Advertisement

Question 34 Chapter 7 of +2-A

Advertisement

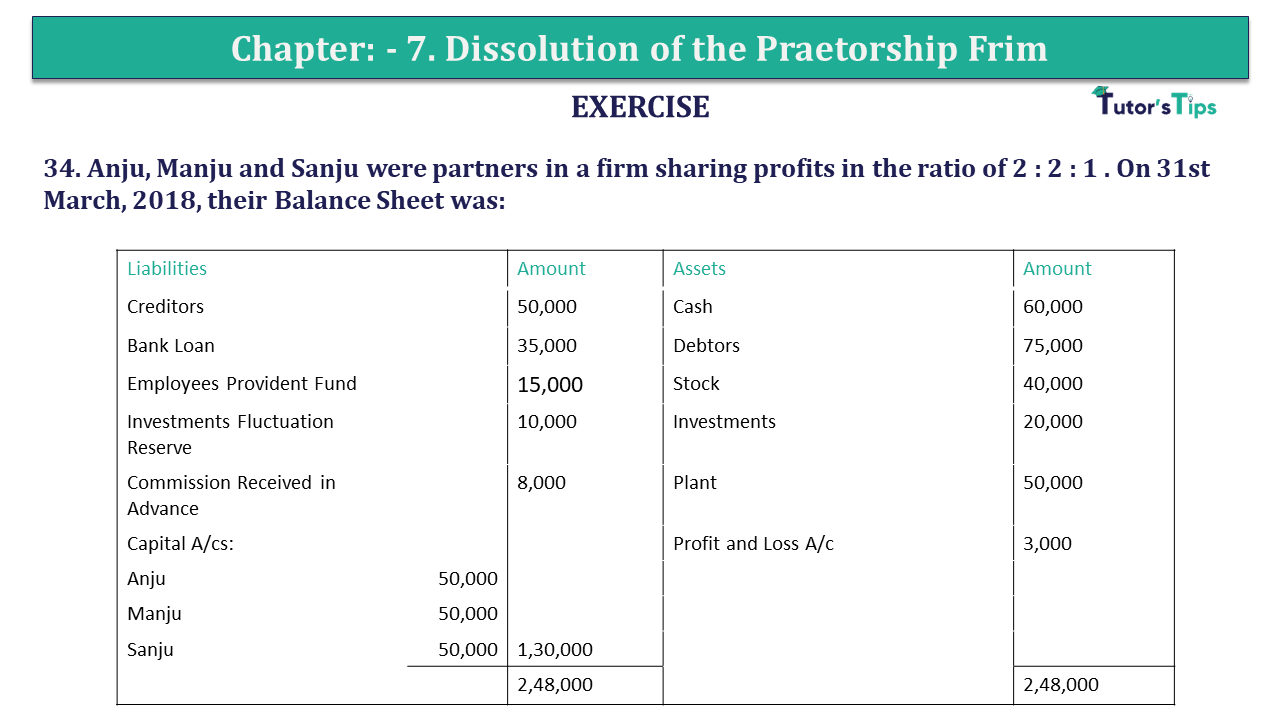

34. Anju, Manju and Sanju were partners in firm sharing profits in the ratio of 2 : 2: 1. On 31st March 2018, their Balance Sheet was:

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 50,000 | Cash | 60,000 | ||

| Bank Loan | 35,000 | Debtors | 75,000 | ||

| Employees Provident Fund | 15,000 | Stock | 40,000 | ||

| Investments Fluctuation Reserve | 10,000 | Investments | 20,000 | ||

| Commission Received in Advance | 8,000 | Plant | 50,000 | ||

| Capital A/cs: | Profit and Loss A/c | 3,000 | |||

| Anju | 50,000 | ||||

| Manju | 50,000 | ||||

| Sanju | 50,000 | 1,30,000 | |||

| 2,48,000 | 2,48,000 |

On this date, the firm was dissolved. Anju was appointed to realise the assets. Anju was to receive 5% commission on the sale of assets except for cash and was to bear all expenses of realisation. Anju realised the assets as follows : Debtors 60,000; Stock 35,500; Investments 16,000; Plant 90% of the book value . Expenses of Realisation amounted to 7,500. The commission received in advance was returned to customers after deducting 3,000. The firm had to pay 8,500 for Outstanding Salary, not provided for earlier, Compensation paid to employees amounted to 17,000. This liability was not provided for in the above Balance Sheet. 20,000 had to be paid for the Employees’ Provident Fund. Prepare Realisation Account, Capital Accounts of Partners and Cash Account

The solution of Question 34 Chapter 7 of +2-A: –

| Realization Account | |||||

| Particular | Amount | Particular | Amount | ||

| Debtors | 75,000 | Creditors | 50,000 | ||

| Stock | 40,000 | Bank Loan | 35,000 | ||

| Investment | 20,000 | Provident Fund | 15,000 | ||

| Plant | 50,000 | Commission Received in Advance | 8,000 | ||

| Investments Fluctuation Fund | 10,000 | ||||

| Cash A/c: | |||||

| Commission Received in Advance | 5,000 | 7,500 | Cash A/c: | ||

| Outstanding Salary | 8,500 | Debtors | 60,000 | ||

| Compensation paid to Employees | 17,000 | Stock | 35,500 | ||

| Provident Fund | 20,000 | Investments | 16,000 | ||

| Creditors | 50,000 | Plant | 45,000 | 1,56,500 | |

| Bank Loan | 35,000 | 1,35,500 | |||

| Anuj’s Capital A/c | 7,825 | Loss transferred to: | |||

| Anju’s Capital A/c | 21,530 | ||||

| Manju’s Capital A/c | 21,530 | ||||

| Sanju’s Capital A/c | 10,765 | 53,825 | |||

| 3,28,325 | 3,28,325 | ||||

Advertisement-X

| Partners’ Capital Account | |||||||

| Part. | Anju | Manju | Sanju | Part. | Anju | Manju | Sanju |

| To Profit and Loss A/c | 1,200 | 1,200 | 600 | By Balance B/d | 50,000 | 50,000 | 30,000 |

| To Realization A/c Loss | 21,530 | 21,530 | 10,765 | By Realization A/c | 7,825 | – | |

| To Cash A/c | 35,095 | 27,270 | 18,635 | ||||

| 57,825 | 50,000 | 30,000 | 57,825 | 50,000 | 30,000 | ||

| Bank Account | |||||

| Particular | Amount | Particular | Amount | ||

| Balance b/d | 60,000 | Realization A/c | 1,35,500 | ||

| Anju’s Capital A/c | 35,095 | ||||

| Realization A/c | 1,56,500 | Manju’s Capital A/c | 27,270 | ||

| Sanju’s Capital A/c | 18,635 | ||||

| 2,16,500 | 2,16,500 | ||||

WORKING NOTE:-

Advertisement-X

Anju’s commission

| Anju’s commission | = | Assets Realised | X | 5 |

| 100 | ||||

| = | 1,56,500 | X | 5 | |

| 100 | ||||

| = | Rs 7,825 |

Advertisement-Y

| Realisation of the Profit | = | 50,000 | X | 90 |

| 100 | ||||

| = | Rs 45,000 |

T.S. Grewal’s Double Entry Book Keeping +2 (Vol. I: Accounting for Not-for-Profit Organizations and Partnership Firms)

- Chapter No. 1 – Financial Statement of Not-For-Profit Organisations

- Chapter No. 2 – Accounting for Partnership Firms – Fundamentals

- Chapter No. 3 – Goodwill: Nature and Valuation

- Chapter No. 4 – Change in Profit-Sharing Ratio Among the Existing Partners

- Chapter No. 5 – Admission of a Partner

- Chapter No. 6 – Retirement/Death of a Partner

- Chapter No. 7 – Dissolution of a Partnership Firm

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 8 – Company Accounts – Accounting for Share Capital

- Chapter No. 9 – Company Accounts – Issue of Debentures

- Chapter No. 10 – Redemption of Debentures

T.S. Grewal’s Double Entry Book Keeping (Vol. II: Accounting for Companies)

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis – Comparative Statements and Common- Size Statements

- Chapter No. 4 – Accounting Ratios

- Chapter No. 5 – Cash Flow Statement

Advertisement-X

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication