Advertisement

Question 08 Chapter 7 of +2-Part-1

Advertisement

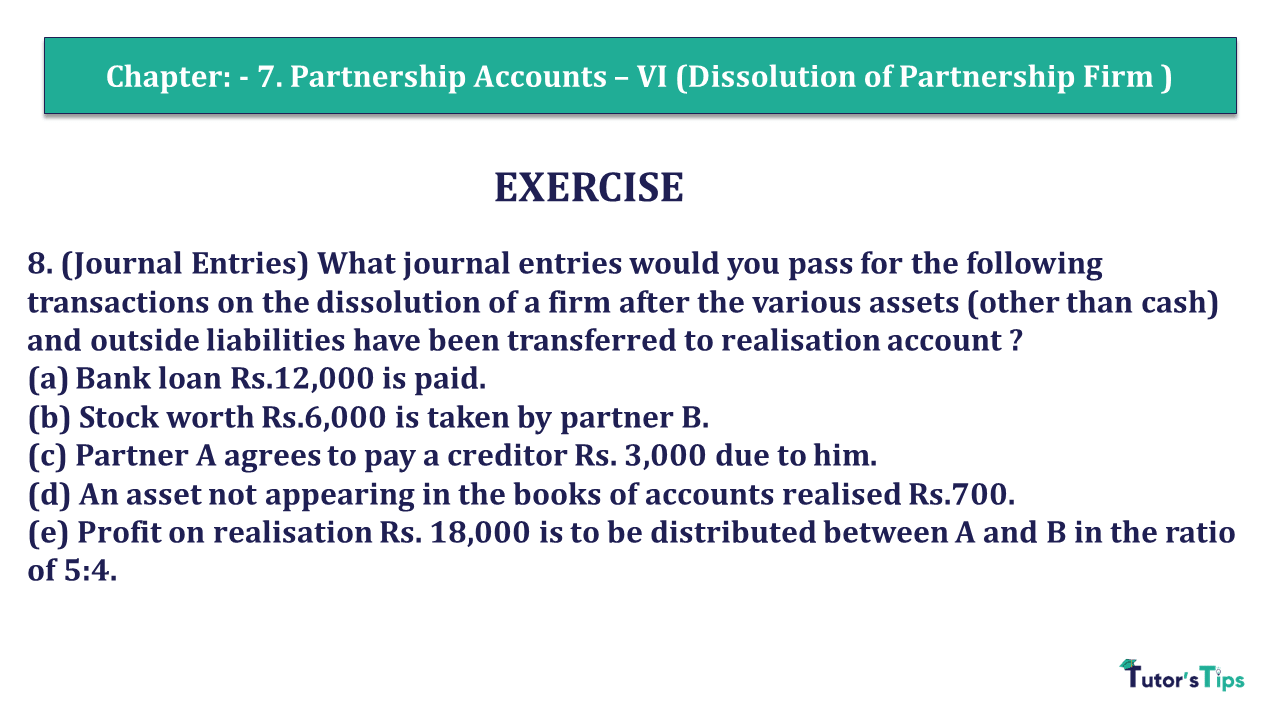

8. (Journal Entries) What journal entries would you pass for the following transactions on the dissolution of a firm after the various assets (other than cash) and outside liabilities have been transferred to realisation account ?

(a) Bank loan Rs.12,000 is paid.

(b) Stock worth Rs.6,000 is taken by partner B.

(c) Partner A agrees to pay a creditor Rs. 3,000 due to him.

(d) An asset not appearing in the books of accounts realised Rs.700.

(e) Profit on realisation Rs. 18,000 is to be distributed between A and B in the ratio of 5:4.

We are providing a solution of Question 8 Chapter 7 of +2 Part-1 in two formats. one is in Video format and another is in article format. Check out both formats as follows:

1. Check out the Solution of this question in Video Format:-

The video consists solution of question numbers from 6 to 10 Chapter no. 7 class 12 of Usha publication. To check the direct solution of question no. 8 from the flowing video by using time stamps of the video.

2. Check out the Solution of this question in Article Format:-

The solution of Question 08 Chapter 7 of +2 Part-1: –

| Journal | |||||

| Date | Particulars | L.F. | Debit | Credit | |

| a) | Realisation A/c | Dr. | 12,000 | ||

| To cash A/c | 12,000 | ||||

| (Being repayment of bank loan) | |||||

| b) | B’s capital A/c | Dr. | 6,000 | ||

| To realisation A/c | 6,000 | ||||

| (Being stock taken over by B ) | |||||

| c) | Realisation A/c | Dr. | 3,000 | ||

| To A’s capital A/c | 3,000 | ||||

| (Being firm’s liabilities assumed by A) | |||||

| d) | Cash A/c | Dr. | 700 | ||

| To realisation A/c | 700 | ||||

| (Being amount realized from the sale of unrecorded asset) | |||||

| e) | Realisation A/c | Dr. | 18,000 | ||

| To A’s capital A/c | 10,000 | ||||

| To B’s capital A/c | 8,000 | ||||

| (Being profit on realisation credited to partners in the ratio 5:4) | |||||

Advertisement-X

Comment if you have any questions.

Also, Check out the solved question of previous Chapters: –

Usha Publication – Accountancy PSEB (Class 12) – Volume I – Solution

- Chapter No. 1 – Accounting Not for Profit Organisations

- Chapter No. 2 – Partnership Accounts – I (Introduction)

- Chapter No. 3 – Partnership Accounts – II (Goodwill: Nature and Valuation)

- Chapter No. 4 – Partnership Accounts – III (Reconstitution of Partnership)

- Chapter No. 5 – Partnership Accounts – IV (Admission of A Partner)

- Chapter No. 6 – Partnership Accounts – V (Retirement and Death of A Partner)

- Chapter No. 7 – Partnership Accounts – VI (Dissolution of Partnership Firm)

- Chapter No. 8 – Company Accounts (Share Capital)

- Chapter No. 9 – Company Accounts (Issue of Debentures)

- Chapter No. 10 – Company Accounts (Redemption of Debentures)

Usha Publication – Accountancy PSEB (Class 12) – Volume II – Solution

- Chapter No. 1 – Financial Statements of a Company

- Chapter No. 2 – Financial Statement Analysis

- Chapter No. 3 – Tools of Financial Statement Analysis- Comparative and Common Size

- Chapter No. 4 – Ratio Analysis

- Chapter No. 5 – Cash Flow Statement

Check out T.S. Grewal +2 Book 2020@ Official Website of Sultan Chand Publication