Advertisement

Question 33 Chapter 6 of +2-Part-1

Advertisement

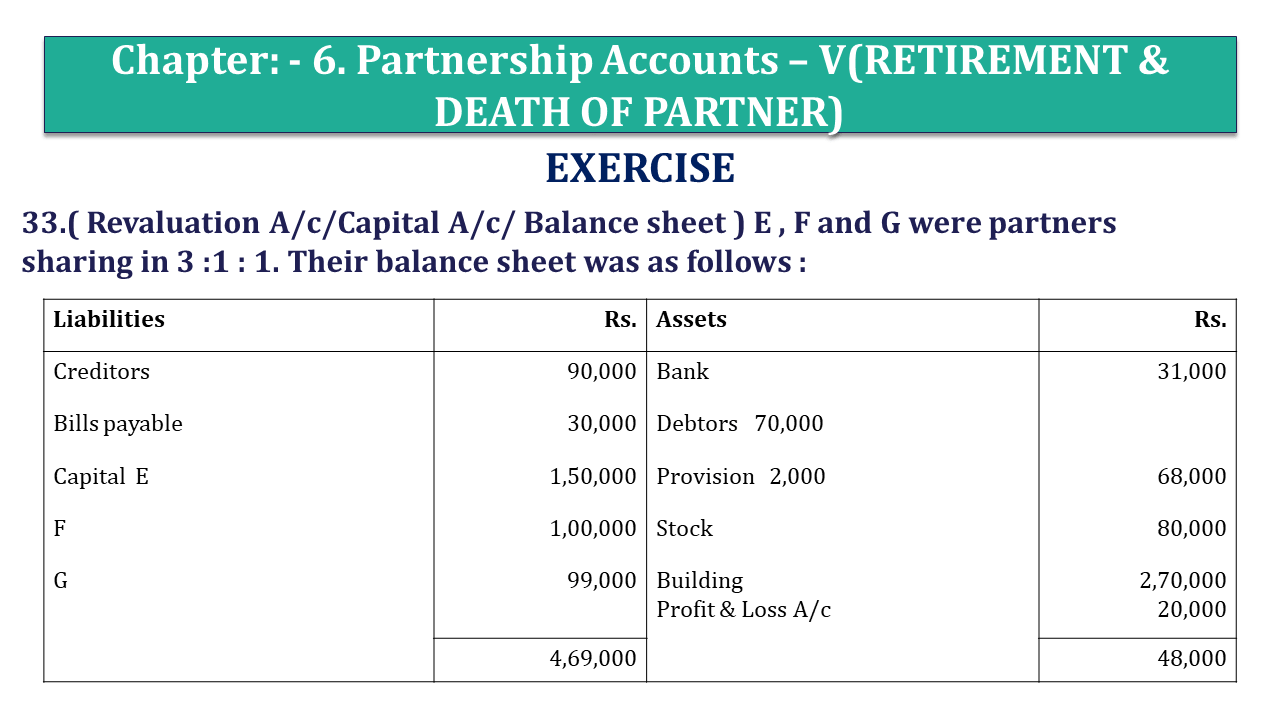

33.( Revaluation A/c/Capital A/c/ Balance sheet ) E , F and G were partners sharing in 3 :1 : 1. Their balance sheet was as follows :

| Liabilities | Rs. | Assets | Rs. |

| Creditors | 90,000 | Bank | 31,000 |

| Bills payable | 30,000 | Debtors 70,000 | |

| Capital E | 1,50,000 | Provision 2,000 | 68,000 |

| F | 1,00,000 | Stock | 80,000 |

| G | 99,000 | Building | 2,70,000 |

| Profit & Loss A/c | 20,000 | ||

| 4,69,000 | 48,000 |

F retired on following terms :

(i) Building is appreciated by 10%.

(ii) Provide for doubtful debts at 10% on debtors.

(iii) Creditors Rs. 10,000 will not be claimed.

(iv) There was an outstanding repair bill Rs. 2,000.

(v) Goodwill of firm valued at Rs. 75,000.

(vi) F is paid Rs. 20,000 and balance transferred to his Loan A/c . Prepare all necessary ledger accounts and balance sheet.

The solution of Question 33 Chapter 6 of +2 Part-1: –

| Revaluation account | |||||

| Particulars | Amount | Particulars | Amount | ||

| To provision d/d | 5,000 | By Building A/c | 27,000 | ||

| To outstanding claim | 2,000 | By creditors | 10,000 | ||

| To profits transferred | |||||

| E | 18,000 | ||||

| F | 6,000 | ||||

| G | 6,000 | 30,000 | |||

| 37,000 | 37,000 | ||||

| Partners’ Capital Account | |||||||

| Particulars | E | F | G | Particulars | E | F | G |

| To Profit & Loss A/c | 12,000 | 4,000 | 4,000 | By Balance b/d | 1,50,000 | 1,00,000 | 99,000 |

| To F’s capital A/c | 11,250 | 3,750 | By Revaluation A/c | 18,000 | 6,000 | 6,000 | |

| To cash A/c | 20,000 | By B’s capital A/c | 11,250 | ||||

| To F’s loan A/c | 97,000 | By C’s capital A/c | 3,750 | ||||

| To Balance c/d | 1,44,750 | – | 97,250 | ||||

| 1,68,000 | 1,21,000 | 1,05,000 | 1,68,000 | 1,21,000 | 1,05,000 | ||

| Balance Sheet | |||||

| Liabilities | Amount | Assets | Amount | ||

| Creditors | 80,000 | Bank | 11,000 | ||

| Bills payable | 30,000 | Debtors | 70,000 | ||

| Outstanding repair charges | 2,000 | Less provision | 7,000 | 63,000 | |

| E’s Capital A/c | 1,44,750 | Stock | 80,000 | ||

| G’s Capital A/c | 97,250 | Building | 2,97,000 | ||

| F’s loan | 97,000 | ||||

| 4,51,000 | 4,51,000 | ||||

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Advertisement-X

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication