 | |

| Interest on debentures | 5,000 | |

| Cash operating Profit before Working Capital adj. | 19,000 | |

| Add: Decrease in Current Assets | ||

| Inventories | 10,000 | |

| Add: Increase in Current Liabilities | ||

| Creditors | 10,000 | |

| Bills Payable | 40,000 | |

| Less: Increase in Current Assets | ||

| Trade Receivable | 30,000 | |

| Input IGST | 4,000 | |

| Input CGST | 8,000 | |

| Input SGST | 8,000 | |

| Less: Decrease in Current Liabilities | ||

| Outstanding Expenses | 2,500 | 46,500 |

| Cash used in Operating Activities | 46,500 | |

| (B) Cash flows from Investing Activities | ||

| Outflow of Cash | ||

| Purchase of Land & Building | 40,000 | |

| Purchase of Machinery | 15,000 | 55,000 |

| Net cash used in investing Activities | 55,000 | |

| (C) Cash flows from Financing Activities | ||

| Inflow of Cash | ||

| Issue of share capital | 25,000 | |

| Outflow of Cash | ||

| Redemption of Debenture | 10,000 | |

| Interest on Debentures (10% of 50,000) | 5,000 | 10,000 |

| Net cash flow from financing activities | 10,000 | |

| Total Cash flow (A + B + C) | 1,500 | |

| Opening Balance Cash | 7,500 | |

| Closing Balance Cash | 9,000 | |

Advertisement-X

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication