Advertisement

Today we are covering the technical and conceptual topic of the Bank Reconciliation Statement. So please read it very consciously and in this article, you will learn the meaning of the Bank Reconciliation Statement, Causes of Difference, Need, types of Balance, Process of preparing BRS and understand it in much better ways we will solve one example of it.

Advertisement

What is Bank Reconciliation Statement?

The statement which is shown the items of difference between bank balance as per cash book and Bank balance as per bank statement or passbook. It is also known as BRS. In other words, it is an explanation of the difference between bank balance as per cash book and bank balance as per Passbook (Bank statement).

Sometimes, The bank balance as per the cash book and passbook does not tally with each other, so we can know the difference between them by preparing the bank reconciliation statement.

The bank reconciliation is the process of checking the differences between a bank column of the cash book and the bank statement or passbook. We have to check all the transactions recorded in the cash book with transactions recorded in the passbook by our bank. At the end of the Financial Year BRS is attached to the financial statement of the business, if there is any difference between both balances.

What is Passbook?

Advertisement-X

Before the explanation of the BRS, you have to know the meaning of the Passbook or bank statement. So, it is explained as follows: –

We have recorded all bank related transactions in the bank column of the cash book. Similarly, the banks also maintain their customer’s accounts in their books of account. Statement of the account given to the customer by the bank is called Passbook. It shows the actual balance of a particular customer with the bank.

The format of the Passbook is shown as follows:-

Explanation of column of Passbook

- Date: – Date of transaction

- Particulars: – show the opposite account detail or code.

- Cheque No.: – If the transaction of deposit or withdrawal is done by cheque the cheque will print in this column.

- Debit: – When customer withdrawal cash

- Credit: – When customer deposit cash

- Balance: – Net balance after withdrawal or deposit.

The Balance of the customer’s account shown in the book of the bank is called balance as per Passbook.

Causes of Difference in the Bank balance as per Cashbook and the Passbook.

- Business record the transaction by the delay.

- The cheque or bills receivable was dishonoured but business did not get intimation.

- Bank Charges deducted by the bank.

- Interest on balance given by the bank.

- Direct payment deposited in the bank by the customer.

- A bank record the transaction by the delay.

- The Cheque issued by business but not presented in the bank by the receiver of the cheque.

- The Cheque deposited by the business in the bank but due to some reason cheque not cleared yet.

- Clerical Mistake in the recording of the transaction by the business.

- Clerical Mistake in the recording of the transaction by the bank.

The need for Bank Reconciliation:

- It helps in detecting errors.

- we can track our interest (charges or received) and fees.

- The business will know the delays in the collection of payment of every customer.

- It helps in completing the cash book by providing information regarding bank charge, cheque or bills receivable dishonoured, direct payment, interest on balance and etc.

- It helps to auditors to know the difference between the bank balance as per cash book and the passbook.

Type of Bank balance: –

There are two types of balance explained as follows we have to explain it with an example image:

- Favourable Balance.

- Unfavourable Balance.

What is Favourable Balance?

Advertisement-X

A favourable Balance means that balance that is in favour of the enterprises. these are shown as follows:-

1. The Debit Balance of a bank column as per cash book. Highlighted in the following image with red colour.

2. The Credit Balance of a bank account as per a Passbook. Highlighted in the following image with red colour.

What is Unfavourable Balance?

The unfavourable Balance means that balance is not in favour of the enterprises. these are shown as follows:-

1. The Credit Balance of a bank column as per cash book. Highlighted in the following image with red colour.

2. The Debit balance of a bank account as per a Passbook. Highlighted in the following image with red colour.

The process of preparing the Bank Reconciliation Statement:

Advertisement-X

1st Step: – Get both statements of account and check out the difference in the balance if any then move to the next step or if tallied then we don’t need to prepare Bank Reconciliation Statement.

- Statement of bank balance as per cash book

- Statement of the bank account in the bank book. (in a simple copy of passbook)

2nd Step: – Tally the balance of both statements with each other if tallied then we do not of bank reconciliation or if not tallied then check of the transaction individual shown in the attached video and images follows.

3rd Step: – Get the un-ticked transaction from both the statements

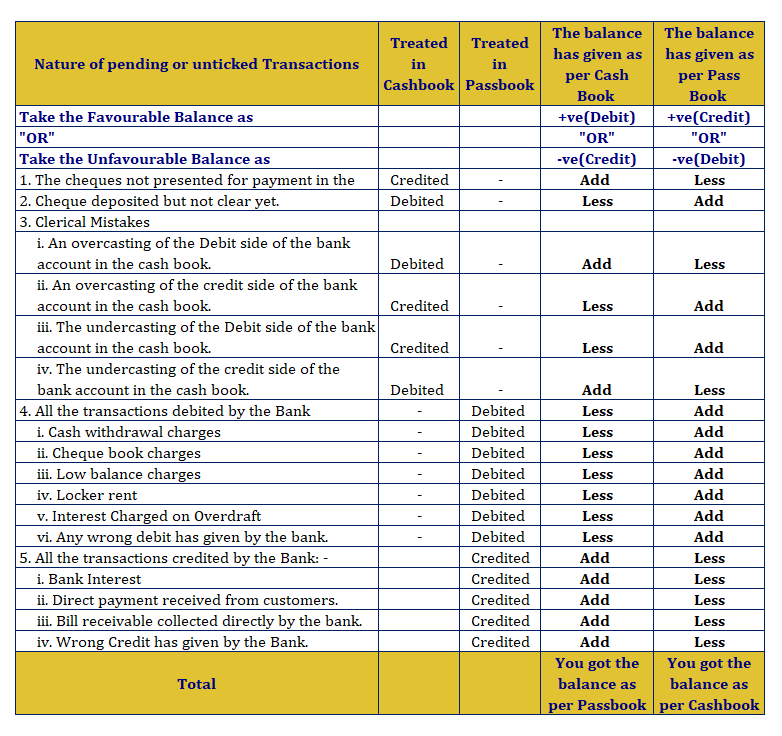

4th Step: – Arrange all un-ticked or pending transactions according to their nature shown as follows:-

- The cheques not presented for payment in the bank.

- Cheque deposited but not clear yet.

- Clerical Mistakes: –

- An overcasting of the Debit side of the bank account in the cash book.

- An overcasting of the credit side of the bank account in the cash book.

- The undercasting of the Debit side of the bank account in the cash book.

- The undercasting of the credit side of the bank account in the cash book

- All the transactions debited by the Bank: –

- Cash withdrawal charges.

- Cheque book charges.

- Low balance charges.

- Locker rent.

- Interest Charged on Overdraft.

- Any wrong debit has given by the bank.

- All the transactions credited by the Bank: –

- Bank Interest

- Direct payment received from customers.

- Bill receivable collected directly by the bank.

- Wrong Credit has given by the Bank.

5th Step: – Now, prepare a bank reconciliation statement and get to know the impact of the pending transaction on bank balance as per the cash book if we are doing a question based on balance as per cash book and check the impact of the pending transaction on bank balance as per the Passbook if we are doing a question on based on balance as per passbook.

We had treated the transactions by two aspects of accounting:-

- Debit

- Credit

| If un-ticked or Pending Transactions had | The balance has been given as per Cash Book | The balance has been given as per Pass Book |

| Debited to the bank account by us | Less | Add |

| Credited to the bank account by Us | Add | Less |

| Debited to the bank account by Bank | Less | Add |

| Credited to the bank account by Bank | Add | Less |

If the balance has given as per cash book: –

1. Debit:-

- If we had debited the Bank account, it means we added an amount of transaction from the bank account. So, we have to subtract it from the balance of bank account in our books to get to know the balance as per passbook.

- If Bank had debited our Bank account, it means they had subtracted an amount of transaction from our bank account. So, we have to add it in the balance of the bank account in our books to get know the balance as per passbook.

2. Credit:-

- If we had credited the Bank account, it means we subtract an amount of transaction from the bank account. So, we have to add back it in the balance of the bank account in our books to get know the balance as per Passbook.

- If Bank had credited our Bank account, it means they had added an amount of transaction in our bank account. So, we have to subtract it from the balance of the bank account in our books to get know the balance as per Passbook.

If the balance has given as per Passbook: –

1. Debit:-

- If we had debited the Bank account, it means we added an amount of transaction from the bank account. So, we have to subtract it from the balance of the bank account as per the Passbook to get to know the balance as per Cashbook.

- If Bank had debited our Bank account, it means they had subtracted an amount of transaction from our bank account. So, we have to add it to the balance of the bank account as per the Passbook to get to know the balance as per Cashbook.

2. Credit:-

- If we had credited the Bank account, it means we subtract an amount of transaction from the bank account. So, we have to add back it in the balance of the bank account as per Passbook to get know the balance as per Cashbook.

- If Bank had credited our Bank account, it means they had added an amount of transaction to our bank account. So, we have to subtract it from the balance of the bank account as per the Passbook to get to know the balance as per Cashbook.

Cheat sheet – Bank reconciliation Statement

Advertisement-X

Advertisement-Y

The treatment of all the transactions which you will get in the question of the BRS shown as follow:

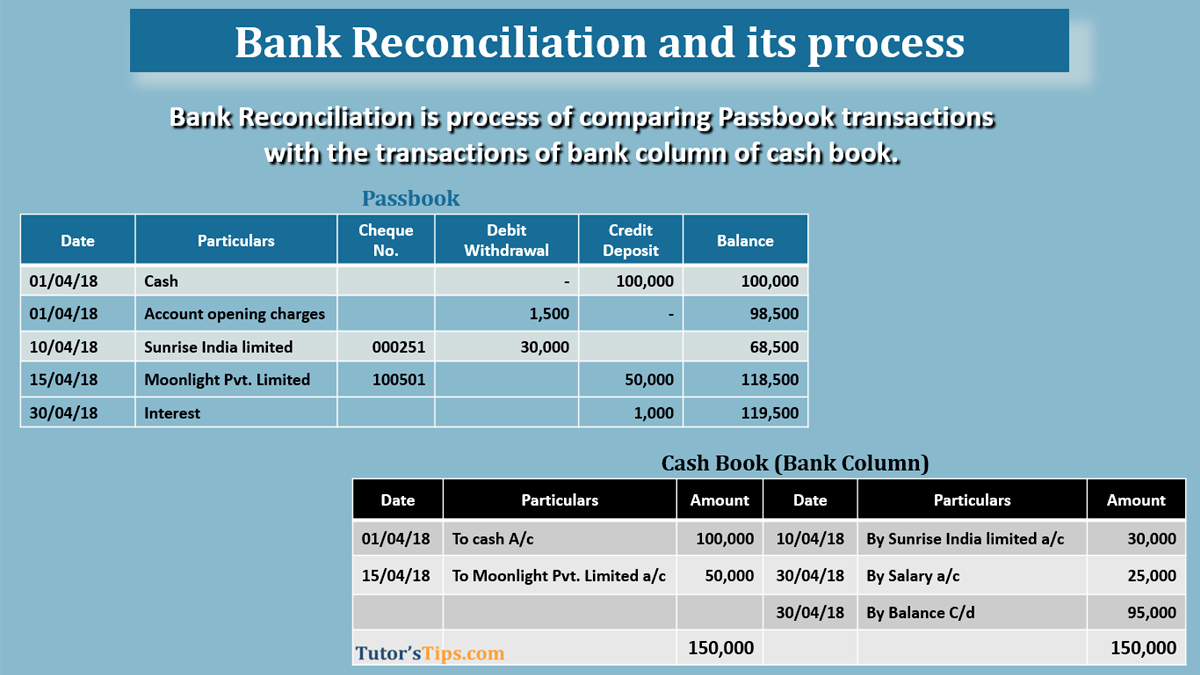

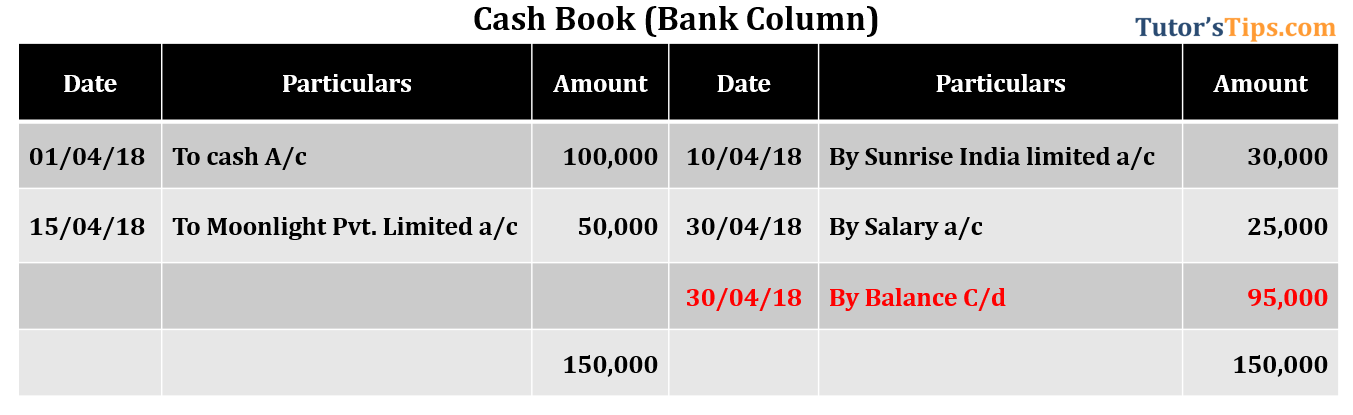

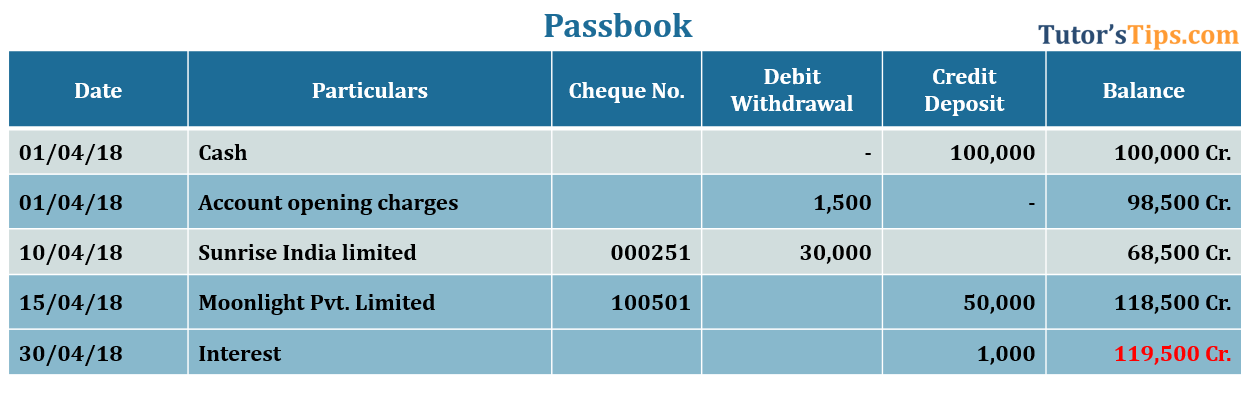

Illustration of bank Reconciling Statement: –

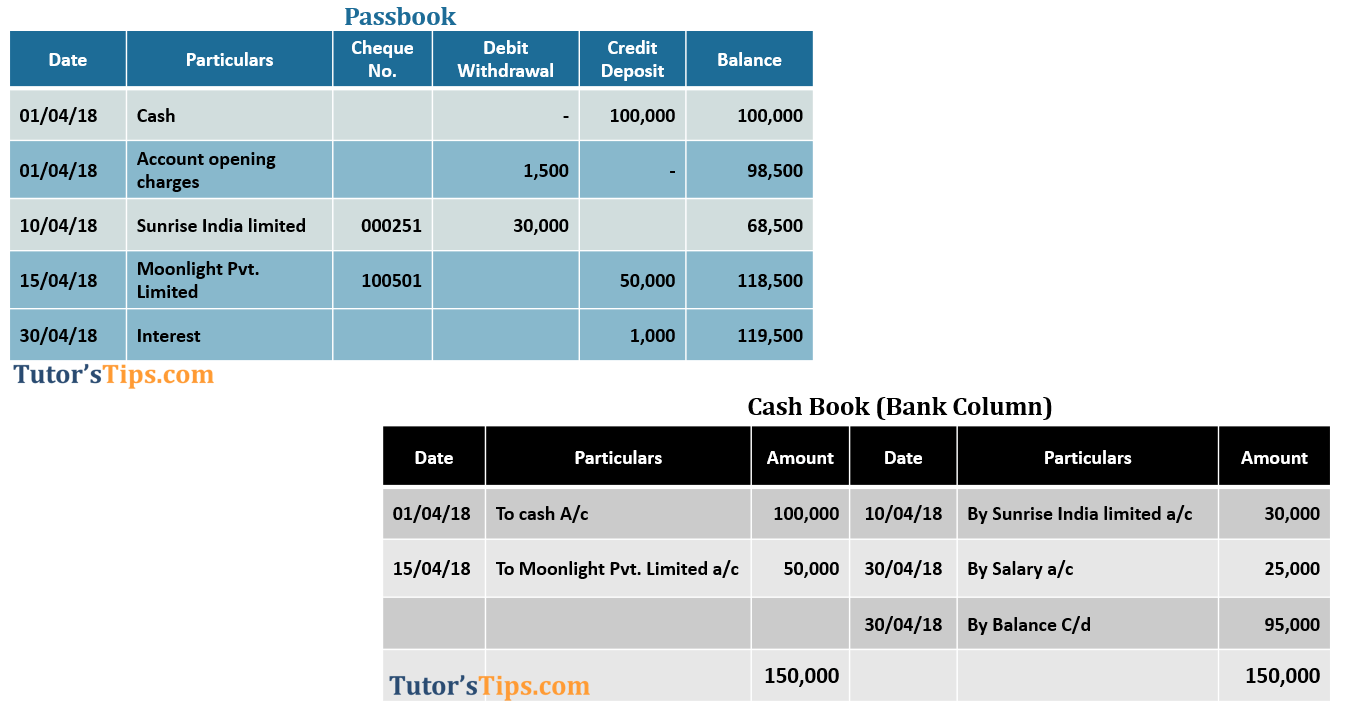

Following are both statements of M/s _____ Ltd. like passbook and cashbook. Prepare the Bank Reconciliation Statement.

Solution:

1st step:- checking the balance of both statements

- Passbook showed 119,500

- Cashbook Showed 95,000

2nd Step:- If there is a difference then we have to reconcile both statements.

- Yes, there is a difference in the balance of both statements.

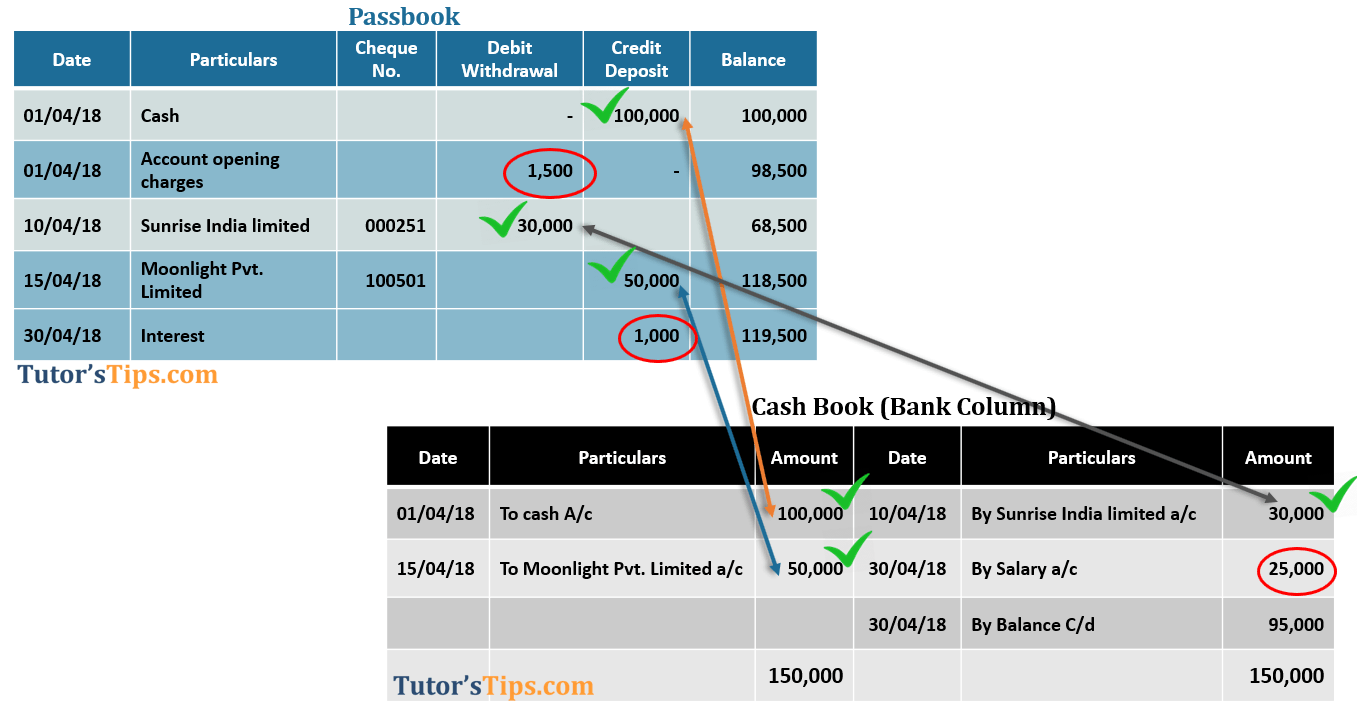

3rd Step:- Now if there is a difference then we have to check it out by ticking individual debit transaction as per passbook with credit as per cash book and Credit as per passbook with the Debit as per cash book as shown in the below image:

At last, we got the reason for the difference between both statements shown as follow: –

Advertisement-X

We have shown the matched or ticked(tallied) transaction with the help of different colours of arrows: –

- Orange arrow Shows ticking of cash deposited in the bank account.

- Gray arrow shows a payment made to sunrise India limited.

- Blue arrow shows a payment received from moonlight Pvt. Limited.

and we have shown the not matched or ticked(tallied) transaction with the help of the red circle: –

- Bank charges for the accounting opening shown only in the passbook of 1,500/-

- Bank Interest on the credit balance in the bank account shown only in the passbook of 1,000/-

- Cheque issued for salary but not yet cleared in the Passbook shown only in the cash book of 25,000/-

4th Step: – Arrange all un-ticked or pending transactions according to their nature shown as follows:-

- Cheque Issued but not cleared: –

- Cheque issued for salary.

- All the transactions debited by the Bank: –

- Bank Charges.

- All the transactions Credit by the Bank: –

- Bank Interest.

5th Step: – Now, preparing the Bank Reconciliation Statement shown in the following image: –

1. The balance has been given as per Cash Book

2. The balance has been given as per Passbook: –

Advertisement-X

Thanks for reading the topic of the Bank Reconciliation Statement, Please comment your feedback whatever you want.

Or

If you have any questions please ask us by commenting.